Struggling with credit card debt in 2026? Learn proven strategies to escape debt fast, avoid collections, and regain control of your finances. In this article, let’s talk about – How to Get Out of Debt Fast.

Introduction

Let’s be honest.

Debt doesn’t hit you all at once.

It starts small.

$500 → $1,200 → $5,000 → suddenly you’re staring at $18,000 and thinking:

“How did this even happen?”

Meanwhile:

- Interest keeps growing (20%–30% APR in the US)

- Minimum payments barely reduce anything

- Collection calls start creeping in

And the worst part?

You feel stuck.

Not broke — stuck.

This guide is not going to sugarcoat anything.

You’re going to understand:

- Why you’re trapped

- What actually works

- And how to get out fast (not “someday”)

Quick Answer (Featured Snippet)

To get out of debt fast in the USA in 2026:

- Stop relying on minimum payments

- Choose a payoff strategy (Snowball or Avalanche)

- Cut interest (balance transfer or consolidation)

- Increase income temporarily

- Focus aggressively on highest-impact debt

Most people can become debt-free in 12–36 months with the right system.

Why People Fall Into Debt (US System Reality)

This isn’t just your fault. The system is built this way.

1. Minimum Payment Trap

Banks don’t want you debt-free.

They want you paying interest for years.

Example:

- $10,000 debt

- 24% APR

- Minimum payment: ~$200

You’ll pay for 7–10 years if you follow minimum only.

2. High APR Culture

In the US:

- Average credit card APR: 20%–29%

That means:

You’re fighting interest more than principal.

3. Easy Credit Access

You get:

- Pre-approved cards

- Credit limit increases

Before you realize:

You’re overleveraged.

4. Lifestyle Inflation

Income goes up → spending goes up faster.

Result:

No savings, only debt.

5. Emergency Expenses

Medical bills

Job loss

Car repair

One emergency = credit card usage → long-term debt

The Real Escape Strategy (Not Motivational, Practical)

There are only 3 levers that matter:

- Reduce interest

- Increase payment amount

- Stay consistent

Everything else is noise.

Best Debt Payoff Strategies (What Actually Works)

1. Snowball Method (Psychological Win)

- Pay smallest debt first

- Gain quick momentum

- Build motivation

Best for:

People who need emotional wins

2. Avalanche Method (Mathematical Win)

- Pay highest interest debt first

- Save maximum money

Best for:

People disciplined with numbers

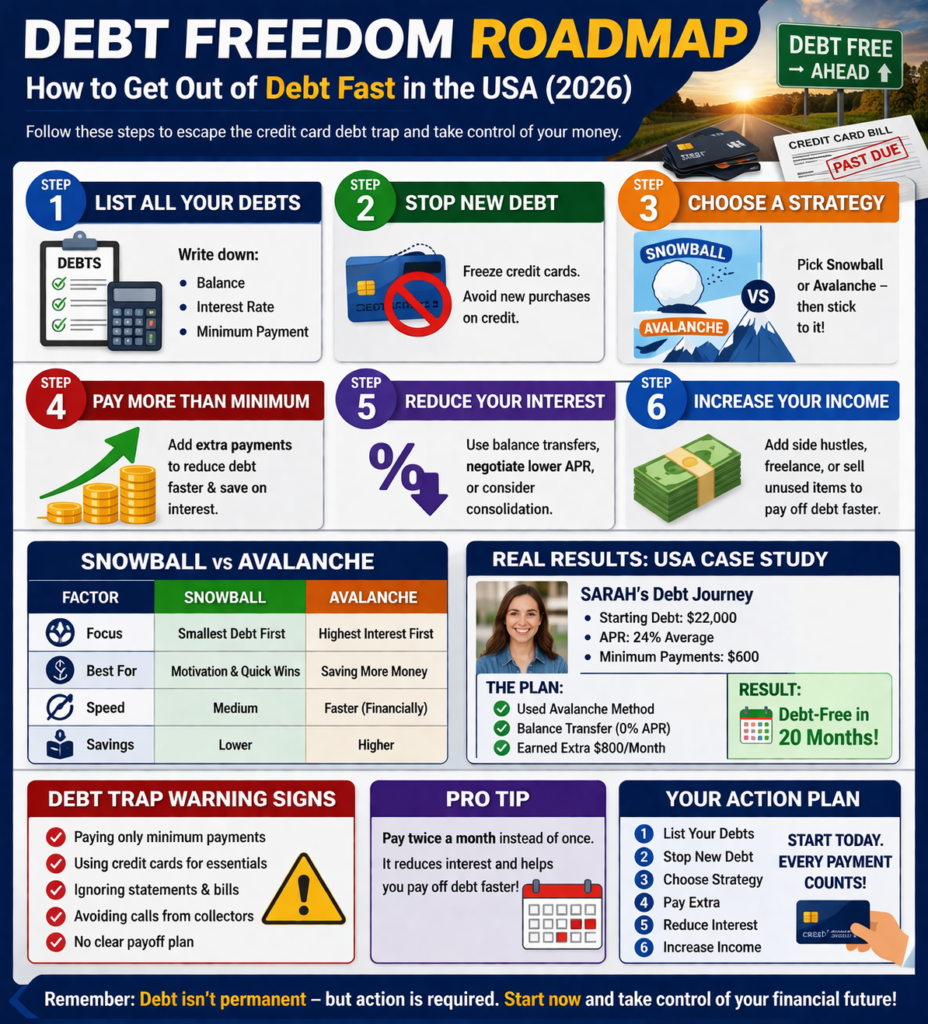

Snowball vs Avalanche (Comparison Table)

| Factor | Snowball | Avalanche |

|---|---|---|

| Focus | Smallest debt | Highest interest |

| Motivation | High | Medium |

| Savings | Lower | Higher |

| Speed | Medium | Faster (financially) |

| Best For | Beginners | Serious planners |

Step-by-Step Debt Escape Plan (Real System)

Step 1: List All Your Debts

Write:

- Total amount

- Interest rate

- Minimum payment

Clarity = control

Step 2: Stop New Debt Immediately

No new:

- Credit card usage

- EMI traps

This is non-negotiable.

Step 3: Choose Strategy (Snowball or Avalanche)

Don’t mix both.

Pick one → stick to it.

Step 4: Attack With Extra Payments

Even +$200/month can:

- Cut years off your debt

Step 5: Reduce Interest (Game Changer)

Options:

- Balance transfer (0% intro APR)

- Debt consolidation loan

This alone can save thousands

Step 6: Increase Income Temporarily

Not forever.

Just for 6–12 months:

- Freelance

- Part-time

- Selling unused items

Debt freedom requires short-term sacrifice

Debt Settlement vs Consolidation (Important Decision)

| Factor | Settlement | Consolidation |

|---|---|---|

| Impact on Credit | Negative | Neutral/Positive |

| Amount Paid | Reduced | Full |

| Time | Faster | Medium |

| Risk | High | Low |

| Best For | Severe debt | Manageable debt |

Debt Traps Most People Don’t Realize

1. The “0% APR Illusion” Trap

Balance transfer cards look like a lifesaver.

But:

- 0% is temporary (12–18 months)

- After that → APR jumps to 20%+

If you don’t clear debt in time, you’re back in the trap.

Smart move: Use only with a strict payoff plan.

2. Minimum Payment Psychological Trap

Minimum payment is designed to:

- Feel easy

- Keep you comfortable

- Extend your debt

Reality: Minimum payment = maximum interest.

3. Credit Limit Increase Trap

When your limit increases:

- You spend more

- Debt grows silently

It feels like progress — but it’s not.

4. Buy Now, Pay Later (BNPL) Debt Cycle

BNPL feels harmless.

But:

- Multiple small payments stack up

- You lose track of total debt

5. Debt Stacking Strategy (Hybrid Model)

Combine:

- Snowball (quick wins)

- Avalanche (interest saving)

Start small → then shift to high-interest debts.

6. Payment Timing Hack (Little Known Trick)

Instead of paying once:

Pay twice a month

This:

- Reduces interest

- Speeds up payoff

7. Negotiate Your Interest Rate

Call your bank.

Ask for lower APR.

You can reduce:

- 3%–10% interest

This saves serious money.

8. Hardship Programs (Hidden Option)

Banks offer:

- Lower payments

- Temporary relief

But only if you ask.

9. Debt Consolidation Timing Strategy

Best time to consolidate:

- Credit score above 650

Late action = worse terms.

10. What Happens When Debt Goes to Collections

Timeline:

- 30 days → late fee

- 60–90 days → credit damage

- 120+ days → collections

11. How to Deal With Collection Agencies

Do this:

- Ask for validation

- Don’t agree instantly

- Negotiate properly

12. Smart Settlement Strategy

- Save money first

- Negotiate (30–60%)

- Get written agreement

Never trust verbal deals.

