Reasons Your Loan Got Rejected: Got rejected for a loan despite a high credit score? Discover the real reasons lenders deny applications and how to fix them fast in 2026. In this article, let’s talk about why loan application rejected with good credit, if your loan got rejected read this full helpful article.

Introduction

You checked your credit score.

It’s 720. Maybe even 760.

You felt confident. Applied for a loan.

And then… rejected.

No clear explanation. Just a generic message:

“Your application could not be approved at this time.”

This is where most people get confused. Because nobody tells you the truth:

A good credit score is important—but it’s NOT enough.

Banks don’t approve loans based on your score alone. They look at your entire financial behavior like a risk analyst.

And sometimes, even “good” borrowers get rejected.

Let’s break down exactly why this happens—and how to fix it fast.

Quick Answer (Featured Snippet Box)

You can get rejected for a loan even with a good credit score because lenders evaluate multiple factors beyond your score, including:

- High debt-to-income (DTI) ratio

- Unstable or insufficient income

- Too many recent credit inquiries

- Thin credit history

- Errors in application or documents

- Employment instability

- Risk patterns in spending behavior

Fix: Lower your DTI, stabilize income, avoid multiple applications, and reapply strategically.

Why This Problem Happens (Real Reasons, Not Textbook)

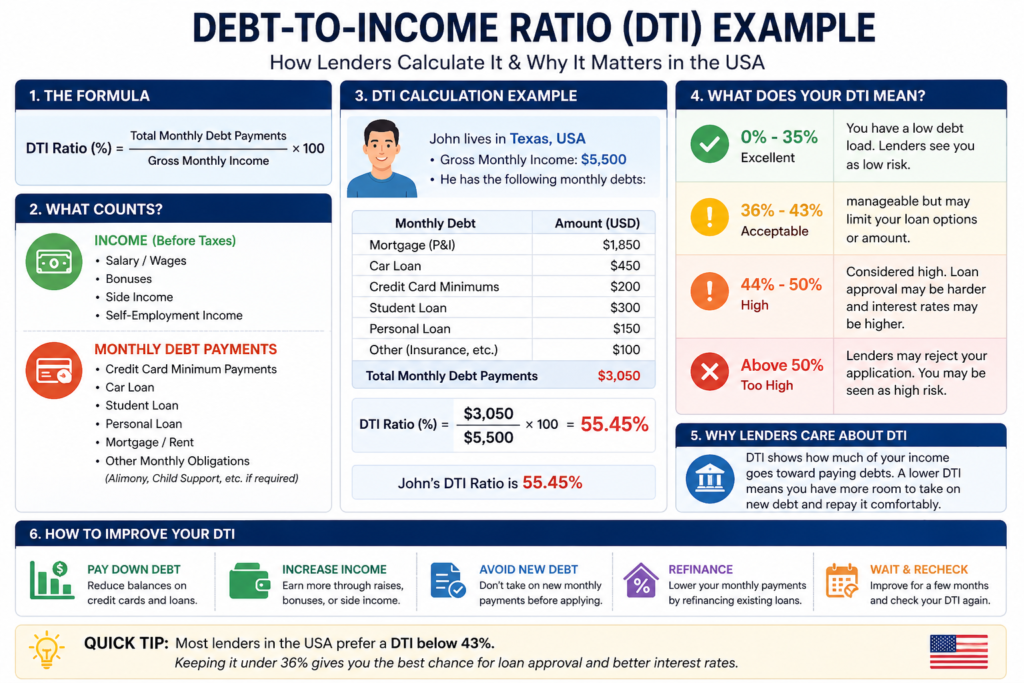

1. Your Debt-to-Income Ratio Is Too High

Even if your score is 750…

If your monthly income is $4,000 and your existing EMIs/loans are $2,000…

That’s a 50% DTI.

Banks see this and think:

“This person is already financially stretched.”

Ideal DTI: Under 35%

2. Income Doesn’t Match the Loan Size

A big mistake people make:

- Applying for $50,000 loan

- With $3,000/month income

Even with good credit, lenders ask:

“Can this person realistically repay this?”

3. Too Many Recent Loan or Credit Applications

Applied for 3–4 loans in a short time?

Each application creates a hard inquiry.

Lenders interpret this as:

“Desperate for money = Higher risk”

4. Unstable Job or Freelance Income

Especially in the USA:

- Frequent job switches

- Gig income without consistency

This reduces trust—even if your credit score is excellent.

