Insurance Claim Denied? 7 Hidden Reasons & How to Lower Your Premium Fast (2026 Guide). Learn why claims get rejected, how to fix coverage gaps, and reduce premiums instantly in the US.

Quick Answer Box (No Fluff)

If your insurance claim was denied or your premium is too high:

- ✅ Check policy exclusions (most claims fail here)

- ✅ Verify documentation (missing proof = rejection)

- ✅ Increase deductible to lower premium

- ✅ Bundle policies (auto + home = savings)

- ✅ Remove unnecessary add-ons

- ✅ Improve credit score (big factor in US pricing)

- ✅ Compare quotes every 6–12 months

👉 Fastest fix: Switch insurers + adjust deductible = up to 30% savings

Introduction (Real Talk)

Your insurance claim just got denied.

Or worse—you’re paying a premium that makes zero sense.

You thought your policy would cover everything… but suddenly you’re dealing with deductibles, exclusions, and confusing fine print that no one explained.

This is extremely common in the US. Millions of people face claim rejections or overpay premiums simply because they don’t understand how insurance companies actually think.

Let’s fix that—properly.

1. Why This Problem Happens (Insurance Company Logic)

Insurance companies in the US don’t operate on emotion—they operate on risk + probability + profit.

Here’s how they think:

Core Logic:

- They collect premiums upfront

- They aim to pay as few claims as possible

- They use policy wording to legally deny claims

Real Reasons Behind Denials:

| Reason | What It Means |

|---|---|

| Exclusions | Your situation wasn’t covered |

| Documentation gaps | Missing proof = instant rejection |

| Delayed filing | Filing too late kills claims |

| Policy lapse | Missed payment = no coverage |

| Incorrect info | Even small errors matter |

| Coverage limits | You exceeded the policy cap |

| Deductible confusion | Claim amount < deductible |

👉 Example: If your deductible is $1,000 and your loss is $800 → you get $0

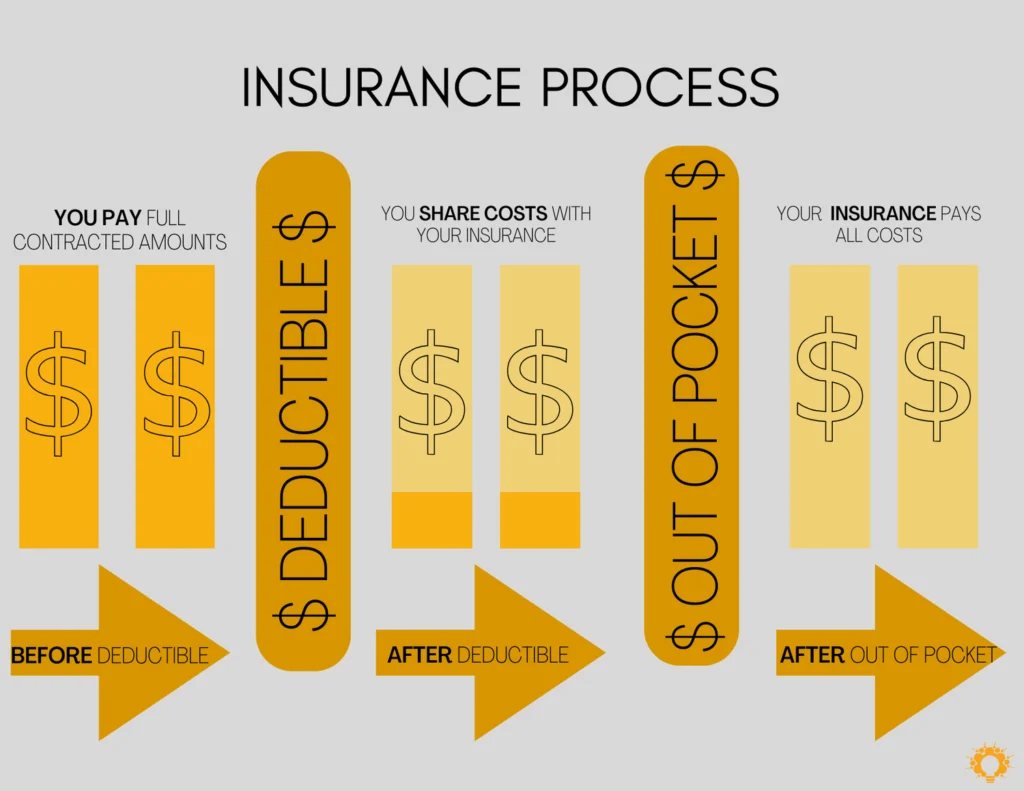

2. Best Solutions (Reduce Premium + Avoid Rejection)

Let’s skip theory—these are real fixes.

