Learn how to refinance student loans in 2026, lower your monthly payments, improve cash flow, and avoid refinancing mistakes that cost borrowers thousands.

“Split-screen thumbnail with stressed borrower on one side and lower monthly payment approval dashboard on the other, bold text saying ‘CUT YOUR STUDENT LOAN PAYMENT?’ with finance-style dramatic lighting”

Introduction

Student loan payments are crushing millions of Americans right now.

People are delaying:

- buying homes,

- starting families,

- investing,

- and even changing careers

because monthly payments keep eating their income.

And in 2026, things feel even worse.

Interest rates remain high.

Living costs keep rising.

And many borrowers are realizing they’ve barely reduced their principal balance after years of payments.

That’s why student loan refinancing searches are exploding across the USA.

But here’s the dangerous part:

A lot of borrowers refinance the wrong way and end up:

- losing federal protections,

- increasing repayment timelines,

- or paying more long term.

Refinancing can absolutely help.

But only if you understand how lenders actually structure these deals.

This guide explains:

- how to refinance student loans properly,

- when refinancing makes sense,

- how to lower payments safely,

- and the hidden traps most borrowers never see coming.

Quick Answer Box

How to Refinance Student Loans Quickly

Student loan refinancing means replacing your current student loans with a new loan that ideally offers:

- lower interest rates,

- smaller monthly payments,

- or a shorter repayment term.

Best results usually happen when borrowers:

- improve credit scores,

- reduce debt-to-income ratio,

- apply with stable income,

- and compare multiple refinance lenders before accepting offers.

Refinancing works best for borrowers with:

- private student loans,

- stable income,

- strong repayment history,

- and decent credit scores.

Why Student Loan Refinancing Has Become So Popular

Monthly Payments Are Draining Cash Flow

A lot of Americans are financially stuck.

Even people earning decent salaries feel trapped because:

- rent increased,

- groceries became expensive,

- insurance costs rose,

- and interest rates climbed.

Student loan debt is often the biggest monthly burden after housing.

Many Borrowers Took High Interest Loans Years Ago

A huge number of borrowers signed loans when:

- they were young,

- financially inexperienced,

- or desperate for approval.

Now they realize:

- their APR is too high,

- repayment timeline is too long,

- and interest is eating most payments.

Federal Payment Changes Created Confusion

Repayment plan changes and policy uncertainty caused many borrowers to rethink their debt strategy.

Some borrowers now prefer predictable refinancing terms instead of waiting for policy updates.

What Student Loan Refinancing Actually Means

Refinancing Is NOT the Same as Consolidation

This confuses many people.

Consolidation

Combines multiple loans into one payment.

Refinancing

Replaces old loans with a completely new loan, usually from a private lender.

Goal:

- lower APR,

- reduce monthly payment,

- or improve repayment structure.

When Refinancing Makes Sense

You Have High Interest Rates

If your current rates are extremely high, refinancing may save thousands long term.

Your Credit Score Improved

Lenders reward lower-risk borrowers.

If your score improved since graduation, you may qualify for:

- lower APR,

- better terms,

- and reduced monthly costs.

You Have Stable Income

Stable income increases approval chances significantly.

Lenders care heavily about:

- employment consistency,

- debt-to-income ratio,

- and repayment history.

You Want Predictable Payments

Fixed-rate refinancing helps borrowers avoid payment uncertainty.

When Refinancing Can Be a Bad Idea

You Have Federal Loan Benefits

Refinancing federal loans into private loans may remove:

- income-driven repayment,

- federal deferment,

- hardship protections,

- and forgiveness opportunities.

This is one of the biggest mistakes borrowers make.

Your Income Is Unstable

If income fluctuates heavily, flexible federal repayment options may be safer.

Your Credit Score Is Too Low

Poor credit can lead to:

- higher refinance rates,

- stricter approval conditions,

- or rejection.

Sometimes improving credit first saves more money later.

How Lenders Actually Evaluate Student Loan Refinance Applications

Most borrowers think lenders only check credit scores.

That’s not true anymore.

Lenders now analyze:

- debt-to-income ratio,

- spending behavior,

- income consistency,

- employment history,

- credit utilization,

- and financial stability patterns.

They ask:

“Will this borrower safely repay us over the next several years?”

That’s the real approval question.

