Secured vs unsecured credit card USA in 2026: learn which card improves your FICO score faster, lowers APR stress, and increases approval odds. Let’s talk about Secured vs Unsecured Credit Card USA in this article.

Quick Update Box

What changed in 2026:

US banks tightened approvals for low-credit borrowers due to rising defaults and debt usage.

Who is affected:

People with low FICO scores, thin credit history, high utilization, or recent loan rejections.

What to do immediately:

Check your credit utilization, compare secured vs unsecured cards carefully, and apply only after checking pre-approval eligibility.

Secured vs Unsecured Credit Card USA (2026)

Your credit card application gets rejected.

Your FICO score drops again.

And suddenly every bank starts offering cards with insane APR rates.

That’s exactly what many Americans are facing in 2026.

With inflation pressure, rising debt-to-income ratios, and stricter bank risk models, choosing the wrong credit card can hurt your financial future fast. The biggest confusion right now?

Should you choose a secured credit card or an unsecured credit card?

The answer depends on your credit profile, approval chances, and long-term credit-building strategy.

Featured Snippet

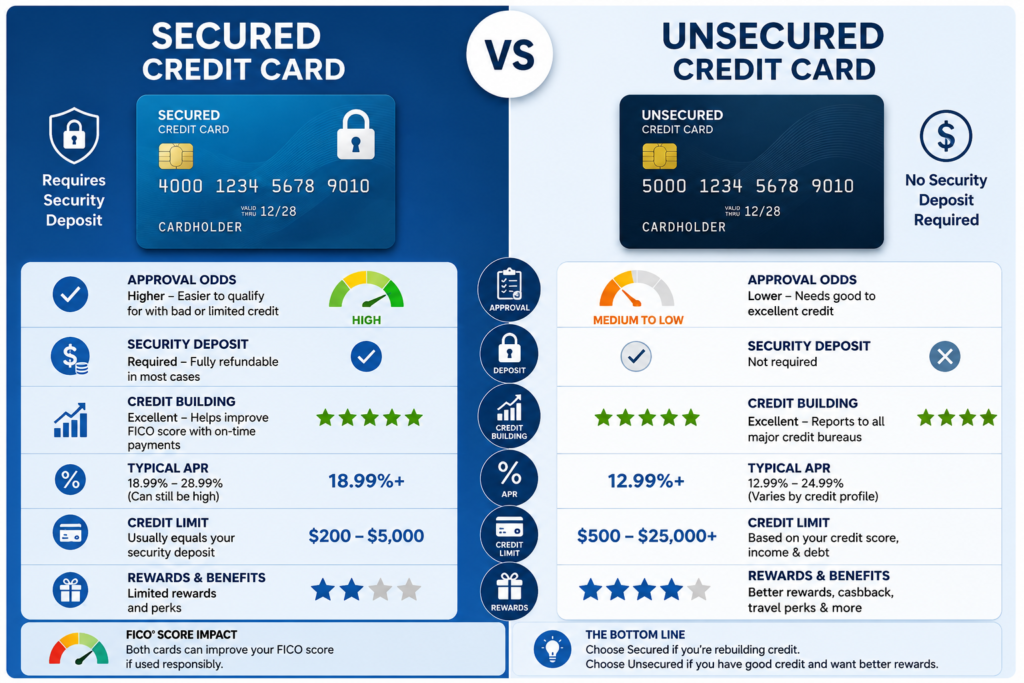

A secured credit card requires a refundable security deposit and is easier to get with poor or limited credit. An unsecured credit card does not require a deposit but usually needs a stronger FICO score and stable credit history. In 2026, secured cards are becoming the preferred option for Americans rebuilding credit after loan rejections or high debt utilization.

What’s Happening Right Now

In 2026, US lenders are becoming stricter.

Banks are:

- lowering approval rates,

- reducing credit limits,

- increasing APRs,

- and monitoring utilization more aggressively.

Many people with:

- FICO scores below 680,

- high revolving debt,

- missed payments,

- or recent hard inquiries

are struggling to get approved for traditional unsecured credit cards.

This is why secured credit cards are trending again across the USA.

Why This Is Happening

Banks are protecting themselves from rising default risks.

After increased consumer debt levels and higher borrowing costs, lenders are focusing heavily on:

- repayment behavior,

- utilization patterns,

- and debt-to-income ratios.

Here’s the hidden truth most people miss:

Banks do not just check your score.

They check your “risk behavior.”

Even someone with a 690 FICO score can get rejected if:

- utilization is too high,

- multiple cards were opened recently,

- income instability exists,

- or balances are close to limits.

Secured cards reduce bank risk because the deposit acts as collateral.

That’s why approvals are significantly easier.

Secured vs Unsecured Credit Card: Main Difference

| Feature | Secured Credit Card | Unsecured Credit Card |

|---|---|---|

| Security Deposit | Required | Not required |

| Approval Difficulty | Easier | Harder |

| Best For | Poor or limited credit | Good to excellent credit |

| Credit Limit | Usually based on deposit | Based on credit profile |

| Risk to Bank | Lower | Higher |

| APR | Can still be high | Varies widely |

| Credit Building | Excellent if used properly | Excellent if managed well |

| Rewards | Limited | Better cashback/travel rewards |

Who Is Affected Most

These groups are currently seeing the biggest impact:

People With Low FICO Scores

Scores under 650 are seeing stricter underwriting.

