Why your loan or credit card is getting rejected in 2026 even with a good credit score. Learn the new rules, hidden checks, and what to do now.

Introduction

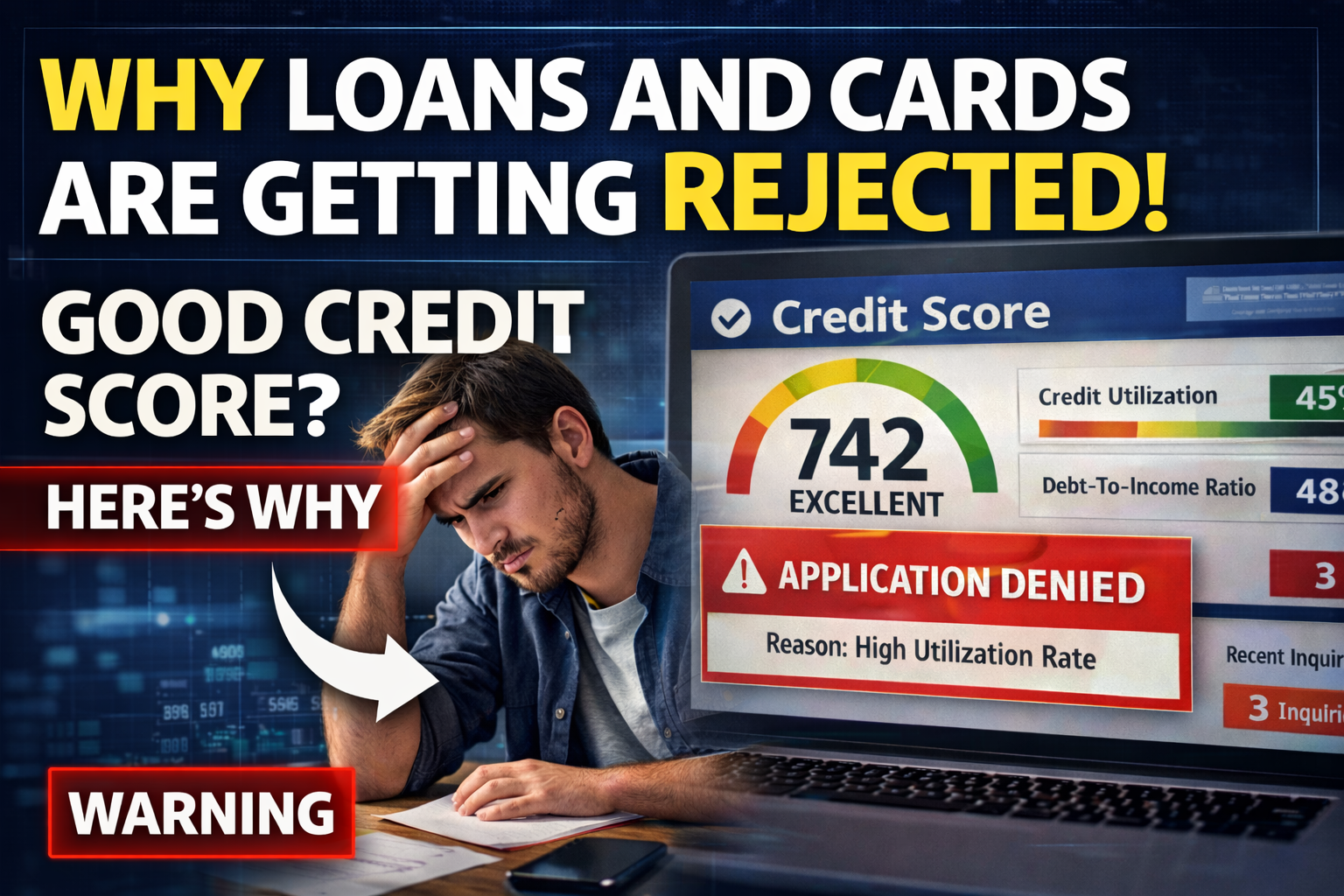

You have a good FICO score. You pay your bills on time. Still, your loan or credit card gets rejected.

