Bank flagged your transaction? Learn the real reasons, how to fix it fast, and avoid account freezes. Step-by-step guide with real examples. In this article, let’s talk about why the bank flagged your payment.

Introduction

You try to make a payment.

Everything looks normal. You have money in your account. Your card works fine.

But suddenly —

“Transaction Declined”

or worse —

“Suspicious Activity Detected”

Now your heart starts racing.

You’re thinking:

- Did I get hacked?

- Is my account going to be frozen?

- Did I do something illegal without knowing?

Here’s the truth most banks don’t clearly tell you:

Your transaction wasn’t random. It was flagged for a reason.

And if you don’t fix it quickly, it can escalate into:

- Account freeze

- Payment blocks

- Even permanent restrictions

Let’s break this down properly — no fluff, no theory — just real reasons and real fixes.

Quick Answer Box (Featured Snippet)

Why did your bank flag your transaction?

Banks flag transactions when they detect unusual or risky activity, such as:

- Spending pattern change

- Large or sudden transactions

- International payments

- Unknown merchant

- Possible fraud signals

How to fix it fast:

- Verify the transaction via SMS/email

- Contact your bank immediately

- Confirm your identity

- Retry the payment

- Avoid repeating risky behavior

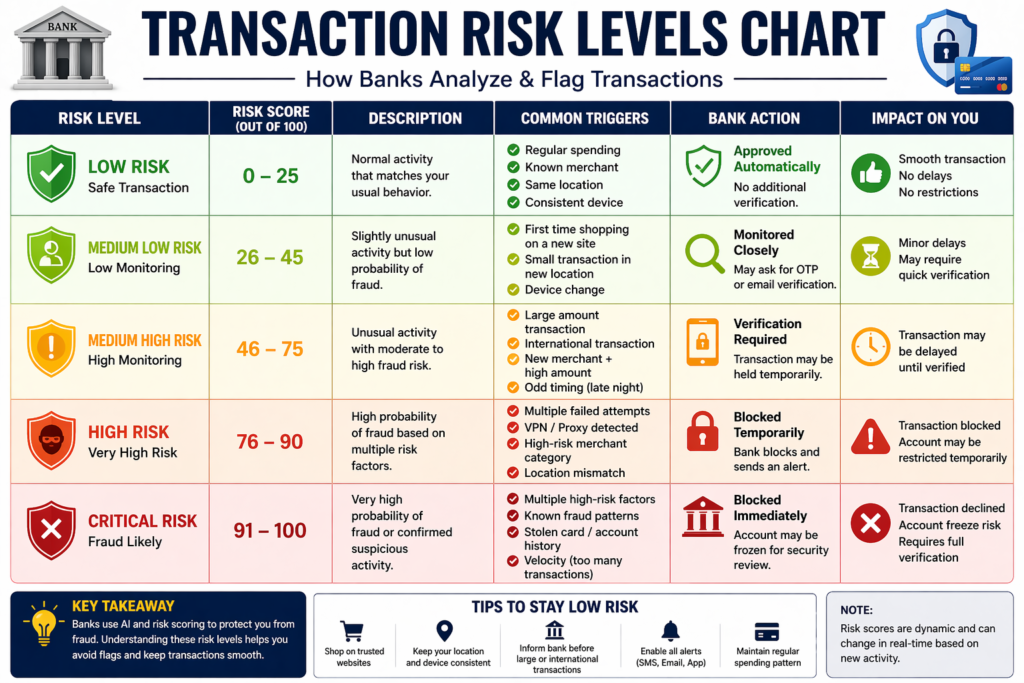

Why This Problem Happens (Real Reasons, Not Textbook)

Banks don’t “guess.”

They use AI-based fraud detection systems. And these systems are extremely sensitive.

Here’s what actually triggers them:

1. Sudden Change in Spending Pattern

If you usually spend $50–$100 and suddenly make a $2,000 payment…

Boom. Flagged.

2. First-Time Merchant Payment

New website, unknown seller, or low-trust business = risk.

Especially:

- Crypto sites

- Gambling platforms

- Foreign e-commerce

3. International Transactions

Even legit payments get flagged if:

- Country is high-risk

- Currency mismatch

- No prior history

4. Multiple Failed Attempts

Trying 3–4 times after decline?

Bank thinks:

“This looks like a fraud attempt.”

5. Odd Timing

Transactions at:

- 2 AM

- Different timezone

- Sudden location change

Raises red flags.

6. Card Not Used Recently

Inactive account suddenly active = suspicious.

7. Security Triggers (Behind the Scenes)

Banks track:

- Device used

- IP address

- Location

- Merchant category

You don’t see this — but they do.

