Welcome to Maintain Market; we post finance, investment, insurance, and loan blogs. In this blog, we will talk about the Best SIP Plans for 5 Years in India.

Introduction: Why SIP for 5 Years Matters

A Systematic Investment Plan (SIP) is one of the most popular and effective ways to build wealth in India — especially for investors with a 5-year horizon.

Unlike lump-sum investing, SIP lets you:

✔ Invest small amounts regularly

✔ Benefit from rupee cost averaging

✔ Reduce timing risk

✔ Build disciplined investing habits

A 5-year SIP is ideal for:

- Young professionals

- Medium-term goals (car, house down payment)

- Wealth creation without huge capital

- Retirement corpus enhancer

This guide will cover everything you must know before choosing the best SIP plans for 5 years in India.

What Is an SIP?

A Systematic Investment Plan (SIP) allows you to invest a fixed amount at regular intervals (monthly/quarterly) into mutual funds.

Benefits:

- Rupee Cost Averaging

- Compounding effect

- Disciplined investing

- Low financial stress

Example:

If you invest ₹5,000 per month for 5 years at 10% annual returns, your corpus can grow significantly thanks to compounding.

Why 5 Years Is a Smart Time Frame

Here’s why a 5-year SIP plan makes financial sense:

✔ Equity markets tend to smooth out volatility

✔ Mid-term goals (wedding, home upgrades)

✔ Good balance of growth + moderate risk

Risk reduces significantly if you stay invested for longer than 3 years. A 5-year horizon offers growth while avoiding short-term market panic.

