Banks Won’t Approve Your Loan: Got rejected for a loan even with a high income? Discover the real reasons banks deny applications and how to fix it fast in the USA. In this article, let’s talk about Hidden Reasons Banks Won’t Approve Your Loan.

Introduction – Hidden Reasons Banks Won’t Approve Your Loan

You checked all the obvious boxes.

Good salary. Stable job. No major financial crisis.

And still… loan rejected.

It doesn’t just feel confusing — it feels unfair.

Most people think:

“If I earn well, I should get approved.”

That’s not how banks think.

And until you understand how lenders actually judge you, you’ll keep getting rejected — no matter how much you earn.

Let’s break this down properly.

Quick Answer (Featured Snippet)

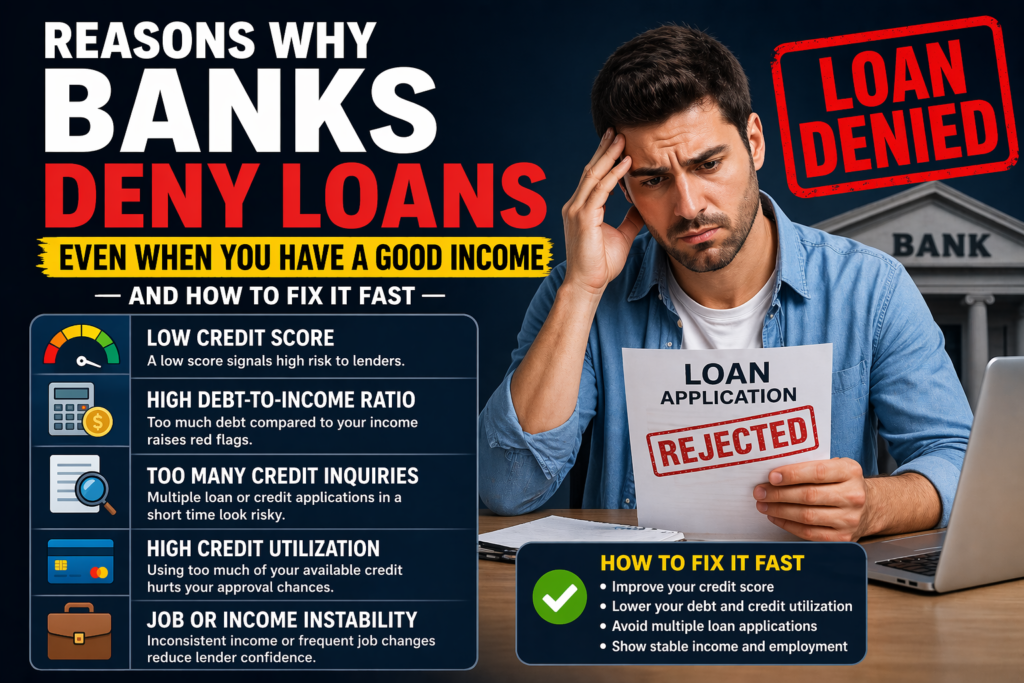

Banks deny loans even if you have a good income because they prioritize risk, not earnings. The most common reasons include:

- Low or unstable credit score (like FICO Score)

- High debt-to-income ratio

- Too many recent credit inquiries

- High credit card utilization

- Thin or risky credit history

- Job instability or inconsistent income pattern

To fix this:

- Reduce your debt ratio below 35%

- Keep credit utilization under 30%

- Avoid multiple loan applications

- Improve your credit profile using reports from Experian, Equifax, and TransUnion

Why This Problem Happens (Real Reasons — Not Textbook)

Here’s the truth most banks won’t say directly:

Income is just ONE factor. Risk is EVERYTHING.

Let’s break the real reasons.

1. Your Debt Is Already Too High

Even if you earn $6,000/month…

If you’re already paying:

- $1,500 in credit cards

- $1,200 in rent

- $800 in car loans

You’re already stretched.

