Struggling with a low credit score? Learn the credit utilization hack that can boost your score in 30 days. Step-by-step strategy used by smart borrowers. In this article, let’s talk about One Utilization Hack Can Boost Your Credit Score.

Introduction

If your credit score is stuck below 650, you’re not alone.

Most people think the problem is late payments, old debt, or collections. But here’s the truth most banks won’t tell you:

Even if you pay on time, your credit score can still stay low.

Why?

Because of one silent factor: credit utilization.

I’ve seen people jump 40–100 points without paying off all their debt — just by fixing this one thing.

And if you understand this properly, you can literally control how lenders see you… within weeks.

Quick Answer Box (Featured Snippet)

The fastest way to boost your credit score using utilization:

- Keep your credit utilization below 30% (ideally under 10%)

- Pay your credit card before the statement closing date

- Split payments into multiple small payments (not one big one)

- Increase your credit limit (without increasing spending)

This alone can boost your score within 15–45 days.

Why This Problem Happens (Real Reasons)

Let’s break something most people misunderstand.

Your credit card company doesn’t report your payment…

They report your balance at a specific time.

Example:

- Credit limit: $1,000

- You spend: $800

- You pay it off fully before due date

Sounds perfect, right?

Wrong.

If the bank reports when your balance was $800 →

Your utilization = 80%

That makes you look risky, even though you paid everything.

That’s why people say:

“I pay on time but my score is still low.”

Step-by-Step Credit Utilization Hack (Real Strategy)

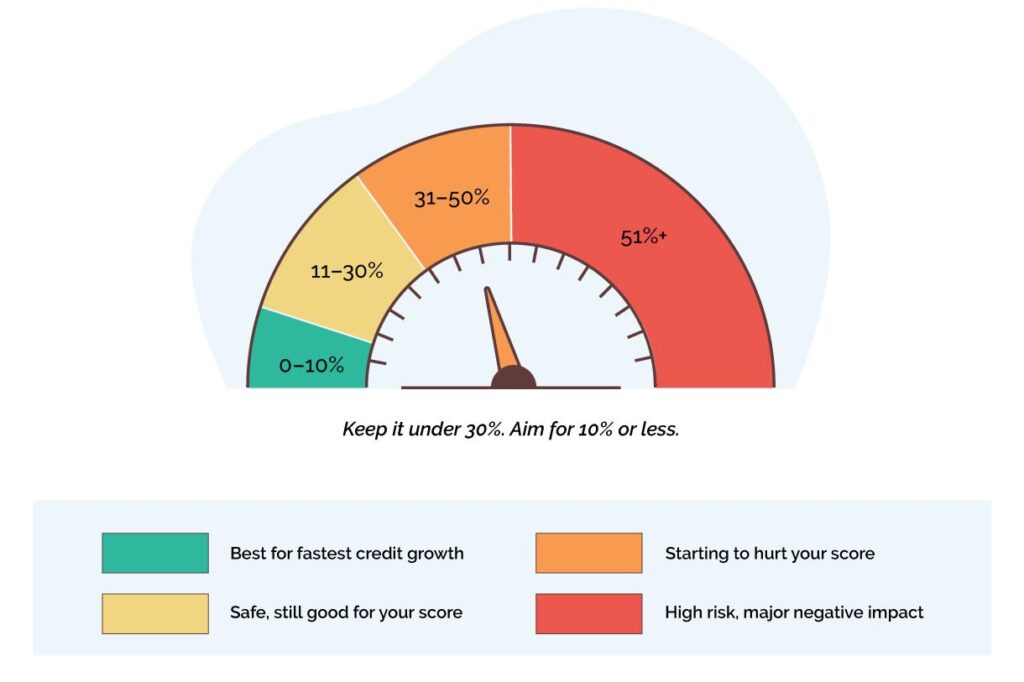

Step 1: Understand the 30% Rule (But Don’t Stop There)

- Safe zone: Below 30%

- Ideal zone: Below 10%

- Dangerous zone: Above 50%

If your usage is high, your score drops — instantly.

Step 2: Learn Your Statement Closing Date

This is where the real game begins.

- Payment due date ≠ reporting date

- Reporting date = statement closing date

Action:

Call your bank or check your app and find this date.

Step 3: Pay BEFORE the Statement Closes

This is the biggest hack.

Instead of paying on due date…

Pay 3–5 days BEFORE statement closing.

That way:

- Reported balance = LOW

- Score = HIGH

Step 4: Use the “Multiple Payment Strategy”

Don’t wait till the end of the month.