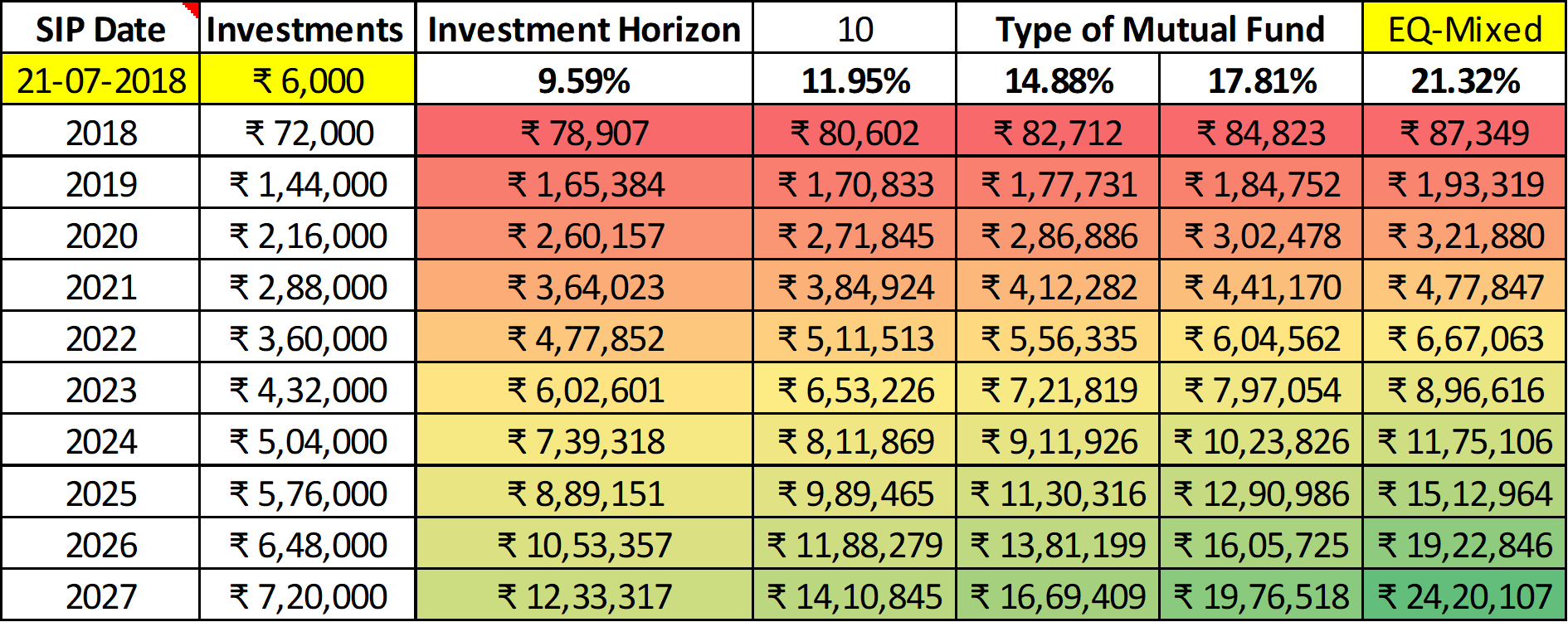

How Returns Are Calculated in SIP

SIP Formula Highlights:

- Monthly investment

- NAV at each purchase

- Units accumulated over time

SIP returns are measured by XIRR (Extended Internal Rate of Return).

Example table:

| Year | Amount Invested | NAV | Units |

|---|---|---|---|

| Year 1 | ₹60,000 | 20 | 3000 |

| Year 2 | ₹60,000 | 25 | 2400 |

| … | … | … | … |

Best SIP Plans for 5 Years (2026)

1. Large Cap Mutual Funds (Safe & Stable)

Large cap funds invest in big, established companies with strong growth records.

Best Picks:

- SBI Bluechip Fund

- HDFC Top 100 Fund

- ICICI Pru Focused Bluechip Fund

Why choose them?

✔ Lower volatility

✔ Good long-term CAGR

✔ Strong portfolio management

Expected 5-year returns: 9% – 14% p.a.

2. Flexi-Cap Funds (Balanced Growth)

Flexi-Cap funds can invest in small, mid, or large cap stocks based on market conditions.

Top Choices:

- Parag Parikh Flexi Cap Fund

- Kotak Flexi Cap Fund

- Axis Flexi Cap Fund

Why choose them?

✔ Flexible allocation

✔ Better risk–adjusted returns

✔ High growth potential

Expected 5-year returns: 11% – 16% p.a.

3. Mid Cap SIP Funds (Growth Focused)

Mid caps can offer higher returns — but with slightly higher risk.

Best SIP Mid Cap Funds:

- DSP Mid Cap Fund

- HDFC Mid Cap Opportunities

- Axis Mid Cap Fund

Why choose them?

✔ Aggressive growth

✔ Excellent for 5+ years

Expected 5-year returns: 12% – 18% p.a.

4. Multi-Cap Funds (Diversified Growth)

Multi-cap funds spread investments across all cap segments.

Top Funds:

- Motilal Oswal Multi-Cap 35

- UTI Multi Cap Fund

- Aditya Birla Sun Life Multi Cap

Expected returns: 10% – 15% p.a.

5. ELSS Tax Saving Funds (Tax + Growth)

If you want tax benefits (₹1.5L per year), ELSS is best.

Strong Performers:

- Axis Long Term Equity Fund

- Mirae Asset Tax Saver

- Canara Robeco Equity Tax Saver

Lock-in: 3 years (but usable in 5-year SIP strategy)

Expected returns: 12% – 17% p.a.

Comparison Table: Best SIP Plans for 5 Years

| Fund Type | Risk | Avg Returns | Ideal For |

|---|---|---|---|

| Large Cap | Low–Medium | 9%–14% | Stability |

| Flexi Cap | Medium | 11%–16% | Balanced growth |

| Mid Cap | Medium–High | 12%–18% | Higher returns |

| Multi Cap | Medium | 10%–15% | Diversified growth |

| ELSS | Medium | 12%–17% | Tax saving + growth |

Choosing the Right SIP: Checklist

Before investing:

✔ Understand your risk profile

✔ Check expense ratio (<2%)

✔ Compare 5-year history

✔ Look at fund manager track record

✔ Avoid recent underperformers

SIP Mistakes to Avoid

❌ Choosing funds on past 1-year returns only

❌ Switching funds too often

❌ Ignoring expense ratio

❌ Not reviewing portfolio annually

❌ Investing without goals

How to Review Your SIP Portfolio

Annual review:

- Check returns vs benchmark

- Rebalance if large imbalance

- Add more when markets dip (opportunity)

Never react emotionally to market corrections.