It’s frustrating. You expected approval, but instead you get a decline or a high APR offer.

Across the US, borrowers with 700+ credit scores are facing unexpected denials due to stricter bank policies and hidden risk checks in 2026.

Quick Update Box

What changed:

Banks are using stricter underwriting, AI risk scoring, and income stability checks

Who is affected:

Good credit users, gig workers, high utilization users, new credit applicants

What to do immediately:

Lower utilization, avoid multiple applications, check income consistency, review full credit report

1. What’s Happening Right Now

In 2026, US banks and lenders have quietly tightened approval rules. This is not officially announced everywhere, but the impact is real.

Loan rejection rates have increased, especially for:

- Personal loans

- Credit cards with high limits

- Balance transfer cards

Even users with strong credit scores (680–780 range) are facing:

- Instant rejection

- Lower credit limits

- Higher interest rates

This shift is happening because lenders are preparing for potential economic slowdown, rising defaults, and unstable borrower behavior patterns.

In simple terms:

Your credit score alone is no longer enough.

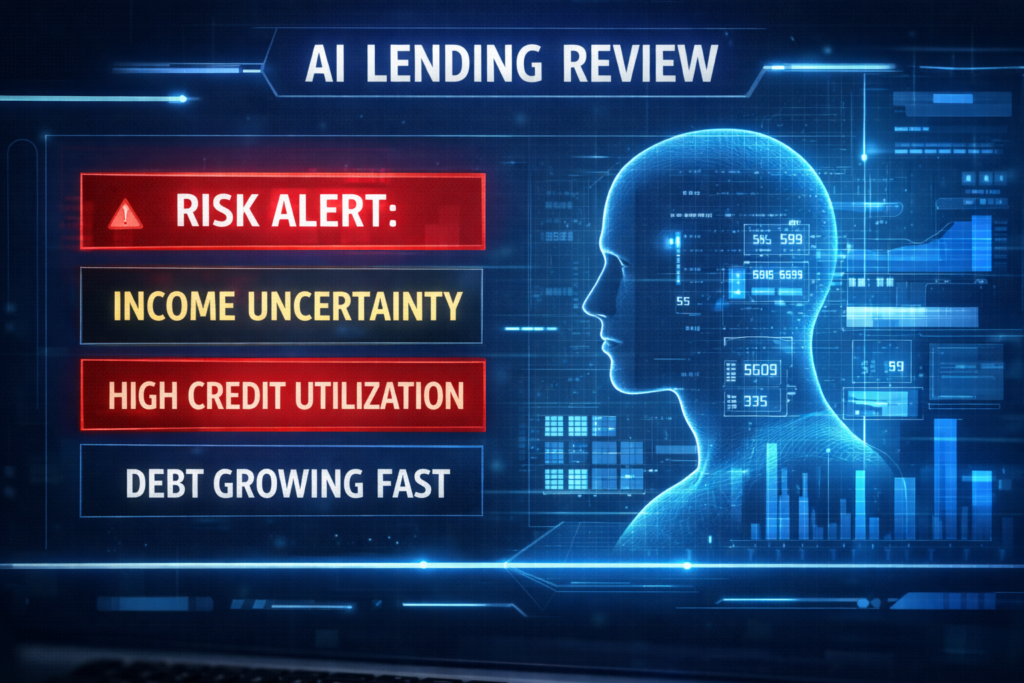

2. Why This Is Happening (The Real System Behind It)

1. Banks Are Predicting Risk, Not Just Measuring It

Earlier, lenders focused on past behavior (credit score).

Now, they focus on future risk prediction using:

- Spending patterns

- Income consistency

- Job stability

- Debt growth trends

2. AI-Based Underwriting

Banks are using AI models that analyze:

- Transaction behavior

- Credit usage spikes

- Hidden financial stress signals

Even if your score is good, your behavior might signal risk.

