Struggling with $10K+ credit card debt in 2026? Discover the exact payoff plan, avoid collections, and reduce interest fast with proven US strategies.

Introduction

Your credit card balance keeps growing—even when you’re paying every month.

Interest is eating your money, and minimum payments feel like a trap.

In the U.S., with APRs touching 20–30%, many users are stuck in a debt cycle they can’t escape.

If you have $10,000+ credit card debt in 2026, you’re not alone—but you are at risk if you don’t act strategically.

Quick Action Box

Problem:

High-interest credit card debt ($10K+) with slow payoff

Risk:

Debt doubling, credit score drop, collections

Immediate Action:

Stop minimum-only payments, choose payoff strategy, reduce APR exposure

1. Why People Fall Into Credit Card Debt (US Reality)

This isn’t just overspending. The system itself pushes users into debt.

1. High APR Trap

- Average credit card APR in 2026: 22%–29%

- Even disciplined users struggle to outpace interest

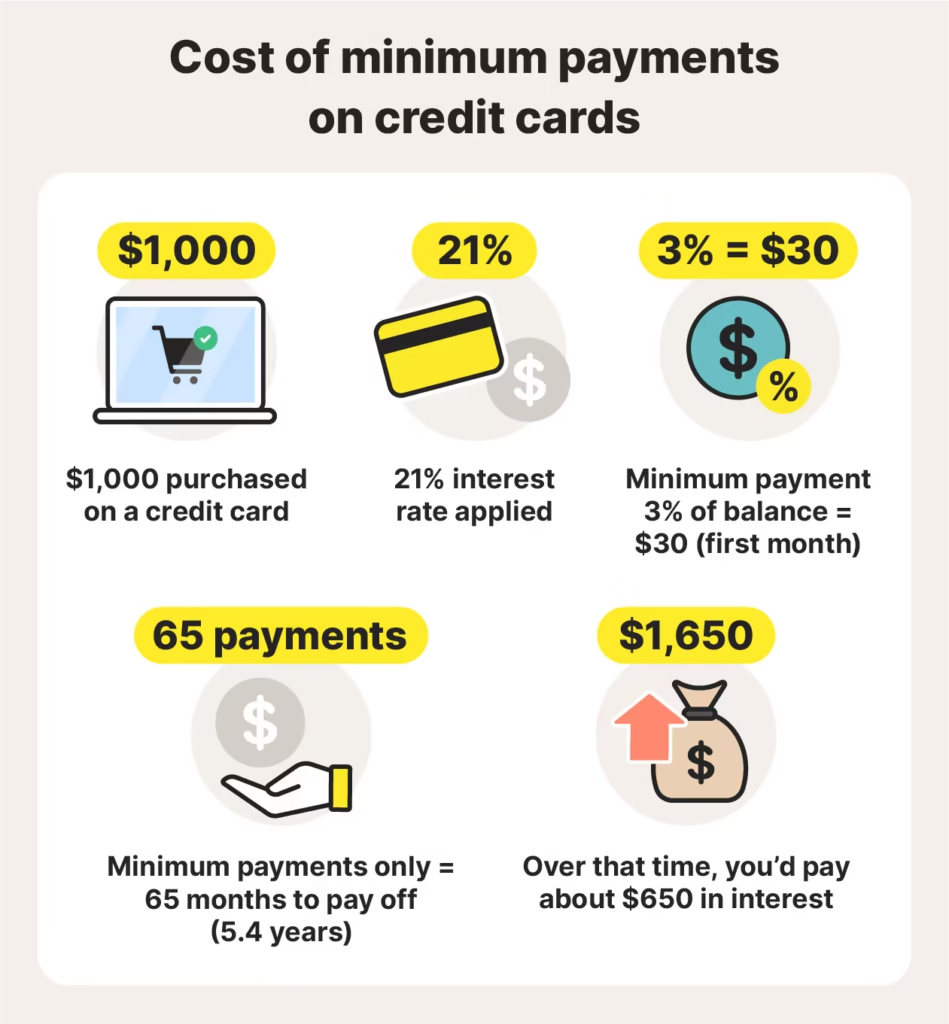

2. Minimum Payment Illusion

Banks design minimum payments to:

- Keep you paying longer

- Maximize interest collection

Example:

- $10,000 debt → $250 minimum

- Actual interest → ~$200/month

👉 You’re barely reducing principal

3. Buy Now Pay Later + Credit Mix

Users combine:

- Credit cards

- BNPL

- Personal loans

Result:

👉 Fragmented debt + no clear strategy

4. Emergency Spending

Medical bills, rent, job loss:

- Credit cards become survival tools

5. Psychological Factor

People think:

“I’ll pay it off later.”