SIP Strategy for Different Goals

Goal: Home Down Payment (5 Years)

- Large cap + Multi cap

- SIP amount: ₹10,000–₹30,000/month

Goal: Child Education (5 Years)

- Flexi cap + ELSS

- SIP: ₹5,000–₹20,000/month

Goal: Travel & Lifestyle

- Balanced basket

- SIP: ₹5,000–₹15,000/month

SIP Returns Illustration (5 Years)

| Monthly SIP | Total Invested | Estimated Corpus (12% CAGR) |

|---|---|---|

| ₹5,000 | ₹300,000 | ~₹418,000 |

| ₹10,000 | ₹600,000 | ~₹836,000 |

| ₹20,000 | ₹1,200,000 | ~₹1,672,000 |

Compounding boosts long-term wealth.

SIP in Down Markets: Why It Works

During corrections:

✔ You buy more units at lower NAV

✔ Rupee cost averaging benefits

✔ Better long-term returns

That’s the power of SIP discipline.

Risk vs Return in SIP Funds

Understand risk:

- Large cap = stable

- Mid cap = higher returns, higher volatility

- ELSS = lock-in + good tax benefit

Choose based on patience and risk tolerance.

Tax Implications of SIP in India

- ELSS: 3-year lock-in, tax benefit under Section 80C

- Others:

- Short-term capital gains (STCG)

- Long-term capital gains (LTCG) tax

Understanding tax improves net returns.

When to Increase Your SIP Contribution

Increase SIP when:

✔ Salary increases

✔ Market dips

✔ New financial goal

✔ Rebalancing required

This accelerates wealth building.

Step-by-Step: How to Start a SIP

- Select platform (AMC/online app)

- Complete KYC

- Choose fund(s)

- Decide SIP amount & date

- Start SIP

- Review annually

Modern apps make SIP start in minutes.

SIP vs Lump Sum (What’s Better?)

- SIP: Rupee cost averaging, disciplined

- Lump sum: If you have big capital during a dip

Both have roles, but SIP reduces timing risk.

How Market Volatility Benefits a 5-Year SIP

Many investors fear market ups and downs. But SIP investors benefit from volatility through rupee cost averaging.

When markets fall:

✔ You buy more units at lower prices

✔ Future gains increase

When markets rise:

✔ Existing units grow in value

Over 5 years, this averaging reduces risk compared to lump-sum investing.

Ideal Asset Allocation for a 5-Year SIP

A balanced mix works best:

| Allocation | Fund Type | Purpose |

|---|---|---|

| 40% | Large Cap | Stability |

| 30% | Flexi Cap | Balanced growth |

| 20% | Mid Cap | Higher returns |

| 10% | ELSS / Thematic | Tax benefit or opportunity |

This reduces downside risk while maintaining growth potential.

SIP vs Recurring Deposit (RD)

| Feature | SIP | RD |

|---|---|---|

| Returns | Market-linked | Fixed |

| Risk | Medium | Low |

| Inflation Protection | Yes | No |

| Potential Growth | High | Limited |

SIP is better for wealth growth over 5 years.

Power of Increasing SIP (Step-Up SIP)

Instead of fixed SIP, increase by 5–10% annually.

Example:

₹10,000/month → increase ₹1,000 yearly

This dramatically boosts corpus in 5 years.

Performance Review Timeline

| Time | Action |

|---|---|

| Year 1 | Check consistency |

| Year 2–3 | Compare with benchmark |

| Year 4 | Rebalance |

| Year 5 | Plan withdrawal strategy |

Avoid reviewing too frequently.

Withdrawal Strategy After 5 Years

When goal is reached:

✔ Use STP (Systematic Transfer Plan) to shift to safer funds

✔ Avoid withdrawing entire amount during market dips

Gradual exit protects gains.

How SIP Helps Beat Inflation

Inflation in India averages ~6%.

Bank deposits may not beat inflation, but equity SIPs historically do over medium term.

Risk Factors to Consider

- Economic slowdown

- Interest rate hikes

- Global market corrections

Diversification across fund categories helps manage this.