3. Rising Credit Card Debt in the US

Americans are carrying record-high credit card balances.

This makes lenders cautious because:

- More debt = higher default risk

- High utilization = financial stress

4. Interest Rate Pressure

Higher interest rates mean:

- Loans are costlier

- Defaults are more likely

So banks are rejecting borderline applicants to reduce risk exposure.

3. Who Is Affected the Most

Not everyone is affected equally.

Most impacted groups:

1. Gig Workers / Freelancers

Irregular income = higher perceived risk

2. High Credit Utilization Users

Even 30–50% utilization can trigger rejection

3. Recent Credit Applicants

Multiple applications = “credit hungry” signal

4. Thin Credit File Users

Good score but low history = low trust

5. Users With Rising Debt Trend

Even if payments are on time

4. Real Impact on Users

This change is not small. It directly affects your money.

What users are experiencing:

- Loan rejection despite 720+ score

- Credit card approval with very low limits

- High APR (20–30%) even for good profiles

- Hard inquiries damaging credit further

Financial consequences:

- Delayed financial goals

- Increased borrowing costs

- More dependence on expensive credit

5. What You Should Do Now

If you want approval in 2026, you must adapt.

Step 1: Reduce Credit Utilization

Keep it below 30%, ideally below 20%

Step 2: Avoid Multiple Applications

Wait at least 3–6 months between applications

Step 3: Show Stable Income

Even side income should look consistent

Step 4: Pay More Than Minimum

Signals financial strength

Step 5: Check Your Full Credit Report

Not just score—look for:

- Errors

- Old collections

- Sudden balance spikes

6. Comparison Table (Before vs After 2026 Changes)

| Factor | Before 2026 | After 2026 |

|---|---|---|

| Credit Score Importance | High | Moderate |

| Income Stability | Less important | Very important |

| AI Risk Analysis | Limited | Strong |

| Approval Rate | Easier | Stricter |

| Credit Utilization Impact | Medium | High |

| Application Sensitivity | Low | High |

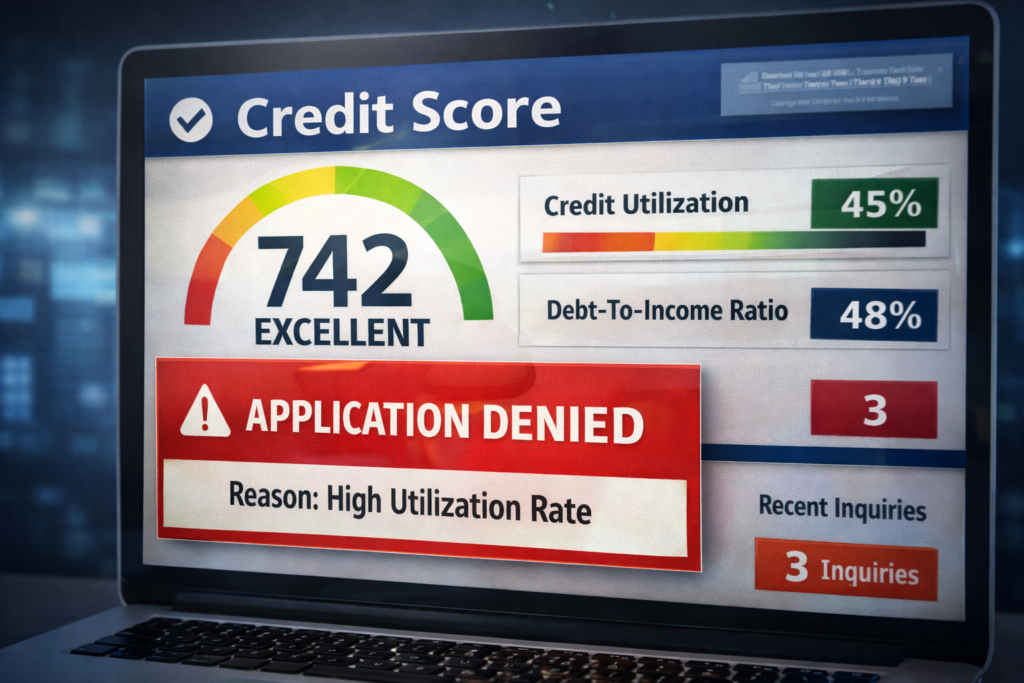

7. Real-Life Example

John, a 29-year-old from Texas:

- Credit Score: 742

- Income: $60,000

- Applied for a credit card

Result: Rejected

Why?

- 45% credit utilization

- 3 applications in last 2 months

- Increasing monthly balances

Even with a good score, the system flagged him as “rising risk.”

8. Mistakes to Avoid

1. Applying Multiple Times After Rejection

This worsens your profile

2. Ignoring Credit Utilization

Biggest hidden rejection factor

3. Relying Only on Credit Score

Score is just one piece

4. Closing Old Credit Cards

Reduces credit history

5. Taking Buy Now Pay Later Excessively

Signals hidden debt

9. Expert Insights (Hidden Truth)

Banks don’t reject you because of your past.

They reject you because of your future risk signal.

Key hidden factors:

- Are your balances increasing?

- Are you relying more on credit monthly?

- Is your income stable or fluctuating?

This is called behavioral risk scoring.

Even if your score is good, your behavior may not be.

10. Future Prediction

What will happen next:

- Even stricter approvals in 2026–2027

- More AI-based lending decisions

- Lower credit limits for new users

- Higher importance of income verification

In short:

Getting approved will become harder unless you optimize your financial profile.

11. Hidden Factors Banks Are Checking in 2026 (Most People Don’t Know)

These are the silent killers of your approval chances:

1. Banking Behavior (Not Just Credit Report)

Banks now analyze:

- How often your balance goes near zero

- Frequency of withdrawals

- Salary consistency

If your account looks unstable → rejection risk increases

2. Subscription Load & Monthly Obligations

Netflix, gym, SaaS tools, EMIs—everything matters now

Too many recurring payments =

👉 Less disposable income

👉 Higher perceived risk

3. Sudden Spending Spikes

If your spending jumps suddenly:

- Travel

- Electronics

- Large purchases

AI systems flag this as:

“Possible financial stress or lifestyle inflation”

4. Dormant Credit Accounts

If you have old credit cards but don’t use them:

- Banks can’t track behavior

- Your “active profile” becomes weak

5. Geographic Risk Profiling

Some US regions are currently flagged as higher default zones

Even if your profile is good:

👉 Location can slightly impact approval

12. Advanced Approval Strategy (Used by Smart Borrowers)

This is what actually works in 2026:

Strategy 1: Pre-Qualification First

Never apply directly

Use soft-check tools from:

- Discover

- Capital One

- Chase

👉 No hard inquiry

👉 Higher approval chances

Strategy 2: Credit Timing Optimization

Apply when:

- Utilization is low (right after bill payment)

- No recent inquiries (last 3 months clean)

Timing alone can increase approval chances by 20–30%

Strategy 3: Balance Distribution Trick

Instead of:

- 1 card = 80% usage

Do:

- 4 cards = 20% each

👉 Looks safer to lenders

Strategy 4: Increase “Financial Stability Signals”

Before applying:

- Keep bank balance stable for 60–90 days

- Avoid large withdrawals

- Show consistent deposits

13. Psychological Triggers Lenders Use (Very Important)

Banks don’t think like humans—they think like risk machines.

They look for patterns like:

- “Is this person becoming dependent on credit?”

- “Is their lifestyle growing faster than income?”

- “Are they preparing for financial stress?”