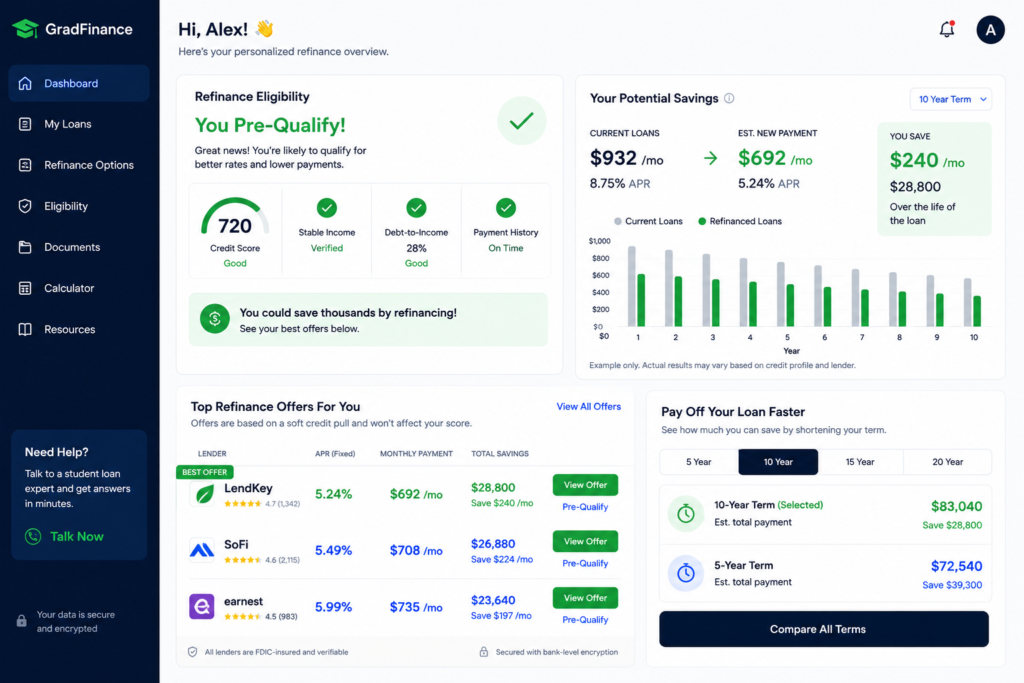

Step-by-Step Guide to Refinance Student Loans

Step 1 — Check Your Current Loan Terms

Review:

- current APR,

- repayment length,

- monthly payment,

- and total remaining balance.

Many borrowers refinance without even understanding their current loan structure.

Step 2 — Check Your Credit Score

Better scores usually unlock better refinance rates.

Typical stronger refinance profiles:

- 680+ FICO

- stable income

- low utilization

Step 3 — Calculate Debt-to-Income Ratio

Debt-to-Income Ratio=Gross Monthly IncomeMonthly Debt Payments×100

Lower debt-to-income ratios improve approval odds significantly.

Step 4 — Compare Multiple Refinance Offers

Never accept the first offer.

Compare:

- APR,

- fixed vs variable rates,

- repayment terms,

- hardship flexibility,

- and lender reputation.

Step 5 — Choose Fixed or Variable Rate Carefully

Fixed Rate

- Stable payments

- Safer long term

Variable Rate

- Lower starting APR

- Payments can increase later

Many borrowers underestimate future rate increases.

Step 6 — Apply Strategically

Too many applications can create unnecessary hard inquiries.

Use prequalification tools whenever possible.

Also read: Loan With 550 CIBIL Score India (2026): Best Approval Options After Rejection

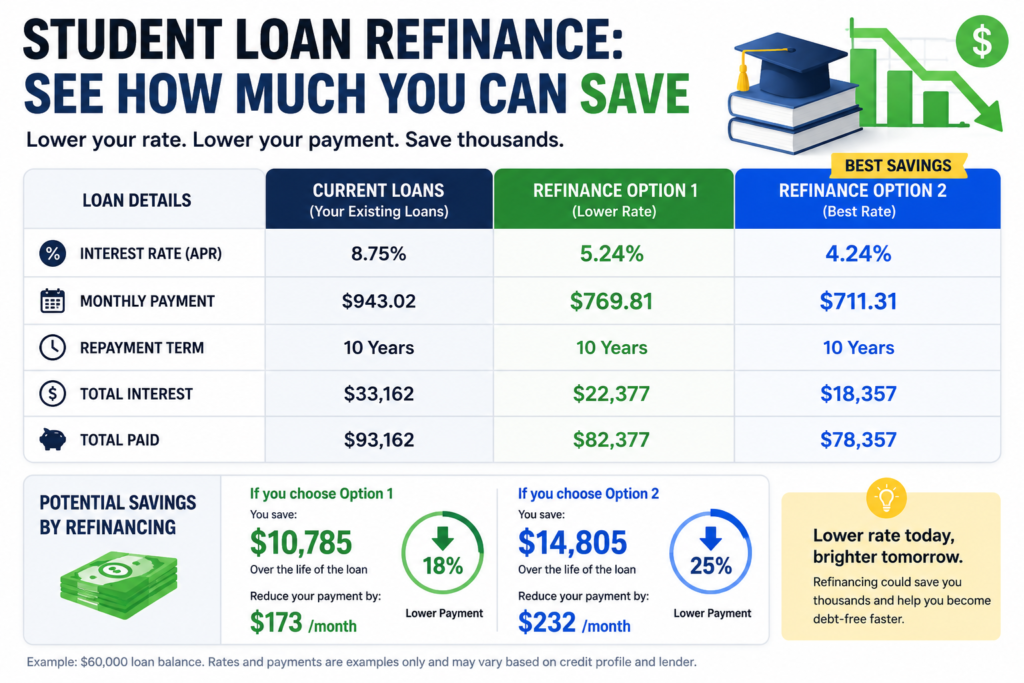

Real-Life USA Case Study

How Emily Reduced Her Student Loan Burden

Emily graduated with:

- $78,000 student debt,

- 9.4% private loan APR,

- monthly payment near $980.