SIP for Salaried vs Business Individuals

| Investor Type | Strategy |

|---|---|

| Salaried | Fixed monthly SIP |

| Business | Flexible SIP, increase in good months |

Emotional Discipline in SIP

Successful SIP investors:

✔ Ignore short-term noise

✔ Stay invested during crashes

✔ Think long-term

Patience = higher returns.

Safety Tips for SIP Investing

✔ Use direct plans to reduce expense ratio

✔ Invest only through SEBI-registered platforms

✔ Avoid NFO hype

✔ Track fund manager changes

SIP Success Story Example

₹8,000/month SIP for 5 years at 13% return →

Invested: ₹4.8 lakh

Corpus: ~₹6.7 lakh

Shows compounding power.

How Different Market Phases Affect a 5-Year SIP

Over a 5-year period, markets go through:

- Bull phases (rising markets)

- Corrections

- Sideways movements

SIP performs well across cycles because:

✔ More units are bought during downturns

✔ Long-term average price benefits

Timing becomes less important than consistency.

SIP Portfolio Rebalancing Strategy

As markets move, allocations change.

Example:

Mid-cap fund grows faster → portfolio risk increases.

Solution:

✔ Reduce exposure to overweight category

✔ Add to underperforming but strong category

Rebalance every 12–18 months.

How Expense Ratio Impacts SIP Returns

Lower expense ratio = higher net return.

| Expense Ratio | Impact Over 5 Years |

|---|---|

| 2.0% | Lower corpus |

| 1.0% | Significantly higher |

Choose direct plans whenever possible.

SIP for Goal-Based Investing

A 5-year SIP is perfect for:

✔ Car purchase

✔ Marriage fund

✔ Foreign trip

✔ Business capital

✔ Emergency corpus growth

Goal-based investing improves discipline.

SIP Top-Up Strategy

Every year, increase SIP amount by 5–15%.

Even small increases dramatically improve the corpus.

What to Do If Market Falls in Year 4–5

Do NOT panic.

✔ Continue SIP

✔ Avoid redemption during dips

✔ Shift gradually to safer funds if goal is near

Direct vs Regular SIP

| Type | Expense | Return |

|---|---|---|

| Direct Plan | Lower | Higher |

| Regular Plan | Higher | Lower |

Direct plans are better for long-term SIP investors.

SIP Risk Management Techniques

✔ Diversify across fund categories

✔ Avoid overexposure to small caps

✔ Review portfolio annually

✔ Keep emergency funds separate

Psychological Edge of SIP Investors

SIP reduces emotional investing because:

✔ You invest automatically

✔ No market timing pressure

✔ Long-term mindset builds confidence

When to Stop or Modify SIP

Consider modification if:

- Fund underperforms consistently for 2+ years

- Fund manager changes with poor track record

- Goal timeline changes

SIP vs PPF (5-Year View)

| Feature | SIP | PPF |

|---|---|---|

| Return | Market-based | Fixed |

| Risk | Medium | Very low |

| Inflation beating | Yes | Limited |

SIP better for growth; PPF for safety.

Frequently Asked Questions (FAQs)

Q1. Which SIP is best for 5 years in India?

Flexi cap and mid cap funds often outperform over a 5-year horizon with disciplined SIP.

Q2. Do SIP returns depend on market?

Yes, but SIP reduces timing risk.

Q3. Can I stop SIP anytime?

Yes, SIP is flexible without penalty (except ELSS lock-in).

Q4. Is SIP safe?

SIP helps reduce volatility risk, but fund choice determines overall risk

Q5. How much should I start with?

Minimum SIP starting can be as low as ₹500/month, but higher amounts build corpus faster.

Final Thoughts

A 5-year SIP in India is one of the most practical ways to build wealth with controlled risk. The key elements for success are:

✔ Discipline

✔ Long-term perspective

✔ Proper diversification

✔ Regular reviews

Stay invested, be patient, and let compounding work for you.

Also read: Top 10 SIP plans in India

Also read: Top 10 Mutual Funds in India

2 thoughts on “10 Best SIP Plans for 5 Years in India (2026) – Top Mutual Funds for High Returns”