8. Merchant Category Code (MCC) Risk

Every business has a category code.

High-risk categories:

- Crypto exchanges

- Online betting

- Adult platforms

- Forex trading sites

Even if the payment is legit → auto suspicion

9. Geo-Location Mismatch

Example:

- Your phone shows India

- Transaction request comes from USA

Bank thinks:

“Impossible movement → possible fraud”

10. Device Fingerprint Change

Banks track:

- Browser

- Device ID

- Operating system

New device = new risk.

11. Velocity Spending Pattern

Too many transactions in short time:

- 5 payments in 2 minutes

- Multiple merchants rapidly

System flags it as:

“Bot-like activity”

12. Card Not Present (CNP) Risk

Online transactions (no physical card) are:

- More risky

- More likely to be flagged

13. Expired or Recently Replaced Card Usage

Using:

- Old saved card details

- Recently replaced card

Triggers mismatch alerts.

14. Recurring Payments Suddenly Increasing

Example:

- Netflix = $10/month

- Suddenly = $100 charge

Flagged instantly.

15. Blacklisted Merchant Database

Banks maintain internal lists.

If merchant is:

- Previously reported

- Linked to fraud

Your transaction gets blocked — even if YOU trust it.

Advanced Fixes (Edge Cases)

Case 1: No Alert Received at All

What to do:

- Check spam email

- Check alternate phone number

- Login to net banking → security alerts

Still nothing?

→ Call bank immediately and ask:

“Was my transaction blocked by fraud system?”

Case 2: International Payment Keeps Failing

Fix:

- Enable international usage in card settings

- Inform bank before retry

- Use same device/location

Case 3: Subscription Payment Getting Blocked

Fix:

- Whitelist merchant via bank

- Use same card consistently

- Avoid switching payment methods frequently

Case 4: Payment Works on One Site but Not Another

Reason:

- Merchant risk score differs

Fix:

- Try trusted platform

- Use PayPal / secure gateway

Case 5: Account Temporarily Frozen

Do this:

- Call bank

- Submit ID proof

- Confirm recent transactions

- Wait for compliance clearance

Case 6: Card Blocked Completely

Fix:

- Request unblock

- Or issue new card

Insider Strategies to Avoid Flags Permanently

This is where you beat 90% of users.

Strategy 1: Warm-Up New Spending Behavior

Don’t jump from:

$50 → $2000

Instead:

- $200

- $500

- then large payment

Strategy 2: Build Merchant Trust Pattern

Repeat payments to same platforms:

- Amazon

- Apple

- Known brands

Bank builds confidence.

Strategy 3: Use One Primary Device

Avoid switching:

- Laptop → mobile → tablet

Consistency reduces flags.

Strategy 4: Maintain Stable Location

Traveling?

→ Inform bank.

Strategy 5: Avoid Midnight Transactions for Large Amounts

Time matters more than you think.

Strategy 6: Enable All Alerts

- SMS

- App

Speed = control.

Strategy 7: Keep KYC Updated

Outdated KYC = higher suspicion score.

Strategy 8: Use Trusted Payment Gateways

Safer options:

- PayPal

- Stripe

Data Table

Transaction Risk Score Breakdown

| Behavior | Risk Score | Impact |

|---|---|---|

| Same merchant repeat | Low | Safe |

| New merchant | Medium | Monitor |

| International payment | High | Likely flag |

| Large amount spike | Very High | Immediate block |

| Multiple retries | Critical | Account freeze risk |

Step-by-Step Solution (What Actually Works)

Step 1: Check Your Messages Immediately

Banks usually send:

- SMS

- App notification

Look for:

“Was this you?”

If yes → confirm it.

Step 2: Open Your Banking App

Most banks now allow:

- One-tap approval

- Fraud confirmation

Do it instantly.

Step 3: Call Customer Support (If Still Blocked)

Don’t wait.

Say clearly:

“I’m trying to approve a flagged transaction.”

They will:

- Verify your identity

- Remove the block

Step 4: Retry Transaction Properly

Important:

Do NOT:

- Spam retry

- Change amounts randomly

Just retry once after approval.

Step 5: Inform Bank Before Big Transactions (Pro Move)

Planning:

- Travel

- Large purchase

- International payment

Call bank first.

This reduces flag risk by 80%.

Insider Insights (How Banks Actually Think)

Here’s something most articles won’t tell you:

Banks don’t care about your intention.

They care about risk probability.

Their system works like this:

| Factor | Risk Level |

|---|---|

| Known merchant | Low |

| New merchant | Medium |

| International + new | High |

| Large amount + unusual | Very High |

If your transaction hits multiple risk factors → auto-flag

Even if it’s YOU.