But later = higher interest + deeper trap.

2. Best Credit Card Debt Payoff Strategies (2026)

There is no single “best” method—only what fits your behavior.

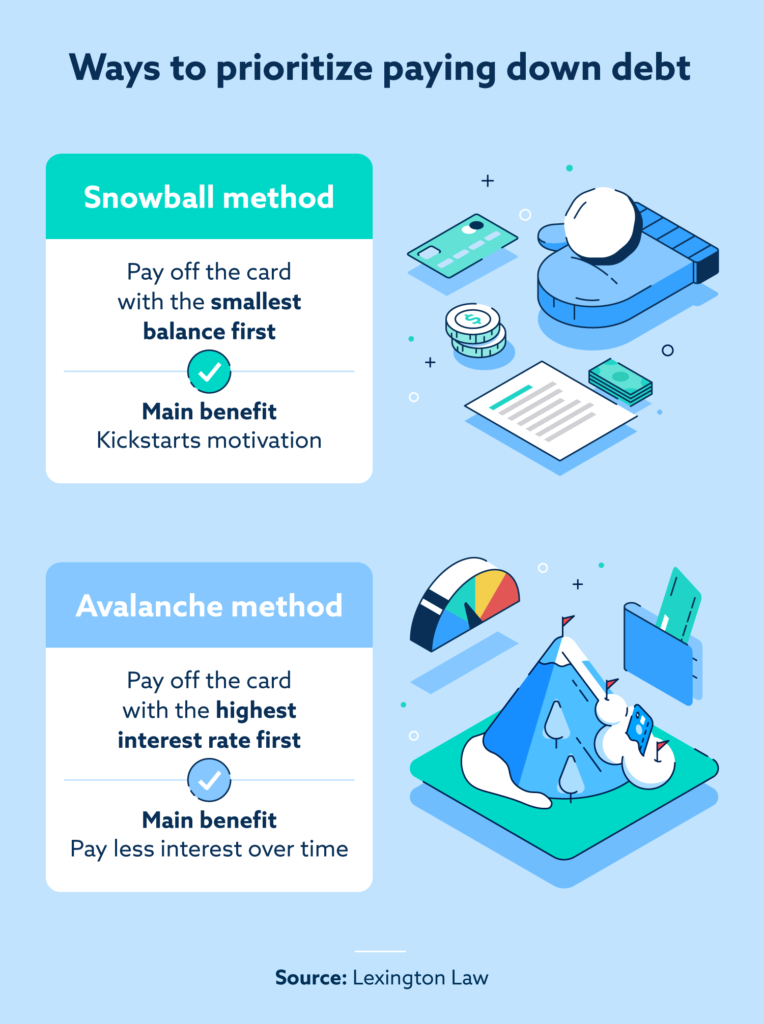

Strategy 1: Debt Snowball (Motivation-Based)

- Pay smallest debt first

- Build psychological wins

Best for:

- Low discipline

- Need quick motivation

Strategy 2: Debt Avalanche (Interest-Based)

- Pay highest APR first

- Save maximum money

Best for:

- Logical thinkers

- Long-term focus

Strategy 3: Balance Transfer (0% APR Hack)

- Transfer debt to 0% APR card

- Save interest temporarily

Best for:

- Good credit score (680+)

Strategy 4: Debt Consolidation Loan

- Combine all debt into one loan

- Lower interest rate

Best for:

- Stable income

- Moderate credit score

Strategy 5: Debt Settlement (Last Option)

- Negotiate lower payoff

- Pay lump sum

Best for:

- Severe financial stress

- Already behind payments

3. Step-by-Step Payoff Plan (Practical Execution)

Step 1: List All Debts

Example:

| Card | Balance | APR | Minimum |

|---|---|---|---|

| Card A | $4,000 | 26% | $120 |

| Card B | $3,500 | 22% | $100 |

| Card C | $2,500 | 29% | $90 |

Step 2: Choose Strategy

If:

- Emotional → Snowball

- Logical → Avalanche

Step 3: Stop New Debt

- Freeze cards if needed

- No new purchases

Step 4: Increase Monthly Payment

Instead of $310 minimum:

👉 Pay $600–$800

Step 5: Automate Payments

- Avoid missed payments

- Improve credit behavior

Step 6: Track Progress Monthly

- Reduce balances

- Monitor utilization

4. Snowball vs Avalanche (Comparison Table)

| Factor | Snowball | Avalanche |

|---|---|---|

| Focus | Smallest debt | Highest interest |

| Motivation | High | Medium |

| Interest Saved | Lower | Highest |

| Speed | Medium | Fastest financially |

| Best For | Beginners | Advanced users |

5. Real-Life Example (USA Case)

Sarah (California):

- Total debt: $12,000

- APR: 24% average

- Income: $3,500/month

Before Strategy:

- Paying minimum → $350

- Debt barely reducing

After Applying Avalanche:

- Monthly payment: $900

- Focused on highest APR

Result:

- Debt cleared in 18 months

- Saved ~$3,200 interest

6. Mistakes That Keep You Stuck in Debt

1. Paying Only Minimum

Biggest trap.

2. Ignoring Interest Rate

APR matters more than balance.

3. Using Card While Paying Debt

Cancels progress.

4. No Clear Strategy

Random payments = no progress.

5. Closing Credit Cards Early

Hurts credit score.

7. Expert Insights (What Most Blogs Don’t Tell You)

Truth 1:

Debt is not a math problem—it’s a behavior problem.

Truth 2:

Consistency beats high payments.

Truth 3:

Interest is your real enemy—not debt amount.

Truth 4:

Banks profit when you stay confused.

8. Timeline: How Fast Can You Get Debt-Free?

| Monthly Payment | Time to Clear $10K | Interest Paid |

|---|---|---|

| $300 | 5+ years | Very high |

| $600 | 2–2.5 years | Moderate |

| $900 | 12–18 months | Low |

9. Strategy Logic (Why This Works)

The system works because:

- You reduce principal faster

- Interest impact drops

- Credit score improves

- Financial stress reduces

It’s not about earning more—it’s about controlling flow.

10. When Debt Becomes Dangerous (Collections Warning)

If you miss payments:

- 30 days → score drops

- 60 days → penalties

- 90+ days → collections

At this stage:

👉 Debt becomes harder to manage

11. Advanced Strategy (For Faster Payoff)

Income Boost Method

- Freelance

- Side hustle

- Sell unused items

Use 100% extra income → debt payoff

Expense Cut Strategy

- Cancel subscriptions

- Reduce discretionary spending

Redirect savings → debt

12. Final Action Plan

Do This Today:

- List all debts

- Choose payoff strategy

- Increase payment

Do This Weekly:

- Track progress

- Adjust payments

Avoid This:

- Minimum-only payments

- New debt

- Random strategy changes

13. Debt Consolidation vs Debt Settlement (Clear Decision Guide)

Most users are confused here—and this confusion costs money.

| Factor | Debt Consolidation | Debt Settlement |

|---|---|---|

| What it does | Combines debt into one loan | Reduces total debt via negotiation |

| Credit Score Impact | Mild (can improve) | Heavy negative impact |

| Interest | Lower than cards | No interest (settled amount) |

| Best For | Stable income users | Financially struggling users |

| Risk | Low | High |

Simple Rule:

- If you can still pay → Consolidate

- If you’re already failing → Settlement

14. How Banks Trap You in Long-Term Debt (Reality Check)

Let’s be very clear—this is designed.

1. Minimum Payment Design

Banks calculate minimums to:

- Stretch repayment to 5–10 years

- Maximize interest

2. High APR + Compounding

Interest compounds monthly:

- You pay interest on interest

3. Reward Psychology

Cashback, points:

👉 Encourages more spending

4. Credit Limit Increases

You feel:

“I can spend more”

But actually:

👉 You’re increasing future liability

15. Debt Payoff Formula (Simple but Powerful)

Here’s the rule most people ignore:

Income – Expenses = Debt Freedom Speed

Not:

Income – Debt = leftover

Meaning:

If you don’t control expenses:

👉 No strategy will work

16. The 3-Bucket System (Practical Control Method)

Split your money into:

Bucket 1: Essentials (50%)

- Rent

- Food

- Bills

Bucket 2: Debt (30–40%)

- Aggressive repayment

Bucket 3: Savings (10–20%)

- Emergency buffer

This ensures:

👉 You don’t fall back into debt again

17. Credit Score Recovery Strategy (After Debt)

Paying off debt is not the end.

You must rebuild your credit.

