Looking for the best lenders for low credit score USA? Discover trusted lenders, approval strategies, hidden bank rules, and ways to improve approval odds fast.

“Split-screen thumbnail showing stressed borrower on one side and approved loan dashboard on the other, bold text saying ‘LOW CREDIT? STILL APPROVED?’ with dramatic finance-style lighting”

Introduction

You apply for a loan hoping things will finally get easier.

Then comes the rejection.

Sometimes it’s instant. Sometimes the bank makes you wait days just to say no.

For millions of Americans in 2026, this is becoming painfully common.

A low FICO score now affects:

- personal loans,

- credit card approvals,

- apartment applications,

- car financing,

- and even insurance pricing.

And the worst part?

Most people don’t even know why they’re getting rejected.

Banks rarely tell the full truth.

They send generic emails like:

“Unable to verify risk profile”

or

“Credit criteria not met.”

But behind the scenes, lenders are analyzing:

- utilization behavior,

- debt-to-income ratio,

- recent hard inquiries,

- spending patterns,

- and income consistency.

The good news?

Some lenders are still approving borrowers with lower credit scores — if you understand how the system actually works.

This guide breaks down:

- the best lenders for low credit score USA,

- how approvals really work,

- mistakes killing applications,

- and what you can do immediately to improve your chances.

Quick Answer Box

Best Lenders for Low Credit Score USA in 2026

| Lender Type | Best For | Typical Credit Flexibility |

|---|---|---|

| Online Personal Loan Lenders | Fast approvals | Moderate to low credit |

| Credit Union Loans | Lower APRs | Flexible underwriting |

| Secured Loan Providers | Easier approvals | Very low scores accepted |

| Peer-to-Peer Lending | Alternative approval systems | Moderate flexibility |

| Payday Alternatives | Emergency short-term help | Higher approval odds |

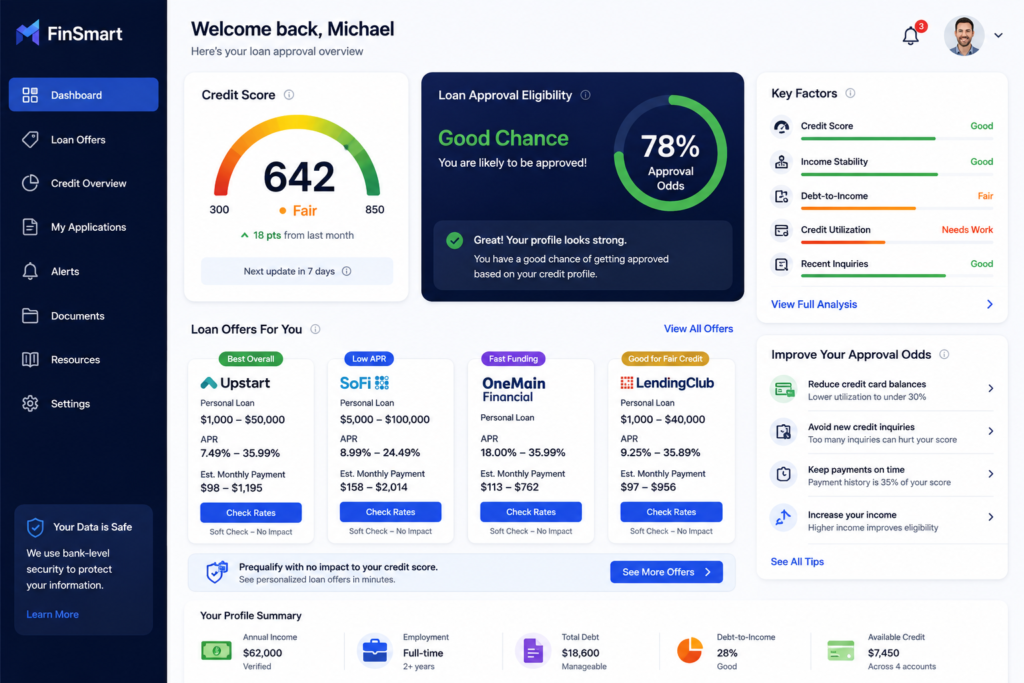

Borrowers with low credit scores improve approval chances significantly by:

- lowering utilization,

- avoiding multiple applications,

- checking prequalification offers,

- and applying with lenders that use soft credit checks first.

Why This Problem Happens

Banks Are More Risk-Averse in 2026

Most major lenders became stricter after rising defaults and increasing consumer debt.

Today, lenders don’t just care about your score.

They care about:

- repayment probability,

- spending discipline,

- income stability,

- and financial stress signals.

That’s why someone with a 640 score may get approved while another person with 690 gets denied.

