If your personal loan application status shows “under review”, it means the lender is still evaluating your financial profile before making a final decision. Read more about “Why Personal Loan Application Is Under Review”.

When you apply for a loan, banks do not approve it immediately. Instead, they conduct several background checks to determine whether you are capable of repaying the loan. During this verification stage, your application may temporarily show the status “under review.”

This stage allows the lender to check:

- Your credit score and credit history

- Your income stability

- Your existing loans and EMIs

- Your identity and KYC verification

- Fraud detection signals

- Risk scoring results

For many borrowers, seeing the “under review” status can be confusing and stressful. However, it is important to understand that this stage is a normal part of the loan approval process.

In most cases, the review process takes between 24 hours and 5 working days, although it may sometimes take longer depending on the lender and your financial profile.

Quick Decision Box

If your personal loan application is under review, it usually means the lender is still verifying your financial information before approving the loan.

The most common reasons include:

- Credit score verification

- Income validation

- Existing loan obligations

- Employment stability checks

- Identity verification

- Fraud detection screening

- Manual risk assessment

This status does not mean your loan is rejected. It simply means the lender needs more time to analyze your profile.

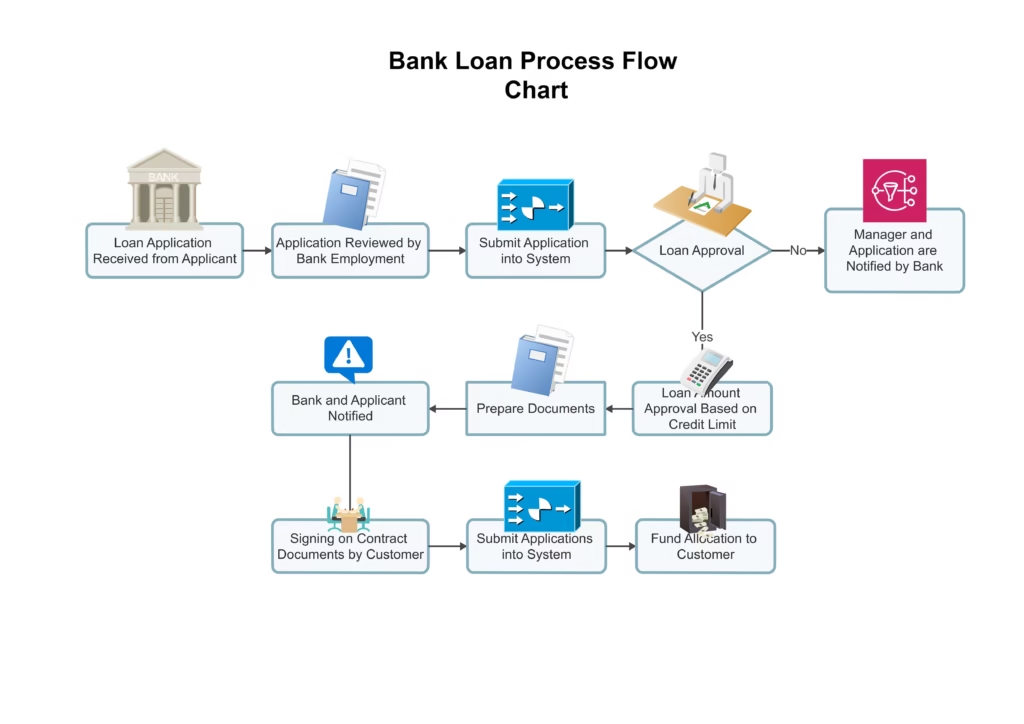

How the Personal Loan Approval Process Works

To understand why applications go under review, it is important to know how banks process loan applications.

When you apply for a personal loan, the lender follows a structured evaluation process.

| Step | What Happens |

|---|---|

| Application Submission | Borrower fills loan application |

| Credit Check | Bank reviews credit history |

| Income Verification | Salary or income documents verified |

| Risk Assessment | Bank calculates borrower risk |

| Final Decision | Loan approved or rejected |

The “under review” stage usually occurs between credit verification and final approval.