She felt financially stuck despite earning decent income.

What she changed:

- improved credit score from 648 to 712,

- reduced credit utilization,

- waited six months,

- compared refinance lenders carefully.

Result:

- refinanced into 5.7% fixed rate,

- monthly payment dropped significantly,

- saved thousands in projected interest.

Most importantly:

She finally regained monthly breathing room.

Comparison Table — Refinancing Options

| Option | Best For | Main Risk | Potential Benefit |

|---|---|---|---|

| Fixed Rate Refinance | Stability | Slightly higher starting APR | Predictable payments |

| Variable Rate Refinance | Short-term savings | Rate increases | Lower initial payment |

| Federal Consolidation | Simpler payments | Limited savings | Easier management |

| Cosigner Refinance | Low credit borrowers | Cosigner risk | Better approval odds |

| Extended Term Refinance | Lower monthly payments | More interest long term | Better cash flow |

Mistakes Borrowers Make

Chasing Only the Lowest Monthly Payment

Lower payments can sometimes increase total repayment cost dramatically.

Ignoring Total Interest Paid

Some refinance terms stretch debt for many extra years.

Always calculate total repayment amount.

Refinancing Federal Loans Too Quickly

This mistake can permanently remove federal protections.

Applying Everywhere at Once

Multiple hard inquiries can temporarily lower credit scores.

Choosing Variable Rates Without Understanding Risk

Variable rates may rise sharply later.

Insider Insights Most Borrowers Never Hear

Banks love borrowers who:

- refinance repeatedly,

- extend repayment timelines,

- and prioritize monthly payment reduction over total debt cost.

Why?

Because longer repayment often means:

more interest profit for lenders.

The smartest borrowers focus on:

- lowering APR,

- reducing total interest,

- and improving financial flexibility.

Not just lowering the monthly payment.

MaintainMarket Expert Advice

If your refinance strategy only focuses on “smaller payments,” you may lose financially long term.

The smarter approach:

- improve your profile first,

- reduce utilization,

- compare lenders strategically,

- and refinance only when the numbers truly help you.

Timing matters more than most borrowers realize.

Why MaintainMarket Is Different

Most websites repeat generic refinance definitions.

MaintainMarket focuses on:

- real borrower problems,

- actual lender psychology,

- approval strategies,

- and long-term financial outcomes.

We explain:

- what lenders actually care about,

- how borrowers accidentally lose money,

- and how to refinance intelligently instead of emotionally.

Action Plan

Do Today

- Check current APR

- Review credit score

- Calculate debt-to-income ratio

- Compare refinance options

Do This Week

- Reduce credit utilization

- Organize income documents

- Use prequalification tools

Avoid

- Panic refinancing

- Ignoring total interest costs

- Variable rates without understanding risk

Check Before Applying

- Fixed vs variable APR

- Hard inquiry policies

- Federal protection loss

- Repayment flexibility

- Total repayment amount

Conclusion

Student loan refinancing can absolutely help.

But only when done strategically.

The goal is not just:

“lower payments.”

The real goal is:

- stronger financial control,

- lower long-term interest,

- improved cash flow,

- and reduced financial stress.

That’s what smart refinancing actually looks like in 2026.

Also read: Best Lenders for Low Credit Score USA (2026) | Fast Approval Options

FAQs – How to Refinance Student Loans

Q1. Does refinancing student loans hurt credit?

Temporary hard inquiries may slightly affect scores, but long-term savings can improve financial health

Q2. Can I refinance federal student loans?

Yes, but refinancing converts them into private loans and removes federal protections.

Q3. What credit score is needed for refinancing?

Many lenders prefer scores above 670, though some accept lower profiles with strong income.

Q4. Is fixed or variable rate better?

Fixed rates are safer long term. Variable rates can increase later.

Q5. Can refinancing lower monthly payments?

Yes, especially through lower APRs or longer repayment terms.

Q6. Can I refinance with bad credit?

Possibly, especially with a cosigner or improved income profile.

Q7. How many times can you refinance student loans?

There is usually no strict limit if you qualify.

Q8. What is the biggest refinancing mistake?

Refinancing federal loans without understanding lost protections.

People also searched for: Secured vs Unsecured Credit Card USA (2026): Which One Builds Credit Faster?

Also read: Loan Rejected? Get Emergency Cash with Bad Credit in USA (2026 Proven Hacks)

1 thought on “How to Refinance Student Loans in 2026 | Lower Monthly Payments Fast”