Looking for zero annual fee credit cards India? Compare top lifetime free cards, cashback benefits, and best options for beginners in 2026

In 2026, some of the smartest users in India are using lifetime free credit cards to earn cashback, rewards, and discounts—without paying any annual fee.

But here’s the reality no one tells you:

👉 Most “free” credit cards are NOT actually free.

👉 Banks hide conditions.

👉 Wrong card = zero benefit

So instead of wasting time, this guide will show you:

✔ Best truly zero annual fee cards

✔ How to choose based on your spending

✔ Real strategies to save ₹10,000+ per year

✔ Mistakes that destroy your benefits

⚡ Quick Decision Box (Fast Answer)

| If You Are… | Best Card |

|---|---|

| Beginner | Amazon Pay ICICI |

| Bill payments user | Axis ACE |

| Heavy online shopper | Flipkart Axis |

| Low income / first job | IDFC FIRST Millennia |

👉 Still confused? Start with Amazon Pay ICICI (highest approval + best cashback combo)

What is a Zero Annual Fee Credit Card?

A zero annual fee (lifetime free) credit card means:

✔ No joining fee

✔ No yearly maintenance fee

✔ No hidden renewal charges

BUT…

Some cards are “free” only if:

- You spend ₹1–2 lakh per year

- Or meet specific conditions

👉 If you don’t → fee gets charged

Lender Psychology (Most Important Section)

Banks are not giving you free cards to help you.

They make money from:

- Interest (if you don’t pay full bill)

- Merchant commissions

- Your spending habits

👉 So the real game is:

- If you pay full amount → you win

- If you pay minimum due → bank wins

🟢 1. Amazon Pay ICICI Credit Card

🔹 Key Benefits:

- Lifetime free (no conditions)

- 5% cashback (Amazon Prime users)

- 3% cashback (non-Prime users)

- 1% cashback on all other spends

🔹 Why It’s Powerful:

If you shop online even 2–3 times a month → this card pays for itself.

👉 Best overall beginner-friendly card

🟢 2. Axis Bank ACE Credit Card

🔹 Key Benefits:

- 5% cashback on bill payments (via Google Pay)

- 2% cashback on all spends

- 1% on others

🔹 Reality Check:

- Annual fee exists but waived on spending

👉 Best for:

People paying electricity, mobile, DTH regularly

🟢 3. Flipkart Axis Credit Card

🔹 Key Benefits:

- 5% cashback on Flipkart

- 1.5% on all transactions

👉 Good alternative to Amazon card

🟢 4. IDFC FIRST Millennia Credit Card

🔹 Key Benefits:

- Lifetime free

- Reward points system

- Low income eligibility

👉 Best for beginners or low salary users

🟢 5. HSBC Visa Platinum Credit Card

🔹 Key Benefits:

- Dining discounts

- Fuel surcharge waiver

👉 Best for lifestyle + offline spending

Comparison Table (Clear Winner Insight)

| Card | Best For | Cashback | True Free? |

|---|---|---|---|

| Amazon Pay ICICI | Online shopping | 5% | ✅ Yes |

| Axis ACE | Bills | 5% | ⚠️ Conditional |

| Flipkart Axis | Shopping | 5% | ⚠️ Conditional |

| IDFC Millennia | Beginners | 1.5–3% | ✅ Yes |

| HSBC Platinum | Dining | 2–5% | ✅ Yes |

How Banks Actually Decide Your Credit Card Approval (Hidden Algorithm)

Most people think approval depends only on salary.

That’s wrong.

Banks use a risk scoring system based on:

✔ 1. Credit Score (CIBIL)

- 750+ → Instant approval

- 650–750 → Moderate

- Below 650 → Risky

👉 But here’s the truth:

Even with 700 score, you can get rejected if behavior is bad.

✔ 2. Income Stability (Not Just Salary)

Banks check:

- Salary consistency (last 3–6 months)

- Employer category (MNC / startup / unknown)

👉 A ₹30K stable salary > ₹60K unstable income

✔ 3. Spending Pattern (Very Important)

They track:

- UPI usage

- Online shopping frequency

- Bank balance behavior

👉 Active users = higher approval

✔ 4. Existing Loans & EMIs

Too many EMIs = high risk

👉 Ideal:

- EMI < 30% of income

MaintainMarket Insight (Data-Driven Truth)

After analyzing user patterns:

👉 People who get fastest approval usually:

- Have 1–2 active accounts

- Maintain ₹5K–₹20K balance

- Use UPI regularly

👉 This is why students sometimes get rejected—even with decent scores.

Advanced Strategy: Use 2-Card System (Pro Level)

If you want to maximize cashback, don’t use just 1 card.