During this period, the lender may run multiple checks to confirm the accuracy of your information.

11 Real Reasons Your Personal Loan Is Under Review

Below are the most common reasons lenders place loan applications under review.

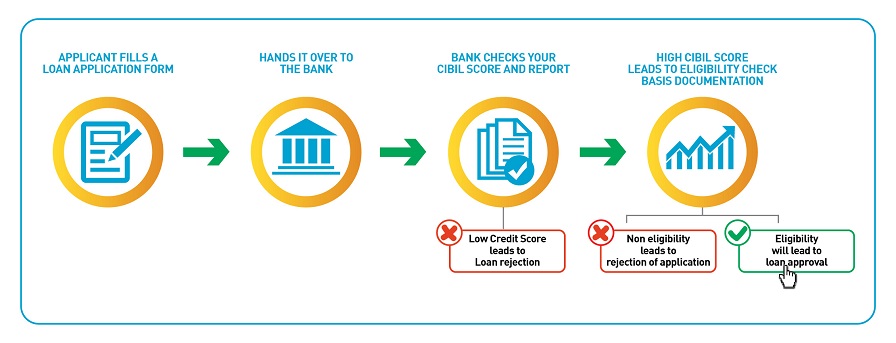

1. Credit Score Verification

One of the first things banks evaluate is your credit score and credit history.

Your credit score reflects how responsibly you have handled previous loans and credit cards.

Typical ranges:

| Credit Score | Loan Approval Chances |

|---|---|

| 750+ | Very High |

| 700–750 | High |

| 650–700 | Moderate |

| Below 650 | Low |

If your credit score falls between 650 and 700, lenders often perform additional verification before approving the loan.

2. Income Verification

Banks must confirm whether your income is sufficient to repay the loan.

To do this, they check:

- Salary slips

- Bank statements

- Income tax returns

- Employment records

If there is any mismatch between your declared income and actual bank transactions, your application may remain under review longer.

3. High Existing Loan Burden

Lenders evaluate your Debt-to-Income Ratio (DTI).

This ratio measures how much of your monthly income is already used to pay EMIs.

For example:

| Monthly Income | Existing EMIs | Risk Level |

|---|---|---|

| ₹50,000 | ₹10,000 | Low |

| ₹50,000 | ₹25,000 | Moderate |

| ₹50,000 | ₹35,000 | High |

If your EMI obligations are already high, lenders may review the application carefully before approving another loan.

4. Employment Stability Check

Lenders prefer borrowers with stable employment history.

If you have:

- recently changed jobs

- started a new business

- switched to freelancing

the lender may conduct additional checks before approving your loan.

Stable employment signals lower repayment risk.

5. Identity Verification

Banks must verify your KYC (Know Your Customer) documents.

Common documents include:

- Aadhaar Card

- PAN Card

- Address proof

- Bank account verification

If there is any mismatch between your documents and application details, your loan may remain under review.

6. Bank Statement Analysis

Banks analyze your last 3–6 months of bank statements.

They review:

- Salary deposits

- Spending behavior

- Bounced transactions

- Balance stability

Frequent cheque bounces or irregular deposits can increase risk and trigger further review.

7. Internal Risk Scoring System

Most lenders use automated risk scoring systems to evaluate borrowers.

These systems analyze:

- credit score

- employment stability

- transaction patterns

- debt obligations

If the algorithm cannot clearly approve or reject the application, it sends it for manual review.

8. Fraud Detection Screening

Banks run fraud detection systems to protect against identity theft and fake loan applications.

These systems detect unusual patterns such as:

- suspicious device usage

- mismatched identity details

- multiple loan applications

If anything looks suspicious, the application may stay under review.

9. Large Loan Amount Request

Higher loan amounts increase the lender’s risk exposure.

For example:

| Loan Amount | Risk Level |

|---|---|

| ₹50,000 | Low |

| ₹2,00,000 | Moderate |

| ₹10,00,000 | High |

Large loans require deeper verification before approval.

10. Verification Call Pending

Many lenders conduct verification calls before approving loans.

During these calls, they confirm:

- employment details

- salary information

- loan purpose

If the bank cannot reach you, your loan may remain under review.