Do this:

- Spend → Pay immediately

- Spend → Pay again

This keeps your utilization artificially low at all times.

Banks love this.

Step 5: Request a Credit Limit Increase

This is underrated.

Example:

- Old: $500 used out of $1,000 → 50% utilization

- New: $500 used out of $3,000 → 16% utilization

Same spending. Huge score improvement.

Insider Insight: How Lenders Actually Think

Banks don’t just check if you pay.

They check:

- Are you dependent on credit?

- Are you maxing out cards?

- Do you look desperate for credit?

High utilization = “This person might default.”

Low utilization = “This person is financially stable.”

That’s why someone with $5,000 debt can have a higher score than someone with $500.

Real-Life Case Study (USA)

- Name: Jason (Texas)

Starting Score: 612

Problem:

- 2 credit cards

- Always paid on time

- Utilization ~70%

What he changed:

- Paid balances before statement closing

- Kept usage under 10%

- Requested limit increase

Result (45 days):

| Factor | Before | After |

|---|---|---|

| Utilization | 70% | 9% |

| Score | 612 | 684 |

| Approval Odds | Low | High |

No debt payoff. Just smart timing.

2. Name: Amanda (California)

Score: 645 → 705 (in 30 days)

What she was doing wrong:

- Using 80–90% of card

- Paying on due date

What changed:

- Paid before statement

- Kept 1 card at 2%

- Increased limit

Result:

- +60 points jump

- Approved for better credit card

Comparison Table (Strategies vs Impact)

| Strategy | Difficulty | Speed | Impact |

|---|---|---|---|

| Paying on due date | Easy | Slow | Low |

| Paying before statement | Medium | Fast | High |

| Keeping under 30% | Easy | Medium | Medium |

| Keeping under 10% | Medium | Fast | Very High |

| Credit limit increase | Medium | Fast | Very High |

Credit Utilization Hacks (Most People Don’t Know)

1. The “1% Utilization Trick” (Ultra Boost Strategy)

Most blogs say “keep it under 10%.”

That’s decent.

But if you really want to push your score faster:

- Keep one card reporting a small balance (1–3%)

- Keep all other cards at 0 balance

Example:

- Card 1: $10 balance on $1,000 limit (1%)

- Card 2: $0

- Card 3: $0

Why this works:

Credit models like FICO don’t love 0 across all cards.

They prefer to see controlled usage, not inactivity.

This tiny trick alone can give you a few extra points boost.

2. The “All Cards Maxed vs One Card Maxed” Trap

Here’s something most people never realize:

- 50% utilization on 1 card ≠ 50% utilization across all cards

Scenario A:

- 1 card at 90%

- 2 cards at 0%

Scenario B:

- 3 cards at 30%

Even if total utilization is similar, Scenario A looks riskier.

Why?

Because lenders track:

- Total utilization

- Per-card utilization

Fix:

Never let a single card go above 30%, even if overall usage is low.

3. The “Reporting Date Manipulation” Strategy

You already know about statement dates.

Now go one level deeper:

Some banks report multiple times per month, not just once.

That means:

- If you spike usage mid-month → it may still get reported

- Even if you pay before closing

Smart move:

- Keep utilization low throughout the month, not just at the end

This is how disciplined users maintain 750+ scores consistently.

4. The “Credit Limit Stacking” Method

Instead of relying on 1–2 cards…

Build multiple credit lines strategically.

Why?

More total limit = lower utilization automatically.

Example:

| Cards | Total Limit | Usage | Utilization |

|---|---|---|---|

| 1 card | $1,000 | $500 | 50% |

| 4 cards | $4,000 | $500 | 12.5% |

Same spending. Massive difference.

5. Use Business Credit Cards (Hidden Advantage)

Most people ignore this.

Many business credit cards:

- Don’t report utilization to personal credit

- Still give you high limits

Result:

- You can spend more

- Without hurting your personal score

This is a powerful move if you’re scaling income or business.

6. The “Utilization Reset Timing Trick”

If your score dropped due to high utilization:

Don’t panic.

Utilization has no memory.

That means:

- Fix it this month → score can bounce back next month

Unlike late payments, this is reversible fast.

7. Balance Transfer Strategy (Smart Reset)

If you’re stuck with high utilization:

- Move balance to a new card with higher limit

Example:

- Old: $2,000 / $2,500 → 80%

- New: $2,000 / $8,000 → 25%

Instant improvement in how lenders see you.

8. The “Zero Before Apply” Rule

Planning to apply for:

- Credit card

- Loan

- Mortgage

Do this 30 days before:

- Reduce utilization to under 5%

Why?