Young Adults

Thin credit history makes unsecured approvals harder.

Recent Loan Applicants

Multiple hard inquiries reduce approval confidence.

Americans Carrying High Balances

High utilization signals repayment stress.

Gig Workers & Freelancers

Irregular income patterns make lenders cautious.

Real Impact on Users

Here’s what is happening in real life:

- Higher APR offers

- Lower credit limits

- Instant application denials

- Security deposit requirements

- More pre-approval checks

Many consumers think rejection means “bad credit.”

But often it means:

- wrong timing,

- high utilization,

- or incorrect card selection.

Choosing the right card type matters more than ever in 2026.

What You Should Do Now

If Your FICO Score Is Below 650

Start with a secured credit card.

This can:

- rebuild payment history,

- lower utilization over time,

- and improve approval odds later.

If Your Score Is Above 700

You may qualify for better unsecured rewards cards with lower APR offers.

Keep Utilization Below 10%

This is one of the fastest ways to improve your score.

Avoid Multiple Applications

Too many hard inquiries can reduce approval chances.

Use Pre-Qualification Tools

Many issuers now allow soft-check eligibility reviews.

Also read: Loan with 500 CIBIL Score India – Real Ways to Get Approved Fast (2026 Guide)

Best Places to Check Credit Card Eligibility (USA)

Discover

Capital One

Chase

Bank of America

Before vs After Choosing the Right Card

| Situation | Before | After |

|---|---|---|

| Credit Utilization | 75% | Under 10% |

| Approval Odds | Low | Improved |

| APR Offers | Extremely high | More competitive |

| Credit Confidence | Poor | Stronger |

| FICO Trend | Falling | Recovering |

| Future Loan Eligibility | Weak | Better mortgage/auto loan chances |

Real-Life Case Study (USA)

Jake, a 27-year-old delivery driver from Texas, had:

- a 592 FICO score,

- two rejected unsecured applications,

- and 68% utilization.

Instead of applying repeatedly, he switched to a secured credit card with a $300 deposit.

What he changed:

- paid balances weekly,

- kept utilization under 10%,

- avoided hard inquiries,

- enabled auto-pay.

After 8 months:

- his score improved to 684,

- he pre-qualified for an unsecured cashback card,

- and reduced borrowing stress significantly.

Mistakes to Avoid

Applying for Multiple Cards Quickly

This signals desperation to lenders.

Ignoring APR

Many people focus only on rewards.

High APR debt destroys savings fast.

Maxing Out Cards

Even paying on time may not fully protect your score.

Missing Auto-Pay Setup

Late payments hurt FICO heavily.

Closing Old Cards Too Early

Credit age matters more than people realize.

Expert Insights Most Sites Don’t Tell You

Here’s the hidden reality:

Secured cards are no longer “bad credit cards.”

In 2026, they are becoming strategic financial tools.

Many financially smart users now:

- rebuild scores intentionally,

- improve utilization,

- then transition into premium unsecured rewards cards later.

Another important truth:

Rewards are useless if interest payments erase your gains.

A lower-risk credit strategy often beats aggressive rewards chasing.

Future Prediction for 2026–2027

Expect:

- stricter lending algorithms,

- AI-based approval systems,

- more income verification,

- and tighter utilization monitoring.

Consumers who manage:

- low balances,

- stable repayment,

- and fewer hard inquiries

will likely get the best offers.

Credit behavior is becoming more important than raw credit score alone.

Hidden Difference Most Americans Ignore

The biggest difference is not the deposit.

It’s how banks see your behavior.

A secured card user who:

- pays on time,

- keeps utilization low,

- and spends carefully

can sometimes look LESS risky than someone with a higher FICO score carrying heavy debt.

Banks now track:

- spending consistency,

- repayment timing,

- utilization spikes,

- and financial stability patterns.

This matters more in 2026 than ever before.

Why Many People Get Rejected for Unsecured Cards

Most people think:

“Good salary = approval.”

Not true anymore.

Banks now reject applicants because of:

- too many recent applications,

- rising living expenses,

- unstable income patterns,

- high card balances,

- or aggressive borrowing behavior.

Even a decent FICO score cannot always save an application.

The Psychological Trap of Rewards Cards

This is something most finance websites never mention.

Many unsecured rewards cards psychologically encourage overspending.

People chase:

- cashback,

- airline miles,

- reward points,

- welcome bonuses,

and slowly increase unnecessary spending.

Banks know this.

That’s why premium rewards cards are highly profitable for lenders.

A secured card often creates more disciplined spending habits.

Why Secured Cards Are Becoming Popular Again

In 2026, many Americans are prioritizing:

- survival,

- stability,

- and lower financial stress.

Instead of chasing rewards, users are focusing on:

- rebuilding credit,

- getting approved later for mortgages,

- lowering interest burden,

- and improving long-term financial health.