11. Manual Review by Credit Team

Sometimes automated systems cannot make a clear decision.

In such cases, the credit risk team manually reviews the application.

This review helps the bank decide whether the loan can still be approved safely.

MaintainMarket Insight

Many borrowers panic when they see “loan under review” in their application status.

However, in many situations this actually means your profile is close to approval but needs additional verification.

Borrowers with moderate credit scores (650–700) or recent job changes are the most commonly reviewed applicants.

Real Case Study

Rahul, a salaried employee from Mumbai, applied for a ₹3 lakh personal loan through an online lender.

His credit score was 670, which is acceptable but not excellent.

The lender placed his application under review to verify:

- employment details

- salary stability

- repayment capacity

After two days of verification and a confirmation call, the lender approved the loan successfully.

This example shows that review does not necessarily mean rejection.

How Long Does Loan Under Review Status Last?

The review period varies depending on the type of lender.

| Lender Type | Review Time |

|---|---|

| Online loan apps | 24–48 hours |

| Private banks | 2–3 days |

| NBFC lenders | 2–4 days |

| Public sector banks | 3–7 days |

If your application remains under review for more than 7 days, you should contact the lender to check the status.

What You Should Do If Your Loan Is Under Review

If your loan application is under review, follow these steps to avoid delays.

1. Answer Verification Calls

Banks often call to confirm your employment and income.

2. Keep Documents Ready

You may need to provide additional documents such as salary slips or bank statements.

3. Monitor Email and Messages

Lenders may request extra documents through email or SMS.

4. Avoid Multiple Loan Applications

Applying for several loans at the same time can reduce your credit score.

5. Maintain Account Balance

Ensure your bank account has a stable balance during verification.

These steps can increase the chances of faster approval.

Signs Your Loan May Get Approved Soon

Some positive indicators include:

- Verification calls completed

- Documents successfully verified

- No additional documents requested

- Credit score above 700

If these conditions are met, approval is likely.

When Should You Worry?

In some cases, the review stage may lead to rejection.

Possible warning signs include:

- credit score below 600

- very high existing loan burden

- inconsistent income records

- failed verification calls

If these factors apply, the lender may reject the application.

Lender Psychology Explained

Banks aim to reduce the risk of loan default.

Instead of rejecting borderline applicants immediately, they review the application carefully.

This approach allows lenders to:

- approve more borrowers

- reduce financial risk

- maintain portfolio quality

From a bank’s perspective, reviewing applications improves loan decision accuracy.

What Happens During the Loan Review Stage?

When your personal loan application enters the review stage, several backend checks are performed by the lender’s risk management system.

During this stage, banks evaluate different aspects of your financial behavior to determine whether lending money to you is safe.

Some of the key checks include:

Credit Bureau Verification

The lender verifies your credit history through credit bureaus such as:

- CIBIL

- Experian

- Equifax

- CRIF High Mark

These reports show your previous loans, repayment history, and credit utilization.

Document Authenticity Check

Banks verify whether your submitted documents are genuine.

They check:

- Salary slips

- Bank statements

- PAN card details

- Address verification

If any document appears suspicious or incomplete, the review stage may take longer.

Financial Stability Analysis

Lenders also examine your financial stability.

They analyze:

- income consistency

- savings habits

- monthly expenses

- existing liabilities

Borrowers with stable financial patterns usually pass the review stage faster.

Common Mistakes That Cause Loan Review Delays

Many borrowers unknowingly make mistakes while applying for loans. These mistakes can cause lenders to keep the application under review for longer periods.

Incorrect Personal Details

If your application contains errors such as:

- incorrect address

- wrong phone number

- mismatched PAN details

the lender may need additional verification.

Applying for Multiple Loans

Submitting loan applications to several lenders simultaneously can reduce your credit score.

Each loan application generates a hard inquiry, which may increase risk signals for lenders.

Incomplete Documents

Sometimes borrowers upload incomplete documents during the application process.

Examples include:

- missing salary slips

- unclear identity proof

- incomplete bank statements

Incomplete documentation often causes delays.