Real-Life Case Study (USA)

John (California) tried to buy a $1,500 laptop from a new website.

What happened:

- First-time merchant

- High amount

- Late-night purchase

Result:

- Transaction declined

- Card temporarily blocked

What he did:

- Ignored SMS

- Retried 4 times

Result:

- Account flagged for fraud

Fix:

- Called bank

- Verified identity

- Got account restored in 24 hours

Lesson:

The problem wasn’t the purchase — it was the pattern.

Comparison Table (Fix Options)

| Situation | Best Action | Time to Fix |

|---|---|---|

| SMS alert received | Confirm immediately | 1–2 minutes |

| App notification | Approve in app | Instant |

| No alert | Call bank | 5–15 minutes |

| Account frozen | Full verification | 24–48 hours |

| International block | Pre-inform bank | Preventive |

Mistakes People Make

1. Ignoring Bank Alerts

Big mistake.

Bank assumes fraud → blocks everything.

2. Retrying Multiple Times

This makes it worse.

System thinks:

“Someone is forcing access.”

3. Using Multiple Devices

Laptop + phone + VPN = high risk

4. Not Updating Contact Info

Missed alerts = blocked account

5. Panic Transferring Money

Moving funds suddenly can trigger more flags.

6. Using VPN During Payments

Big red flag.

7. Trying Different Cards Repeatedly

Looks like fraud testing behavior.

8. Ignoring Small Declines

Small declines lead to bigger blocks.

9. Sharing OTP Carelessly

Even one mistake = account risk profile increases.

10. Using Suspicious Websites

Cheap deals = high risk.

11. Frequent Refund Requests

Too many refunds → suspicious pattern.

12. Using Someone Else’s Card Frequently

Mismatch in user behavior.

MaintainMarket Expert Advice

If you want to avoid this problem long-term:

- Keep transaction patterns consistent

- Use trusted merchants first

- Avoid VPN during payments

- Inform bank before unusual activity

- Enable app notifications

Think like the bank’s AI system.

If something looks unusual — it WILL react.

Why MaintainMarket is Different

Most websites tell you:

“Contact your bank.”

That’s surface-level advice.

Here, you learned:

- Actual triggers

- Real system logic

- Preventive strategies

- Behavioral fixes

This is what actually solves the problem.

Action Plan (Do This Now)

If your transaction is flagged right now:

- Check SMS/email

- Approve transaction

- Open bank app

- Call support if needed

- Retry once

For future:

- Inform bank before large payments

- Avoid risky platforms

- Keep activity consistent

Conclusion

A flagged transaction is not a punishment.

It’s a warning system.

But if you ignore it or react wrongly, it can turn into:

- Account freeze

- Payment failure

- Financial stress

Handle it smartly, and it becomes a 2-minute fix.

Handle it poorly, and it becomes a 2-day problem.

FAQs – Bank Flagged Your Payment

Q1. Can a bank block my account for one transaction?

Yes, if it looks highly suspicious or risky.

Q2. How long does it take to unflag a transaction?

Usually minutes, but can take up to 48 hours.

Q3. Will I lose my money if transaction is flagged?

No, money stays safe unless fraud is confirmed.

Q4. Why is my debit card declined but I have money?

Likely due to security flag, not balance issue.

Q5. Do international transactions always get flagged?

Not always, but they have higher risk.

Q6. Can VPN cause transaction issues?

Yes, it can trigger fraud detection.

Q7. Should I retry a failed transaction?

Only once after confirming with bank.

Q8. How to prevent this in future?

Maintain consistent behavior and inform bank before unusual activity.

Q9. Why is my transaction flagged even after approval?

Because system still detects risk pattern.

Q10. Can banks reverse flagged transactions?

Yes, if fraud is confirmed.

Q11. Does flagged transaction affect credit score?

No direct impact.

Q12. How many flags before account gets blocked?

Depends on severity, not count.

Q13. Can I whitelist a merchant permanently?

Yes, in many banks.

Q14. Why does my card work offline but not online?

Online = higher fraud risk.

Q15. Is it safe to retry after decline?

Only after confirming with bank.

Q16. Can flagged transactions trigger audits?

In rare cases, yes (especially large amounts).

People searched for: You Earn Well But Still Got Rejected? 5 Hidden Reasons Banks Won’t Approve Your Loan USA

Also read: 15 Best Side Hustles From Home USA (Earn $1000+/Month) – Real Guide 2026

2 thoughts on “Bank Flagged Your Payment? Here’s What It Really Means (And What to Do Immediately)”