Banks calculate something called:

Debt-to-Income Ratio (DTI)

If it crosses ~40–45%, you’re risky.

2. Your Credit Score Looks “Okay” — But Not Safe

People think:

“700 is good, right?”

Yes… but not for all lenders.

- 650–699 = risky zone for many banks

- 700–740 = average approval

- 750+ = premium borrower

Even a small drop can hurt approval chances massively.

3. Too Many Loan Applications (Desperation Signal)

Applied for:

- 2 credit cards

- 1 personal loan

- 1 BNPL

In 2 months?

Banks see this as:

👉 “This person urgently needs money — risky.”

Each application = hard inquiry = lower approval chances.

4. High Credit Card Usage (Silent Killer)

Even if you pay on time…

If your credit usage is:

- 70% or more → Red flag

- 90% → High risk

Example:

Limit: $10,000

Used: $8,000

This alone can get your loan rejected.

5. Income Stability Matters More Than Amount

Banks prefer:

- $4,000 stable income (2+ years)

OVER - $8,000 unstable freelance income

If your income fluctuates, lenders assume uncertainty.

6. Thin Credit File (No Proof You Can Handle Debt)

If you:

- Never used credit cards

- Never took loans

Banks don’t trust you yet.

No history = No proof = No approval.

7. Internal Bank Risk Models (Hidden Algorithms)

Banks don’t just check reports.

They use:

- Behavioral data

- Spending patterns

- Risk scoring models

You might look fine externally but fail internally.

8. Recent Job Switch (Even With Higher Salary)

This kills approvals more than people expect.

If you:

- Changed job in last 3–6 months

- Switched industries

- Moved from salaried → freelance

Banks see:

👉 “Unstable income phase”

Even if your salary increased, lenders prefer:

- 2+ years consistency in same field

9. Industry Risk Factor (Yes, This Exists)

Not all jobs are treated equally.

High-risk industries (in lender models):

- Startups

- Commission-based sales

- Gig economy (Uber, DoorDash)

- Entertainment / freelance

Low-risk industries:

- Government

- Healthcare

- Tech (stable companies)

Same income — different approval outcomes.

10. Bank Relationship History

If you’re applying in a bank where:

- You have low balance history

- Frequent overdrafts

- Irregular transactions

Your chances drop.

Banks trust existing behavior more than documents.

11. Loan Amount vs Income Mismatch

Example:

Income: $4,000/month

Loan applied: $50,000

Even if technically possible…

Bank thinks:

👉 “Over-leveraging risk”

Result:

❌ Rejection or lower approved amount

12. Existing Unused Credit Limits

This one surprises people.

If you already have:

- $20,000 credit card limit (unused)

Bank thinks:

👉 “They can borrow anytime → future risk”

So they reduce or reject new loans.

13. Payment Patterns (Not Just On-Time)

Even if you pay on time…

If you:

- Always pay minimum due

- Delay until last day

- Revolve balance constantly

Banks see:

👉 “Financial stress behavior”

This silently reduces approval chances.

14. Geographic Risk (Location-Based Decisions)

Yes, your location matters.

Banks analyze:

- Default rates in your ZIP code

- Economic conditions

- Employment trends

High-risk area = stricter approval

15. Banking Behavior (AI-Based Risk Detection)

Modern lenders track:

- Spending spikes

- Gambling transactions

- Crypto volatility

- Sudden withdrawals

These trigger:

👉 “Behavioral risk flags”

Even with good income, you get rejected.

Step-by-Step “Approval Boost System” (Advanced Strategy)

This is what actually moves you from rejected → approved.