How to Speed Up Personal Loan Approval

If your loan is currently under review, there are steps you can take to improve approval chances.

Maintain a Good Credit Score

A credit score above 750 significantly increases approval chances and reduces review time.

You can improve your credit score by:

- paying EMIs on time

- reducing credit card balances

- avoiding loan defaults

Submit Accurate Documents

Ensure that all documents submitted during the loan application process are:

- clear

- complete

- up to date

Providing accurate documents helps the lender complete verification faster.

Stay Available for Verification Calls

Banks may contact you to confirm details about:

- your job

- salary

- employer

- loan purpose

Missing verification calls can delay approval.

Can a Loan Be Approved After Being Under Review?

Yes, many personal loan applications are approved after the review stage.

In fact, the review stage often indicates that the lender is carefully evaluating the application instead of rejecting it immediately.

If your profile meets the lender’s requirements, the application may move from “under review” to “approved” within a few days.

Situations Where Loan Under Review May Turn Into Rejection

Although many applications are approved, some may eventually be rejected.

Common reasons include:

- very low credit score

- inconsistent income records

- negative credit history

- high debt-to-income ratio

If the lender determines that the borrower may struggle to repay the loan, they may reject the application.

Difference Between Loan Processing and Loan Under Review

Many borrowers confuse these two terms.

Here is a simple comparison.

| Loan Processing | Loan Under Review |

|---|---|

| Application is being prepared | Application is being evaluated |

| Basic verification stage | Advanced risk assessment |

| Early stage | Mid approval stage |

Understanding this difference can help borrowers track the loan status more accurately.

How to Check Personal Loan Application Status

Most lenders allow borrowers to track their loan application status online.

You can check your status through:

Bank Website

Log into the lender’s official website using your application number.

Mobile Banking App

Many banks provide loan tracking features through their mobile apps.

Customer Support

You can also contact the lender’s customer care team for updates.

Can You Cancel a Personal Loan Application During Review?

Yes, borrowers can cancel their loan application while it is under review.

However, it is important to consider a few factors:

- Some lenders may record the application in your credit history.

- Multiple cancellations can affect your future loan applications.

Before cancelling, it is best to confirm whether the loan will likely be approved.

Tips to Improve Personal Loan Approval Chances

If you are planning to apply for a personal loan, these tips can increase your chances of approval.

Maintain Low Credit Utilization

Keep your credit card usage below 30% of the credit limit.

Avoid Loan Defaults

Late payments and defaults can significantly reduce approval chances.

Increase Income Stability

Borrowers with consistent income records are considered lower risk.

Choose the Right Loan Amount

Requesting a loan amount that matches your income level improves approval probability.

Future of Digital Personal Loan Approval (2026 and Beyond)

With the advancement of financial technology (FinTech), loan approval systems are becoming more automated.

Modern lenders use:

- artificial intelligence

- machine learning algorithms

- real-time financial data

These technologies help banks evaluate loan applications faster while reducing fraud risk.

As digital lending grows, the review stage may become shorter and more efficient.

Related Articles You Should Read

To understand personal loan approval better, read these guides:

- Why Personal Loan Gets Rejected After Pre Approval

- Personal Loan Verification Call Questions

- Minimum Credit Score for Personal Loan Approval

These resources explain the complete loan approval system used by lenders.

Frequently Asked Questions About Why Personal Loan Application Is Under Review

Q1. Does loan under review mean rejection?

No. It simply means the lender is still verifying your profile before making the final decision.

Q2. How long does loan review take?

The review stage usually lasts 24 hours to 5 working days, depending on the lender.

Q3. Can I cancel a loan application while it is under review?

Yes. You can cancel the application before the loan is approved or disbursed.

Q4. Should I apply for another loan while my application is under review?

No. Multiple loan applications can reduce your credit score and decrease approval chances.

Final Action Plan

If your personal loan application is under review, follow this action plan:

- Wait 2–3 working days for verification.

- Respond to lender verification calls quickly.

- Provide additional documents if requested.

- Ensure all personal details are accurate.

- Avoid applying for multiple loans simultaneously.

In many cases, applications under review are approved after verification is completed.