13. Why Cutting Expenses Alone Won’t Work

You can’t cut forever.

Income growth = faster escape.

14. Fast Income Ideas (USA Context)

- Uber / DoorDash

- Freelancing

- Selling unused items

Extra $500/month = big impact

15. Why People Quit Debt Plans

- No quick results

- Burnout

- Unexpected expenses

16. The “Debt Fatigue” Phase

Around month 2–4:

- Motivation drops

- Progress feels slow

Most people quit here.

17. How to Stay Consistent

- Track progress

- Celebrate wins

- Automate payments

18. Debt Settlement vs Bankruptcy

| Factor | Settlement | Bankruptcy |

|---|---|---|

| Credit Impact | Medium | Severe |

| Time | Faster | Long-term |

| Debt Relief | Partial | Full/Partial |

| Legal | No | Yes |

19. Opportunity Cost of Debt

While paying interest:

- You lose investment growth

- You delay wealth building

20. Mental Cost of Debt

Debt affects:

- Stress levels

- Decision making

- Relationships

21. Signs You’re in a Debt Trap

- Paying minimums only

- Using credit for basics

- Ignoring statements

- No plan

3+ signs = you’re trapped.

22. Tools That Help You Escape Faster

- Balance transfer cards

- Consolidation loans

- Budget apps

These accelerate your plan.

23. The Truth Most People Avoid

Debt isn’t permanent.

But staying in debt is a choice.

Every delay = more interest paid.

Real Case Study (USA)

Case: Sarah (California)

- Debt: $22,000

- APR: 24% average

- Minimum payments: $600

Problem:

Debt wasn’t reducing.

Solution:

- Chose Avalanche method

- Took balance transfer (0% APR for 12 months)

- Increased income by $800/month

Result:

Debt-free in 20 months

Mistakes That Keep You Stuck

- Paying only minimum

- Ignoring interest rates

- Using cards again during payoff

- Not tracking progress

- Waiting for “right time”

Expert Insights (What Actually Works)

1. Debt Is a Behavior Problem, Not Just Math

If habits don’t change:

Debt comes back.

2. Speed > Perfection

You don’t need perfect strategy.

You need consistent action.

3. Income Boost Is the Shortcut

Cutting expenses helps.

But increasing income changes the game faster

Timeline: How Fast Can You Be Debt-Free?

| Debt Amount | Aggressive Plan | Normal Plan |

|---|---|---|

| $5,000 | 3–6 months | 8–12 months |

| $10,000 | 6–12 months | 12–24 months |

| $20,000+ | 12–24 months | 24–36 months |

Strategy Logic (Why This Works)

You’re attacking:

- Interest (reducing it)

- Time (paying faster)

- Behavior (stopping cycle)

This combination breaks the trap.

MaintainMarket Expert Advice

If you’re serious:

Don’t think:

“I’ll try”

Think:

“I’m finishing this”

Debt doesn’t disappear slowly.

It disappears when you become aggressive.

Why MaintainMarket Is Different

Most blogs:

Give theory

We:

- Break down real financial psychology

- Give step-by-step action

- Focus on outcomes

This is built for people who actually want results.

Final Action Plan (Do This Now)

- List all debts

- Stop using credit cards

- Choose payoff strategy

- Add extra monthly payment

- Reduce interest immediately

- Increase income

- Track progress weekly

FAQs – How to Get Out of Debt Fast

Q1. What is the fastest way to get out of debt?

Aggressive payments + interest reduction.

Q2. Should I close credit cards?

No, but stop using them.

Q3. Is debt consolidation worth it?

Yes, if it reduces interest.

Q4. Can I negotiate credit card debt?

Yes, but it impacts credit score.

Q5. How much should I pay monthly?

As much as possible beyond minimum.

Q6. Snowball or avalanche better?

Depends on personality vs math.

Q7. How to stop collection calls?

Communicate or settle legally.

Q8. Can I be debt-free in 1 year?

Yes, with aggressive strategy.

People also searched for: Why Your Tax Refund Is Delayed in 2026 (IRS) — And How to Get It Faster

Also read: Best Financial Tools in the USA That Actually Save You Money and Help You Earn More (2026 Guide)

Loan Denied After Pre-Approval? Real Reasons & Fix – Solutions To Know (USA 2026)