Phase 1: Clean-Up (0–15 Days)

- Check all 3 credit reports

- Dispute errors immediately

- Pay down credit cards below 30%

- Avoid any new applications

Goal:

👉 Remove visible red flags

Phase 2: Strengthen Profile (15–45 Days)

- Increase bank balance consistency

- Show stable income deposits

- Avoid unnecessary spending spikes

- Pay more than minimum dues

Goal:

👉 Build “trust signals”

Phase 3: Smart Application (After 30–45 Days)

- Apply with 1 lender only

- Choose lender matching your profile

- Pre-check eligibility (soft check tools)

- Apply for realistic loan amount

Goal:

👉 Maximize approval probability

Insider Lending Psychology (Real Truth)

Here’s how lenders actually rank you internally:

| Factor | Weight (Approx) |

|---|---|

| Credit Score | 30–35% |

| Debt-to-Income | 20–25% |

| Credit Behavior | 15–20% |

| Income Stability | 10–15% |

| Recent Activity | 10% |

Notice something?

👉 Income is NOT the top factor.

That’s why people earning less sometimes get approved — and high earners don’t.

Real-Life Case Study 2 (High Income Rejection)

Sarah (California)

- Income: $9,000/month

- Credit Score: 720

- 5 credit cards (80% utilization)

- Applied for 2 loans in 1 month

Result:

❌ Rejected by 2 banks

Fix Applied:

- Reduced utilization to 28%

- Waited 40 days

- Applied with online lender

Final Result:

✅ Approved $20,000 loan at better terms

Smart Tools & Options Comparison (USA)

| Option | Best For | Approval Chance | Interest Rate | Speed |

|---|---|---|---|---|

| Traditional Banks | Strong profiles | Medium | Low | Slow |

| Online Lenders | Moderate profiles | High | Medium | Fast |

| Credit Unions | Balanced profiles | High | Low-Medium | Medium |

| Peer-to-Peer | Risky profiles | Medium | High | Fast |

Hidden Mistakes That Kill Approval Instantly

- Applying after salary drop

- Closing old credit cards (reduces history)

- Ignoring small late payments

- Taking BNPL loans frequently

- Applying for maximum eligible amount

MaintainMarket Deep Insight

Here’s something most people miss:

👉 Banks reward predictability, not ambition

If your finances look:

- Stable

- Controlled

- Predictable

You win.

If they look:

- Aggressive

- Risky

- Uncertain

You get rejected.

Ultra-Clear Action Plan (High Conversion)

If you were rejected TODAY, do this:

Day 1–3

- Pull credit report

- Identify 2 biggest issues

Day 4–15

- Reduce card usage

- Fix errors

Day 15–30

- Maintain stable bank activity

- Avoid new debt

Day 30–45

- Apply smartly (1 lender only)

Step-by-Step Solution (What Actually Works)

Let’s fix this practically.

Step 1: Check Your Credit Report (Non-Negotiable)

Use:

- Experian

- Equifax

- TransUnion

Look for:

- Errors

- Late payments

- High utilization

Fixing errors alone can boost approval chances.

Step 2: Lower Your Debt-to-Income Ratio

Target:

👉 Below 35%

How:

- Pay off small debts first

- Avoid new EMIs

- Increase income proof (side gigs)

Step 3: Reduce Credit Utilization

Golden rule:

👉 Keep under 30%

Best hack:

- Pay card before statement date (not just due date)

Step 4: Stop Applying Everywhere

After rejection:

👉 Wait at least 30–45 days

Then apply strategically.

Step 5: Apply with the Right Lender

Not all lenders are same.

- Banks = strict

- Online lenders = flexible

- Credit unions = moderate

Choose based on your profile.

Step 6: Add a Co-Signer (Game Changer)

If your profile is weak:

👉 Add someone with strong credit

Approval chances can double instantly.

Insider Insights: How Banks Actually Think

Banks don’t care about your income emotionally.

They think in one line:

👉 “Will this person repay us safely?”

They check:

- Probability of default

- Behavior patterns

- Financial discipline

Income is just supporting evidence.

Your behavior is the real decision-maker.