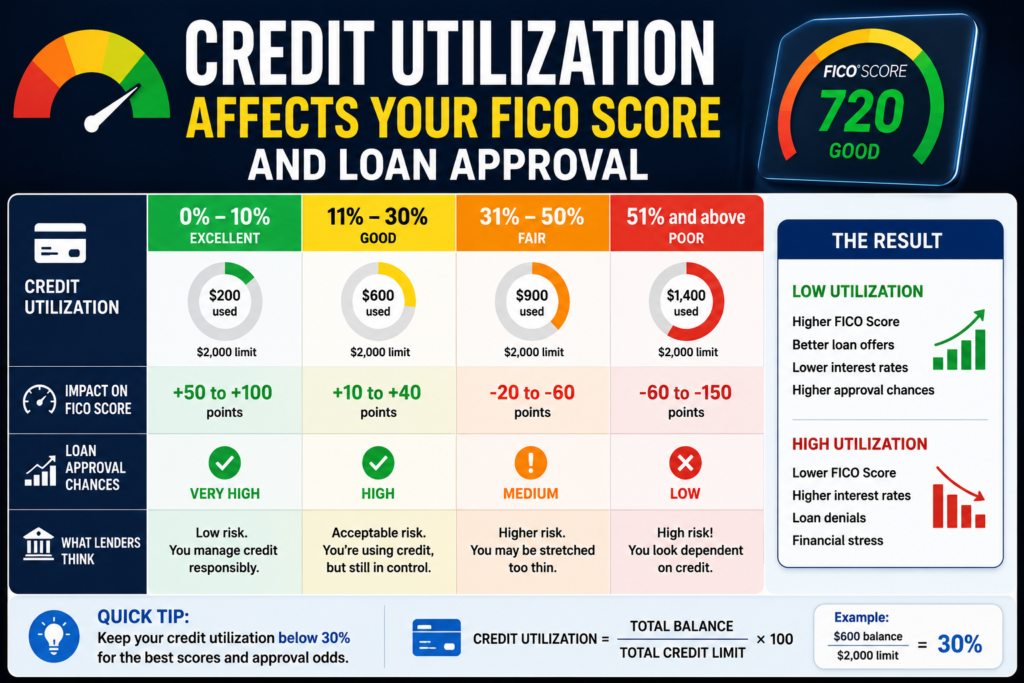

High Credit Utilization Is Quietly Destroying Approvals

One of the biggest hidden problems is utilization.

Many Americans are using:

- 50%,

- 70%,

- or even 90%

of their available credit.

To lenders, this signals financial pressure.

Even if payments are on time.

Too Many Applications Trigger Risk Warnings

Every hard inquiry tells lenders:

“This person urgently needs money.”

Multiple inquiries in a short period can destroy approval odds.

Best Types of Lenders for Low Credit Scores

Online Personal Loan Lenders

These lenders are often more flexible than traditional banks.

They usually:

- process applications faster,

- consider alternative financial data,

- and allow prequalification checks.

Best for:

- emergency expenses,

- debt consolidation,

- medical bills,

- short-term cash flow problems.

Common Features

- Faster decisions

- Higher approval odds

- Higher APRs for risky borrowers

Credit Unions

Credit unions are underrated.

Unlike major banks, many credit unions:

- focus more on member history,

- offer lower interest rates,

- and sometimes approve borrowers with imperfect credit.

Best for:

- lower APR loans,

- rebuilding trust,

- smaller loan amounts.

Secured Loan Providers

Secured loans use:

- vehicles,

- savings,

- or other assets

as collateral.

This reduces lender risk and improves approval odds significantly.

Best for:

- extremely low credit scores,

- rebuilding financial stability,

- larger approval amounts.

Peer-to-Peer Lending Platforms

Some platforms evaluate:

- employment consistency,

- education,

- income trends,

- and financial behavior.

Not just FICO score.

This can help borrowers rejected by traditional banks.

Also read: Secured vs Unsecured Credit Card USA (2026): Which One Builds Credit Faster?

Insider Insight — How Lenders Actually Think

Most borrowers misunderstand approvals completely.

Banks ask one question:

“Will this person become risky in the next 12 months?”

That’s it.

Not:

“Are they a good person?”

Not:

“Do they deserve help?”

Lenders care about probability.

Things that secretly hurt you:

- maxed-out cards,

- unstable bank balances,

- gambling transactions,

- overdraft patterns,

- frequent BNPL usage,

- and income inconsistency.

This is why many applications fail despite “fair” scores.

Step-by-Step Solution to Improve Approval Odds

Step 1 — Check Your Utilization

Keep credit usage below 10% if possible.

Credit Utilization=Total Credit LimitCredit Used×100

Example:

- Credit limit = $2,000

- Usage = $1,400

Utilization = 70%

That’s risky to lenders.

Step 2 — Use Prequalification Tools

Soft-check prequalification tools help avoid unnecessary hard inquiries.

Always check eligibility before applying.

Step 3 — Reduce Recent Applications

Wait before reapplying if recently denied.

Too many applications increase rejection probability.