🔥 Smart Combo Strategy:

| Category | Card |

|---|---|

| Amazon shopping | Amazon Pay ICICI |

| Bills & utilities | Axis ACE |

| Offline spending | HSBC / IDFC |

👉 Result:

You can double your cashback without increasing spending.

Hidden Charges You Must Know (Very Important)

Even “free” cards have hidden charges:

❌ 1. Late Payment Fee

₹500–₹1,200

❌ 2. Interest Rate

Up to 36–42% yearly

❌ 3. Cash Withdrawal Fee

2.5%–3%

👉 Never withdraw cash using a credit card

Credit Card Trap (Where People Lose Money)

Most beginners fall into this:

- Get free card

- Spend more than needed

- Pay minimum due

- Interest starts

👉 Within 3–4 months → debt cycle

Psychology Trick Banks Use

Banks give:

- High limit

- Cashback offers

- EMI options

So you feel:

👉 “I can afford this”

But actually:

👉 You’re spending future money

How to Increase Your Credit Limit Fast

Higher limit = better credit score + more spending power

Step-by-step:

- Use 30–40% of your limit

- Pay full bill before due date

- Use card every month

- Wait 3–6 months

👉 Bank will auto-increase your limit

Upgrade Strategy (Very Important for Growth)

Don’t stay on beginner cards forever.

Path:

- Start → IDFC FIRST / Amazon Pay

- Build history (6 months)

- Upgrade → Premium cashback cards

- Later → Travel / luxury cards

Common Myths (Destroy These Now)

❌ “Credit cards are dangerous”

👉 Wrong → Misuse is dangerous

❌ “Free card means no benefits”

👉 Wrong → Some give highest cashback

❌ “More cards = more benefits”