Real-Life Case Study (USA)

John (Texas)

- Income: $5,500/month

- Credit Score: 690

- Credit Card Usage: 85%

- Applied for 3 loans in 2 months

Result:

❌ Rejected everywhere

What he changed:

- Paid down cards to 25% usage

- Waited 45 days

- Applied via credit union

Final Result:

✅ Approved $12,000 personal loan at 11% APR

Comparison Table (What Matters vs What You Think Matters)

| Factor | What You Think | What Actually Matters |

|---|---|---|

| Income | High income = approval | Stability + consistency |

| Credit Score | 700 is enough | 740+ preferred |

| Applications | More attempts = better | More attempts = risky |

| Credit Cards | Paying minimum is fine | Low utilization is key |

| Debt | Manageable in mind | DTI < 35% required |

Mistakes People Make

- Applying immediately after rejection

- Ignoring credit report errors

- Maxing out credit cards

- Taking multiple small loans

- Assuming salary guarantees approval

MaintainMarket Expert Advice

If you remember one thing, remember this:

👉 Control your risk profile, not just your income.

Before applying:

- Clean your credit

- Reduce visible debt

- Space out applications

This alone can change outcomes dramatically.

Why MaintainMarket is Different

Most websites:

- Give textbook advice

- Repeat “improve credit score”

We focus on:

- Real lender psychology

- Practical fixes

- Fast approval strategies

Because that’s what actually works.

Action Plan (Do This Now)

- Check your credit report today

- Reduce credit usage below 30%

- Stop applying for 30 days

- Pay off smallest debts first

- Apply with a targeted lender

- Consider co-signer if needed

Follow this, and your approval chances will improve fast.

Conclusion

Getting rejected despite a good income isn’t bad luck.

It’s a mismatch between:

👉 How YOU see your finances

👉 How BANKS evaluate risk

Fix that gap — and approvals become predictable.

Final Thought (Stronger Close)

You’re not getting rejected because you don’t earn enough.

You’re getting rejected because:

👉 Your financial profile doesn’t match lender expectations

Fix that — and approvals become predictable, not stressful.

FAQs – Banks Won’t Approve Your Loan USA

Q1. Can I get a loan with high income but low credit score?

Yes, but approval chances drop significantly. You may need a co-signer.

Q2. How long should I wait after loan rejection?

At least 30–45 days before applying again.

Q3. Does checking my credit score hurt it?

No. Only hard inquiries affect your score.

Q4. What is the ideal credit score for loan approval in USA?

740+ gives the best approval rates.

Q5. Can multiple loan applications hurt me?

Yes. Too many applications signal financial stress.

Q6. What is the safest debt-to-income ratio?

Below 35% is ideal.

Q7. Do banks verify income stability?

Yes. Stability matters more than amount.

Q8. Can I fix loan rejection quickly?

Yes, if the issue is utilization or application behavior.

Q9. Does changing jobs affect loan approval?

Yes. Recent job changes reduce approval chances due to instability risk.

Q10. Can high credit limit hurt loan approval?

Yes. It increases potential future debt risk.

Q11. Do banks check spending habits?

Yes. Modern lenders use behavioral analysis models.

Q12. Is freelance income considered risky?

Yes, unless consistent for 2+ years.

Q13. Can I get approved after multiple rejections?

Yes, if you fix the underlying issues and wait before reapplying.

Q14. Does location affect loan approval?

Yes, based on regional risk data.

Q15. What is the fastest way to improve approval chances?

Reduce credit utilization and avoid multiple applications.

People searched for: 15 Best Side Hustles From Home USA (Earn $1000+/Month) – Real Guide 2026

Also read: $100? Start Investing in USA (2026 Easy Ways For Beginner)

Insurance Claim Under Investigation What To Do USA (2026): Why It Happens & How to Get Paid Faster

3 thoughts on “You Earn Well But Still Got Rejected? 5 Hidden Reasons Banks Won’t Approve Your Loan USA”