Step 1: Keep Utilization Below 30%

Ideal: 10–20%

Step 2: On-Time Payments Only

100% payment history = key factor

Step 3: Keep Old Accounts Active

Don’t close long history accounts

Step 4: Limit Hard Inquiries

Avoid multiple applications

18. Emotional Triggers That Cause Debt (Psychology Layer)

Most people don’t go into debt because of need.

They go because of:

- Stress spending

- Lifestyle comparison

- Social pressure

- “I deserve this” mindset

Solution:

Create friction:

- Remove saved cards

- Use debit for daily spend

- Track expenses

19. What to Do If You’re Already Behind on Payments

If you’ve missed payments:

Step 1: Call Your Bank Immediately

Ask for:

- Hardship programs

- Temporary reduced interest

Step 2: Negotiate Payment Plan

Banks prefer:

👉 Partial recovery over default

Step 3: Avoid Ignoring Calls

Ignoring = escalation to collections

20. Collections Strategy (Critical Section)

If your debt goes to collections:

What Happens:

- Account charged off

- Collection agency takes over

- Credit score drops heavily

What You Should Do:

- Verify the debt (don’t blindly pay)

- Negotiate settlement (30–60%)

- Ask for “Pay for Delete” (if possible)

Important:

Never agree verbally—get everything in writing.

21. The “Debt Snowball Burnout” Problem

Most people quit mid-way.

Why?

- No immediate results

- Long timelines

- Emotional fatigue

Fix:

- Track monthly progress

- Celebrate small wins

- Visualize debt reduction

22. Automation Strategy (Underrated Hack)

Set:

- Auto minimum payment (safety)

- Manual extra payment (growth)

This prevents:

- Late fees

- Score damage

23. Side Income Strategy (Fastest Debt Killer)

This is the game changer.

Examples:

- Freelancing (writing, design)

- Delivery gigs

- Selling digital services

Rule:

👉 100% side income → debt

This can:

- Cut payoff time by 50%

24. Expense Cutting Blueprint (Realistic)

Don’t go extreme. Go smart.

Cut:

- Subscriptions

- Dining out

- Impulse shopping

Keep:

- Essentials

- Productivity tools

Goal:

👉 Free $300–$500/month extra

25. Warning Signs You’re Heading Toward Debt Trap

If you notice:

- Using one card to pay another

- Skipping payments

- Constant balance increase

- Stress around bills

👉 You’re entering danger zone

26. Real Strategy Breakdown (Simple Formula)

Here’s the actual system:

- Stop new debt

- Choose strategy

- Increase payment

- Reduce expenses

- Add income

- Stay consistent

Most people fail at:

👉 Step 6 (Consistency)

27. What Will Change in 2026–2027 (Future Insight)

- Higher APR trends

- Stricter lending

- More AI-based risk checks

- Faster move to collections

Meaning:

👉 Debt will become harder to manage

28. Brutal Truth (But Necessary)

If you don’t act:

- Your debt will grow faster than your income

- Interest will eat your progress

- Financial stress will increase

But if you act:

- You can be debt-free in 12–24 months

- Your credit score will recover

- Your financial control will return

29. MaintainMarket Tested Insight

Users who follow:

- Structured plan

- High payment discipline

- No new debt

👉 Clear $10K debt 2x faster

This is not luck.

It’s execution.

30. Final Power Statement

You don’t need:

- Perfect income

- Financial expertise

- Complex tools

You need:

👉 A clear plan + consistent action

Why MaintainMarket is Different

Most platforms give generic advice.

MaintainMarket focuses on:

- Real user behavior

- Practical strategies

- Result-based approach

- Debt freedom roadmap

This is built for execution—not theory.

FAQ – $10K+ Credit Card Debt

1. Is $10,000 credit card debt bad in 2026?

Yes, especially with high APR—it can double if unmanaged.

2. Should I use debt consolidation?

If it lowers your interest rate—yes.

3. Does paying more improve credit score?

Yes, by reducing utilization.

4. Is settlement a good option?

Only in extreme cases—it impacts credit score.

5. Can I negotiate with banks?

Yes, especially if you’re struggling.

6. How long does it take to become debt-free?

12–36 months depending on strategy.

People also searched for: 7 Reasons Why Your Credit Card Limit Reduced? Here’s What Banks Are Not Telling You

Also Read: Fake Loan Scams in USA 2026: 7 Warning Signs That Can Save You Thousands

Loan Rejected? Get Emergency Cash with Bad Credit in USA (2026 Proven Hacks)