That’s why secured cards are quietly growing again.

Warning Signs You Should NOT Apply for an Unsecured Card Yet

Your utilization is above 30%

Banks may see you as overdependent on credit.

You were recently denied

Another hard inquiry may reduce approval odds further.

You carry balances monthly

High APR interest can spiral quickly.

You recently lost income

Lenders are becoming stricter with unstable earnings.

Your credit age is too short

Thin profiles often struggle with approvals.

Smart Strategy Used by Credit Experts

Many financially smart Americans now follow this strategy:

Step 1:

Open a secured card.

Step 2:

Keep utilization under 10%.

Step 3:

Enable auto-pay.

Step 4:

Wait 6–12 months.

Step 5:

Upgrade into unsecured cashback/rewards cards later.

This creates:

- stronger approval odds,

- healthier credit history,

- and lower long-term borrowing costs.

How Secured Cards Help Future Loans

A properly managed secured card can help with:

- mortgage approvals,

- auto loans,

- apartment rentals,

- insurance pricing,

- and even job background checks.

That’s because your credit report impacts more than borrowing.

The APR Problem Nobody Talks About

Many unsecured cards targeting low-credit users now have:

- very high APRs,

- hidden fees,

- annual charges,

- and penalty interest structures.

Some users end up paying hundreds extra yearly.

Always compare:

- APR,

- annual fee,

- late payment fee,

- balance transfer fee,

- and foreign transaction fee.

Not all “approved” cards are financially smart.

Red Flags to Watch Before Applying

Avoid cards that:

- promise “guaranteed approval,”

- hide fee structures,

- charge monthly maintenance fees,

- or do not report to all 3 credit bureaus.

Always verify reporting to:

- Experian,

- Equifax,

- and TransUnion.

Best Time to Apply for a Credit Card

Your approval odds improve when:

- utilization is low,

- recent inquiries are minimal,

- bills are paid on time,

- and income appears stable.

Timing matters more than most people realize.

The 10% Utilization Rule

Credit experts increasingly recommend keeping utilization below 10%.

For example:

If your limit is $500, try staying below $50 usage before statement closing date.

This single habit can improve your credit profile surprisingly fast.

Future Banking Trend in the USA

Expect more:

- AI-based approvals,

- real-time income analysis,

- spending behavior monitoring,

- and risk prediction systems.

Traditional credit scores alone may become less important over time.

Behavioral finance data is becoming the new approval weapon.

Also read: Instant Approval Credit Cards USA: Why You Get Denied & How to Fix Fast

Why MaintainMarket Is Different

Most finance websites only explain definitions.

MaintainMarket focuses on:

- real approval strategies,

- actual lender behavior,

- utilization psychology,

- and practical actions that improve financial outcomes.

We focus on:

- higher approval odds,

- lower borrowing stress,

- smarter credit usage,

- and long-term financial stability.

FAQ Section

Q1. Is a secured credit card better for bad credit?

Yes. Secured cards are easier to qualify for and help rebuild payment history and utilization behavior.

Q2. Does a secured credit card improve FICO score?

Yes, if the issuer reports to major credit bureaus and payments are made on time.

Q3. Can I upgrade from secured to unsecured later?

Many banks allow upgrades after several months of responsible usage.

Q4. What FICO score is needed for unsecured credit cards?

Most quality unsecured cards prefer scores above 670, though some options exist below that range.

Q5. Do secured cards require a hard inquiry?

Usually yes, but some issuers offer pre-qualification tools with soft checks first.

Q6. Which is safer during financial stress?

Secured cards are often safer because limits are controlled and approval standards are easier.

Q7. Can high utilization hurt even if I pay on time?

Yes. High utilization can still lower your FICO score significantly.

Q8. Can a secured card become unsecured automatically?

Some issuers review accounts after consistent on-time payments and may refund the deposit automatically.

Q9. Does closing a secured card hurt credit?

It can affect utilization and account age depending on your overall profile.

Q10. Is a secured card safer during recession fears?

For many users, yes. Lower limits often reduce overspending risk.

Q11. Which is better for beginners?

Secured cards are often easier and safer for first-time credit users.

Q12. Can immigrants or international students get secured cards easily?

Yes, many US banks offer secured cards for newcomers with limited credit history.

People searched for: Best Credit Cards for Bad Credit USA (300–580) That Actually Approve You in 2026

Final Action Plan

Do Today:

- Check your FICO score

- Review utilization percentage

- Compare secured vs unsecured eligibility

- Use pre-qualification tools

Do This Week:

- Lower balances below 10%

- Set up auto-pay

- Avoid unnecessary applications

Avoid:

- Maxing out cards

- Applying emotionally after rejection

- Ignoring APR terms

Check Before Applying:

- Annual fee

- APR

- Credit bureau reporting

- Upgrade eligibility

- Deposit refund terms

Also read: How to Get a Loan with 500 Credit Score (Guaranteed Best Options 2026) – USA

3 thoughts on “Secured vs Unsecured Credit Card USA (2026): Which One Builds Credit Faster?”