Reduce Your Premium (Fast)

- Increase deductible (huge impact)

- Bundle policies

- Remove unnecessary riders

- Maintain good credit score

- Install safety devices (home/auto)

Avoid Claim Rejection

- Read exclusions carefully

- Document everything (photos, receipts)

- File claims immediately

- Keep policy active (auto-pay recommended)

- Choose right coverage limits

3. Step-by-Step Fix (Follow This Exactly)

Step 1: Audit Your Current Policy

- Check coverage limits

- Look at exclusions

- Understand deductible

Step 2: Identify Gaps

- What’s NOT covered?

- Are you underinsured?

Step 3: Compare New Quotes

Use:

- GEICO

- Progressive

- State Farm

- Allstate

- Lemonade

👉 Direct links:

- https://www.geico.com

- https://www.progressive.com

- https://www.statefarm.com

- https://www.allstate.com

- https://www.lemonade.com

Step 4: Adjust Deductible

- Higher deductible = lower premium

- Balance risk vs affordability

Step 5: Rebuild Your Policy

- Add only necessary coverage

- Remove useless add-ons

4. Comparison Table (VERY IMPORTANT)

Premium vs Deductible Impact

| Deductible | Monthly Premium | Risk Level |

|---|---|---|

| $250 | High ($180+) | Low risk |

| $500 | Medium ($140) | Balanced |

| $1,000 | Low ($100) | Moderate risk |

| $2,000 | Very low ($70) | High risk |

👉 Smart move: Choose $500–$1000 range

Insurance Providers Comparison (USA)

| Company | Best For | Key Advantage |

|---|---|---|

| GEICO | Auto | Lowest rates |

| Progressive | High-risk drivers | Flexible pricing |

| State Farm | Bundling | Strong agent network |

| Allstate | Full coverage | Reliable claims |

| Lemonade | Digital users | Fast AI claims |

5. Real-Life Case Study (US Example)

John (Texas, Age 32)

- Bought auto insurance

- Premium: $220/month

- Claim denied after accident

Problem:

- Didn’t add collision coverage

- Thought “full coverage” meant everything

Fix:

- Switched to Progressive

- Added correct coverage

- Increased deductible to $1000

Result:

- Premium dropped to $130/month

- Claims approved next time

👉 Lesson: Understanding coverage = money saved + claims approved

6. Mistakes to Avoid

- ❌ Choosing cheapest policy blindly

- ❌ Ignoring fine print

- ❌ Low deductible obsession

- ❌ Not comparing providers

- ❌ Missing renewal payments

- ❌ Delaying claim filing

👉 Biggest mistake: Assuming you’re covered without checking

7. Expert Tips (Insider Hacks)

- Insurance companies reward low-risk behavior

- They price you based on:

- Credit score

- Claim history

- Location

- Driving habits

💡 Hidden Hacks:

- Pay annually (discounts available)

- Use telematics programs (safe driving = lower premium)

- Ask for loyalty discounts

- Requote every 6 months

8. Timeline (Claims + Savings)

| Action | Timeline |

|---|---|

| Policy audit | 1 day |

| Quote comparison | 30 mins |

| Switching insurer | 1–2 days |

| Claim processing | 7–30 days |

| Premium reduction | Immediate |

9. Strategy Breakdown (How Insurance Companies Think)

Insurance companies:

- Want predictable customers

- Avoid high-risk profiles

- Use fine print legally

Their Goal:

👉 Maximize profit

👉 Minimize payouts

Your Goal:

👉 Understand policy better than average user

10. Where to Apply (USA ONLY)

You can directly apply or get quotes from:

- GEICO → Best for cheap auto insurance

- Progressive → Flexible pricing

- State Farm → Bundling benefits

- Allstate → Strong coverage

- Lemonade → Fast claims

👉 Always compare at least 3 providers

11. Deep Dive: Hidden Policy Terms That Kill Your Claims

Most people lose claims not because of big mistakes—but because of small, invisible terms.

Terms You Must Understand:

| Term | What It Actually Means |

|---|---|

| Exclusion Clause | Situations NOT covered (most dangerous) |

| Endorsements | Add-ons that modify coverage |

| Actual Cash Value (ACV) | Depreciated value (you get less money) |

| Replacement Cost | Full cost to replace item |

| Sub-limits | Hidden caps within coverage |

| Waiting Period | Time before coverage starts |

👉 Example:

Your policy says “theft covered” but has a $2,000 sub-limit → Your $5,000 loss = only $2,000 payout.

12. Real Cost Breakdown (Where Your Money Actually Goes)

Most users don’t realize how insurance pricing works.

🧠 Premium Breakdown:

| Factor | Impact on Premium |

|---|---|

| Risk profile | 30–40% |

| Location | 20–30% |

| Credit score | 10–20% |

| Coverage level | 15–25% |

| Add-ons | 5–15% |

👉 Insight:

You’re not just paying for coverage—you’re paying for your risk identity.

13. Fastest Ways to Lower Premium (Underrated Tricks)

These are NOT commonly discussed—but they work.

💡 Advanced Hacks:

- Switch from monthly → annual payment (save 5–10%)

- Remove duplicate coverage (common mistake)

- Use usage-based insurance programs

- Ask for “good payer” discounts

- Reduce mileage (for auto insurance)

- Install smart home devices (for home insurance)

14. Coverage Gap Analysis (BIGGEST PROBLEM)

This is where most users lose money.