Even small signals like:

- Increasing minimum payments

- Frequent small borrowings

👉 Can reduce your approval chances

14. Soft Rejection vs Hard Rejection (Big Difference)

Soft Rejection (Hidden)

You are approved BUT:

- Very low limit

- Very high APR

👉 This is still a rejection in disguise

Hard Rejection

- Application declined

- Hard inquiry added

What it means:

If you’re getting:

- $500 limit on a good profile

👉 System doesn’t trust you fully

15. Debt-to-Income Ratio (DTI) – The Silent Killer

Most users ignore this completely.

Ideal DTI in 2026:

- Below 36% = Safe

- 36%–50% = Risky

- Above 50% = High rejection chances

Example:

Income: $5,000/month

Debt payments: $2,500

DTI = 50%

👉 Even with 750 score → possible rejection

16. New Credit Card Approval Trends in 2026

Trend 1: Lower Initial Limits

Banks are starting low and increasing later

Trend 2: Relationship-Based Approvals

If you already bank with them → higher chances

Trend 3: Tiered Risk Pricing

Same card, different APR based on risk

Trend 4: Income Verification Tightening

More lenders asking:

- Bank statements

- Employment proof

17. Red Flags That Instantly Reduce Approval Chances

Avoid these at all cost:

- Maxing out cards before applying

- Applying after missing even one payment

- Using cash advances

- Closing oldest account

- Sudden balance transfers

18. Smart Moves Before Applying (Checklist)

Use this checklist before any application:

✔ Credit utilization below 25%

✔ No new inquiries in last 60 days

✔ Stable income deposits

✔ No late payments (last 12 months)

✔ DTI below 40%

✔ Old accounts active

If you don’t meet at least 4–5 of these → wait

19. How Long This Situation Will Last

This is not temporary.

Expect:

- Strict approvals till at least 2027

- More AI control in lending

- Reduced easy credit access

This is a structural shift, not a short-term change

20. Final Insight (Most Important)

In 2026:

👉 Credit Score = Entry Ticket

👉 Behavior = Final Decision

If you understand this, you’ll win.

If not, you’ll keep getting rejected—even with a “good score.”

Where to Take Action (USA ONLY)

If you’re planning to apply, choose lenders strategically and check eligibility first:

- https://www.discover.com/credit-cards

- https://www.capitalone.com/credit-cards

- https://creditcards.chase.com

- https://www.bankofamerica.com/credit-cards

Apply only when your profile is strong. Avoid trial-and-error applications.

Why MaintainMarket is Different

Most blogs tell you “improve your credit score.”

MaintainMarket focuses on:

- Real approval strategies

- Data-backed insights

- Behavior-based optimization

- Practical steps that increase approval chances

We don’t just explain finance.

We help you get results.

Final Action Plan

What to do today:

- Check your credit report

- Reduce utilization below 30%

- Stop unnecessary applications

What to avoid:

- Multiple credit inquiries

- High revolving balances

- Ignoring income consistency

What to check before applying:

- Debt-to-income ratio

- Recent credit activity

- Bank-specific approval criteria

FAQ – Loan or credit card is getting rejected

Q1. Why am I getting rejected with a 700+ credit score?

Because lenders now evaluate income stability, utilization, and risk patterns beyond just score.

Q2. Does applying multiple times hurt approval chances?

Yes. Multiple inquiries signal financial stress and reduce approval probability.

Q3. What is the ideal credit utilization in 2026?

Below 30%, but under 20% is safer for approvals.

Q4. Are banks using AI for credit decisions?

Yes. Most major lenders use AI-based risk models for approvals.

Q5. Can income type affect loan approval?

Yes. Irregular income (freelancing/gig work) may reduce approval chances.

Q6. How long should I wait after a rejection?

At least 3–6 months before applying again.

People also searched for: Get Emergency Cash with Bad Credit in USA (Proven Hacks)

Also read: Emergency Loan Without Income Proof: How to Get Money Fast When Banks Say No

Get ₹20,000 Instant Loan Without CIBIL Score – Approval Even with Low Income