Because lenders check your latest reported data, not your intentions.

9. Psychological Hack: Spend Like Debit, Not Credit

People misuse credit cards because they think:

“I’ll pay later.”

That’s where utilization spikes.

Instead:

- Treat credit cards like UPI/debit

- Spend → Pay immediately

This naturally keeps utilization low without effort.

10. The “Small Balance Reporting Trick”

Instead of reporting $0:

Let $5–$20 report on one card.

Why?

- Shows activity

- Improves scoring behavior

- Avoids “inactive user” profile

Deep Insight: Why This Hack Works So Fast

Most credit factors take time:

- Payment history → months/years

- Age of credit → years

But utilization?

Updates every billing cycle.

That’s why it’s the fastest lever in your control.

Additional Mistakes That Kill Your Score

Let’s go deeper here:

1. Thinking “Available Limit = Safe to Use”

Just because you can spend doesn’t mean you should.

2. Ignoring Authorized User Accounts

If you’re added to someone’s high-utilization card → your score drops too.

3. Using BNPL (Buy Now Pay Later) Carelessly

Some BNPL providers now report usage → increases utilization-like risk.

4. Maxing Out Cards Before Big Purchases

Even temporary spikes can get reported and hurt score.

5. Not Tracking Credit Reports Monthly

You’re blind if you don’t track.

MaintainMarket Advanced Advice (High-Level Strategy)

If you’re serious about fixing your credit:

Focus on this order:

- Utilization (Immediate impact)

- Payment history (Consistency)

- Credit mix (Long-term)

- Credit age (Passive growth)

Most people do this in reverse — that’s why they stay stuck.

Bonus: 30-Day Credit Boost Blueprint

Week 1:

- Pull credit report

- Identify high utilization cards

Week 2:

- Pay balances down to under 10%

- Set reminders before statement date

Week 3:

- Apply for credit limit increase

Week 4:

- Let low balance report (1–3%)

Expected Outcome:

- +30 to +80 points improvement

Mistakes People Make

- Paying only on due date

- Using full limit and paying later

- Ignoring statement closing date

- Closing old credit cards

- Applying for too many cards at once

These quietly destroy your score.

MaintainMarket Expert Advice

If your score is below 650:

Focus on utilization first before anything else.

Why?

Because it’s the fastest variable you can control.

You can’t erase history overnight.

But you can manipulate utilization within days.

Why MaintainMarket is Different

Most websites tell you:

“Pay on time”

“Keep utilization low”

That’s basic advice.

Here, you learned:

- Timing strategy

- Reporting behavior

- Psychological scoring system

This is how real credit improvement works.

Action Plan (Follow This Exactly)

Week 1:

- Check credit limits

- Find statement dates

Week 2:

- Start paying before closing date

Week 3:

- Keep utilization under 10%

Week 4:

- Request limit increase

Result:

Expect visible score movement within 30–45 days.

Conclusion

Your credit score is not just about how much you owe.

It’s about how smartly you manage what you owe.

Most people stay stuck because they follow the wrong timing.

Once you fix utilization, everything changes:

- Higher score

- Better approvals

- Lower interest rates

This is not theory.

This is how people actually win with credit.

FAQs

1. What is the best credit utilization percentage?

Below 10% is ideal for maximum score boost.

2. Does paying twice a month help?

Yes, it keeps your reported balance low.

3. How fast can utilization improve score?

15–45 days depending on reporting cycle.

4. Is 30% utilization bad?

Not bad, but not optimal. Aim for under 10%.

5. Should I close unused credit cards?

No, it reduces your total limit and increases utilization.

6. Does increasing credit limit hurt score?

No, it usually helps if spending stays same.

7. Can I boost score without paying full debt?

Yes, by reducing utilization strategically.

8. Does utilization reset every month?

Yes, it updates with every reporting cycle.

If your score is low mainly due to utilization:

You don’t need years.

You need strategy + timing.

Start with:

- Paying before statement

- Keeping under 10%

- Increasing limits smartly

That’s how people quietly move from 600 → 700+ without struggle.

People searched for: How to Get a High Credit Limit Card in 2026 (Banks Are Quietly Changing Approval Rules)

Also read: Bank Flagged Your Payment? Here’s What It Really Means (And What to Do Immediately)

You Earn Well But Still Got Rejected? 5 Hidden Reasons Banks Won’t Approve Your Loan USA

2 thoughts on “One Utilization Hack Can Boost Your Credit Score in 30 Days”