Step 4 — Consider Smaller Loan Amounts

Borrowers requesting:

- smaller amounts,

- shorter terms,

- and realistic repayment structures

often get approved faster.

Step 5 — Add Stable Income Proof

Lenders love stability.

Showing:

- regular paychecks,

- freelance consistency,

- or recurring deposits

can help more than people realize.

Also read: Loan Rejected? Get Emergency Cash with Bad Credit in USA (2026 Proven Hacks)

Real-Life USA Case Study

How Marcus From Arizona Improved His Approval Odds

Marcus had:

- 589 FICO score,

- $11,000 credit card debt,

- 78% utilization,

- two recent rejections.

Instead of applying again immediately, he:

- paid utilization below 30%,

- stopped unnecessary spending,

- waited 60 days,

- used prequalification tools,

- and requested a smaller loan amount.

Result:

- Approved for a $4,500 installment loan

- APR lower than previous offers

- Credit score improved within months

The biggest change?

He stopped panic-applying everywhere.

Comparison Table — Best Lending Approaches

| Option | Approval Difficulty | APR Range | Speed | Best For |

|---|---|---|---|---|

| Online Lenders | Medium | High to medium | Fast | Emergency needs |

| Credit Unions | Easier | Lower | Medium | Affordable loans |

| Secured Loans | Easier | Medium | Medium | Very low credit |

| Payday Loans | Very easy | Extremely high | Instant | Last resort only |

| Peer-to-Peer Loans | Medium | Medium | Medium | Alternative approvals |

Mistakes People Make

Applying Emotionally After Rejection

This creates more inquiries and lowers approval chances further.

Ignoring APR

Some “easy approval” loans become financial traps.

Always compare:

- APR,

- fees,

- repayment penalties,

- and total repayment cost.

Believing “Guaranteed Approval” Ads

Many are misleading.

No legitimate lender guarantees approval without evaluating risk.

Taking Payday Loans Repeatedly

This can create a dangerous debt cycle.

Use only as absolute last resort.

MaintainMarket Expert Advice

The smartest borrowers in 2026 are not chasing approvals blindly.

They are:

- managing utilization strategically,

- improving cash flow,

- reducing inquiries,

- and applying selectively.

Approval strategy matters more than desperation.

One carefully timed application is often stronger than five rushed applications.

Why MaintainMarket Is Different

Most finance sites repeat generic advice.

MaintainMarket focuses on:

- real lender behavior,

- actual approval psychology,

- practical borrower strategy,

- and financial survival tactics that work in the real world.

We study:

- what gets people approved,

- what silently causes denials,

- and how Americans can improve financial stability without falling into debt traps.

Where to Place Affiliate Links Naturally

Best placements:

- after comparison tables,

- after lender explanations,

- inside “Check Eligibility” CTA sections,

- and after case studies.

Natural CTA examples:

- “Check your prequalification without affecting your score”

- “Compare rates before applying”

- “See if you qualify in minutes”

Action Plan

Do Today

- Check your FICO score

- Review utilization

- Stop unnecessary applications

- Use soft-check tools

Do This Week

- Lower balances

- Organize income proof

- Compare lender types carefully

Avoid

- Payday loan dependency

- Panic applications

- Ignoring APR terms

Check Before Applying

- Interest rate

- Origination fees

- Hard inquiry policy

- Minimum credit score

- Repayment flexibility

Conclusion

A low credit score does not mean you are financially finished.

But it does mean you need strategy.

In 2026, lenders are stricter, smarter, and more data-driven than ever before.

The people getting approved are usually the ones who:

- understand lender psychology,

- control utilization,

- apply strategically,

- and improve financial behavior before applying.

That’s the real difference.

Not luck.

Not magic.

Strategy.

FAQs

Q1. What is the easiest loan to get with bad credit?

Secured loans and certain online installment lenders are generally easier to qualify for.

Q2. Can I get approved with a 500 credit score?

Yes, but options may include higher APRs or secured lending structures.

Q3. Does checking eligibility hurt my score?

Soft-check prequalification usually does not affect your score.

Q4. What credit utilization is best for approvals?

Under 10% is ideal. Under 30% is generally safer.

Q5. Are online lenders safer than payday lenders?

Generally yes. Payday loans often have extremely high borrowing costs.

Q6. How long should I wait after rejection?

Usually 30–90 days depending on financial improvements made.

Q7. Can debt consolidation help approval odds later?

Yes, if it lowers utilization and improves repayment consistency.

Q8. Why did my loan get denied despite decent income?

Lenders also evaluate debt levels, spending behavior, utilization, and inquiry history.

People searched for: 10 Best Debt Consolidation Loans for Poor Credit in the USA (2026) – Easy Approval Options

Also read: Best Credit Cards for Bad Credit USA (300–580) That Actually Approve You in 2026

3 thoughts on “Best Lenders for Low Credit Score USA (2026) | Fast Approval Options”