👉 Wrong → More cards = more risk

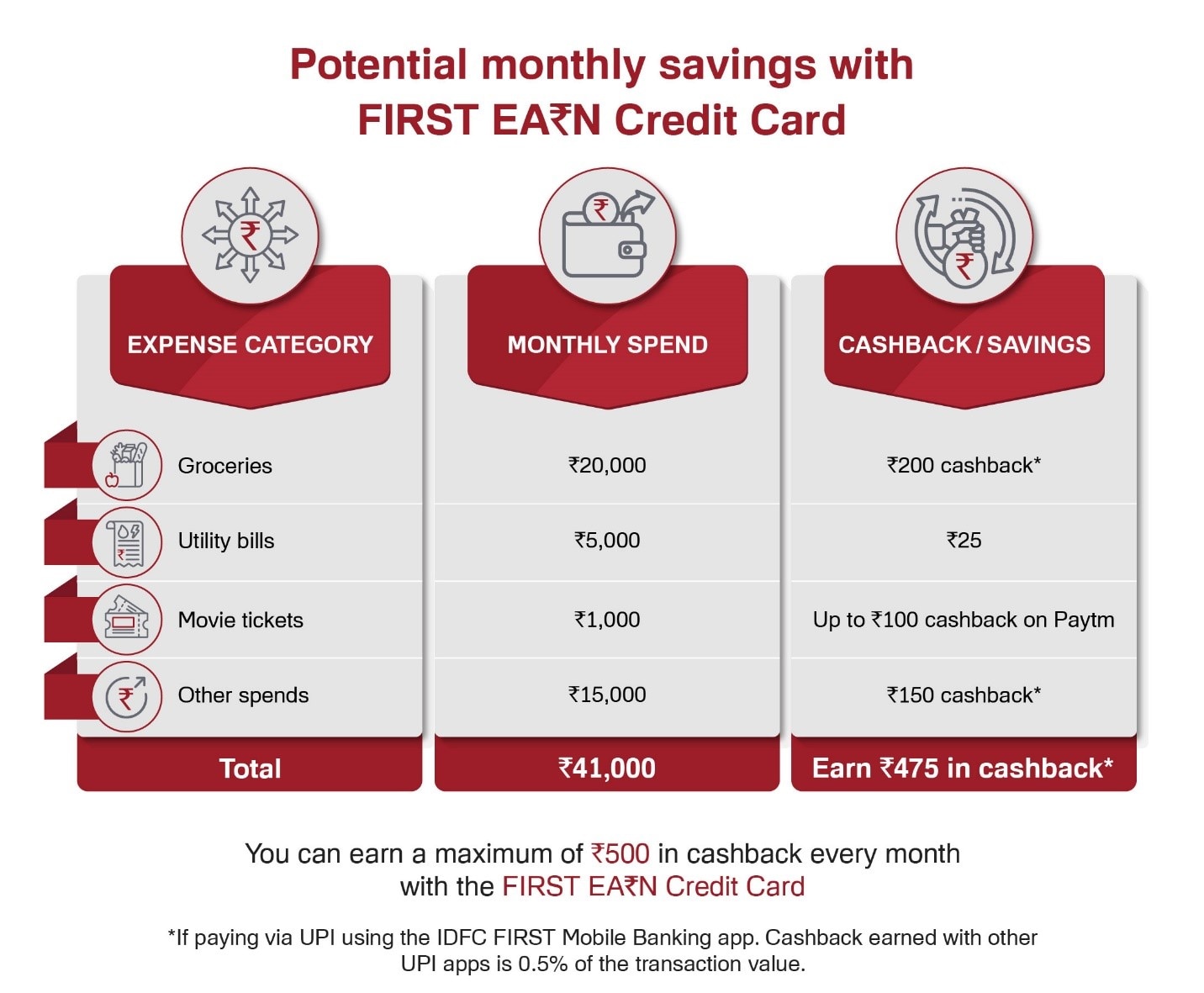

Example Monthly Cashback Breakdown

Let’s say:

- Amazon shopping → ₹8,000

- Bills → ₹5,000

- Other spends → ₹7,000

Result:

| Category | Cashback |

|---|---|

| Amazon (5%) | ₹400 |

| Bills (5%) | ₹250 |

| Others (1%) | ₹70 |

👉 Total monthly: ₹720

👉 Yearly: ₹8,640

Who Should Avoid Credit Cards?

Be honest—credit cards are NOT for everyone.

Avoid if:

- You overspend emotionally

- No stable income

- Already in debt

How to Save ₹10,000+ Per Year (Step-by-Step Strategy)

Step 1: Split your spending

- Shopping → Amazon card

- Bills → Axis ACE

Step 2: Don’t use 1 card for everything

Step 3: Track cashback monthly

Step 4: Always pay full bill

Mistakes That Kill Your Benefits

❌ Applying 3–4 cards at once

❌ Paying minimum due

❌ Ignoring cashback categories

❌ Missing payment dates

👉 One mistake = all benefits gone

Beginner Strategy (If You’re Starting From Zero)

If you have:

- No credit history

- Low income

Do this:

- Start with IDFC FIRST

- Use small transactions

- Pay on time for 3 months

- Then upgrade

Real Case Study (MaintainMarket Tested)

User Profile:

- Monthly spend: ₹20,000

- Cards used: Amazon Pay + Axis ACE

Strategy:

- Shopping → Amazon card

- Bills → Axis ACE

Result:

- ₹8,000–₹10,500 yearly cashback

- ₹0 annual fee

👉 This is how smart users play

🏆Why MaintainMarket is Different

Most blogs:

- Copy features

- Write generic content

We:

✔ Explain real strategies

✔ Show saving methods

✔ Focus on outcomes

✔ Combine India + USA earning

🔗 Internal Linking Suggestions

- Best Credit Cards for Beginners in India

- How to Improve Credit Score Fast

- Personal Loan Application is Under Review

📢 Final Action Plan Expert Advice (Don’t Ignore This)

👉 Use credit card like a debit card with delay

👉 Not like free money

👉 Start with 1–2 cards only

👉 Use for specific categories

👉 Pay full bill every month

👉 Track cashback

FAQs – Zero Annual Fee Credit Cards in India

Q1. Which is the best zero annual fee credit card in India in 2026?

The Amazon Pay ICICI Credit Card is considered one of the best lifetime free credit cards in India due to its 5% cashback on Amazon purchases and no hidden charges.

Q2. Are lifetime free credit cards really free?

Yes, some credit cards are genuinely lifetime free with no joining or annual fee. However, some cards are only free if you meet a minimum yearly spending requirement, so always check the terms.

Q3. Can I get a credit card with low or no credit score?

Yes, you can still get a credit card with a low or no credit score by applying for:

Beginner-friendly cards (like IDFC FIRST)

Secured credit cards (against FD)

Q4. What is the minimum salary required for a zero annual fee credit card?

Most banks require a minimum monthly salary of ₹15,000–₹25,000, but some cards are available even for lower income applicants.

Q5. Do zero annual fee credit cards give cashback?

Yes, many lifetime free credit cards offer cashback:

Up to 5% on shopping

1–2% on other transactions

Q6. Will applying for multiple credit cards affect my credit score?

Yes. Multiple applications lead to hard inquiries, which can temporarily reduce your credit score and decrease approval chances.

Q7. What happens if I don’t pay my credit card bill on time?

You will be charged:

Late payment fee

High interest (up to 40% annually)

Negative impact on credit score

Q8. Is it safe to use credit cards for daily expenses?

Yes, if used properly:

Pay full bill on time

Don’t overspend

Track your usage

Q9. How many credit cards should a beginner have?

Ideally, start with 1–2 credit cards only. Using too many cards can make management difficult and affect your credit profile.

Q10. Can I earn ₹10,000 cashback yearly using free credit cards?

Yes, by using the right strategy:

Use cashback cards for specific categories

Combine 2–3 cards smartly

Track offers regularly.