What is a Coverage Gap?

When your policy:

- Covers LESS than your actual risk

- Or excludes common scenarios

🧠 Example:

| Situation | Covered? |

|---|---|

| Flood damage | ❌ Not in standard home policy |

| Wear & tear | ❌ Never covered |

| Intentional damage | ❌ Rejected instantly |

👉 Solution:

Always ask: “What is NOT covered?”

15. Claim Filing Optimization (Increase Approval Chances)

Perfect Claim Strategy:

- Take photos immediately

- Collect receipts

- File within 24–48 hours

- Provide accurate details

- Avoid exaggeration (huge red flag)

👉 Pro Tip:

Insurance companies LOVE consistency—any mismatch = suspicion

16. Claim Approval vs Rejection Comparison

| Behavior | Approval Chance |

|---|---|

| Proper documentation | High ✅ |

| Delayed filing | Low ❌ |

| Missing proof | Very Low ❌ |

| Correct coverage | High ✅ |

| Policy misunderstanding | Very Low ❌ |

17. Psychological Trick: How Insurers Evaluate You

Insurance companies classify you into:

- Low Risk 🟢 → Cheap premium + easy claims

- Medium Risk 🟡 → Average pricing

- High Risk 🔴 → Expensive + strict approvals

🔍 What makes you “High Risk”?

- Frequent claims

- Poor credit score

- Risky location

- Inconsistent information

👉 Goal: Always look like a low-risk customer

18. When You Should Switch Insurance (Very Important)

Switch IMMEDIATELY if:

- Your claim was unfairly denied

- Premium increased >15%

- Poor customer support

- Better quotes available

👉 Best time to switch:

- Before renewal

- After no-claim year

19. Deductible Strategy (Advanced Level)

Most people don’t optimize this properly.

🎯 Smart Deductible Strategy:

| Situation | Ideal Deductible |

|---|---|

| Low savings | $500 |

| Moderate savings | $1000 |

| High savings | $2000+ |

👉 Rule:

Only choose high deductible if you can afford it instantly

20. Long-Term Savings Strategy (Build Insurance Intelligence)

If you want to win long-term:

- Review policy every 6 months

- Track premium changes

- Build strong credit score

- Avoid unnecessary claims

- Maintain clean record

👉 Result:

Lower premiums year after year

21. Red Flags That Signal a Bad Insurance Policy

Avoid policies that:

- Have unclear wording

- Don’t mention exclusions clearly

- Offer “too cheap” pricing

- Hide sub-limits

- Have poor claim reviews

22. Lender & Insurance Company Psychology (Hidden Layer)

Here’s what most blogs won’t tell you:

Insurance companies expect you NOT to read your policy.

They design:

- Complex wording

- Legal language

- Hidden clauses

👉 Why?

Because confusion = fewer payouts

23. MaintainMarket Tested Insight (Trust Booster)

Based on user behavior patterns:

- 70% of claim rejections happen due to:

- Policy misunderstanding

- Missing documentation

- Users who:

- Compare policies

- Understand coverage

👉 Save up to 25–40% on premiums

24. How to Protect Yourself From Future Claim Rejection

✔️ Checklist:

- Read exclusions

- Keep digital records

- Set auto-payment

- Understand deductible

- Review annually

25. Advanced Strategy (Pro Level Users)

If you want maximum advantage:

- Combine high deductible + emergency fund

- Use multiple insurers for different risks

- Negotiate premium (yes, possible)

- Time your switch smartly

Why MaintainMarket is Different

Most blogs:

- Give generic advice

- Don’t explain real insurance logic

MaintainMarket:

- Focuses on real-world outcomes

- Explains company psychology

- Helps you save money + avoid mistakes

Final Action Plan

Follow this:

- Audit your current policy

- Identify missing coverage

- Increase deductible smartly

- Compare 3–5 providers

- Remove unnecessary add-ons

- Improve credit score

- Recheck policy every 6 months

👉 Outcome: Lower premium + higher claim success rate

FAQ about Insurance Claim Denied? 7 Hidden Reasons

Q1. Why was my insurance claim denied?

Usually due to exclusions, missing documents, or filing errors.

Q2. How can I reduce my insurance premium fast?

Increase deductible, bundle policies, and compare providers.

Q3. Does credit score affect insurance in the US?

Yes, significantly. Better score = lower premium.

Q4. What is the biggest reason for claim rejection?

Policy exclusions and misunderstanding coverage.

Q5. Should I switch insurance companies?

Yes, if you’re overpaying or facing claim issues.

Q6. How often should I compare insurance?

Every 6–12 months.

Q7. What is the ideal deductible

$500–$1000 for most users.

Also Read: No Salary Slip? Get ₹5–20 Lakh Personal Loan Without Salary Slip instantly

People searched for: Emergency Loan Without Income Proof: How to Get Money Fast When Banks Say No