5. Thin Credit Profile

You may have a good score, but:

- Only 1 credit card

- Very short history

This is called a “thin file”

Lenders prefer borrowers with proven long-term behavior

6. Errors in Your Application

Simple mistakes can kill approval:

- Wrong income entry

- Mismatch in documents

- Missing employer details

Banks don’t “correct”—they reject.

7. Risk Signals Banks Don’t Publicly Explain

This is insider-level:

Banks analyze patterns like:

- Sudden large deposits

- High credit utilization

- Gambling/crypto-heavy transactions

- Frequent overdrafts

These don’t always affect your score—but affect approval.

Step-by-Step Solution (Practical Fix)

Step 1: Check Your Debt-to-Income Ratio

Formula:

Monthly Debt ÷ Monthly Income

If above 40% → reduce debt first.

Step 2: Reduce Credit Utilization

Keep usage below 30% of limit

Example:

Limit = $10,000 → Use under $3,000

Step 3: Stop Applying Everywhere

Wait at least 30–45 days before reapplying.

Step 4: Increase Approval Odds Strategically

- Apply for smaller loan first

- Choose lenders matching your profile

- Use pre-qualification tools

Step 5: Show Stable Income

If freelance:

- Show 6–12 months bank statements

- Maintain consistent inflow

Step 6: Fix Errors Immediately

Check:

- Credit report

- Application details

- Income proof

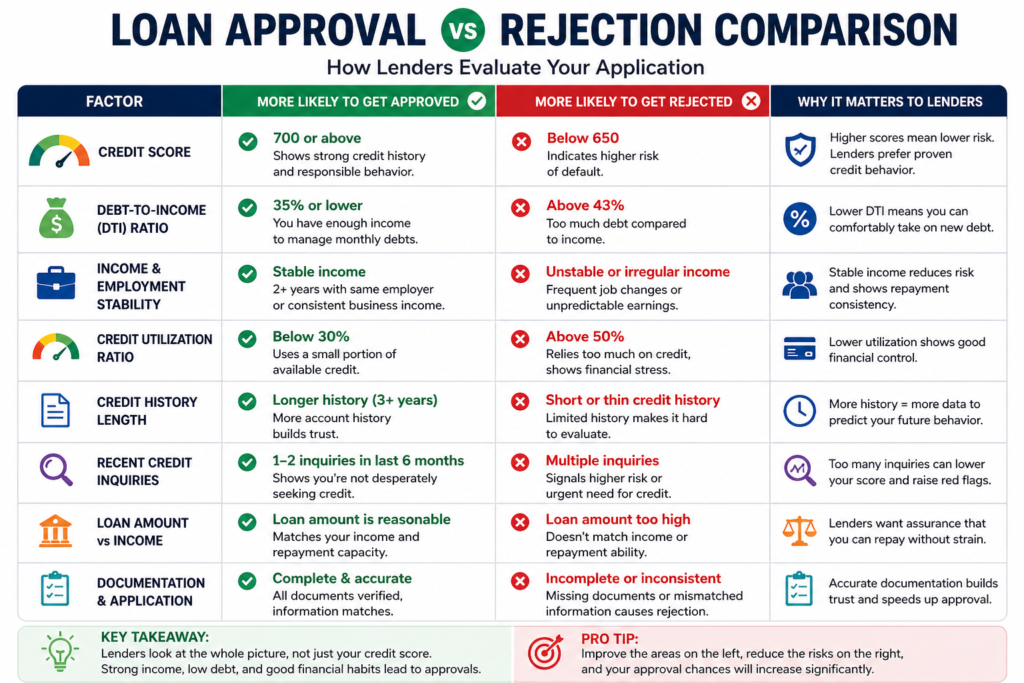

Insider Insights: How Lenders Actually Think

Banks don’t ask:

“Is this person good?”

They ask:

“What’s the probability this person will default?”

They calculate risk using:

| Factor | Weight |

|---|---|

| Credit Score | 30% |

| Income Stability | 25% |

| Debt Load | 20% |

| Credit Behavior | 15% |

| Application Signals | 10% |

Even if your score is perfect…

Fail in 2–3 other areas → rejection.

Real-Life Case Study (USA)

Case: John, Texas

- Credit Score: 742

- Income: $3,800/month

- Existing Debt: $1,900/month

- Applied Loan: $25,000

Result: Rejected

Why?

- DTI = 50%

- 3 recent credit inquiries

Fix Applied:

- Paid off $800 debt

- Waited 45 days

- Applied for $15,000

Result: Approved

Comparison Table: Why You’re Rejected vs Fix

| Problem | What It Means | Fix |

|---|---|---|

| High DTI | Over-leveraged | Pay off debt |

| Low income | Can’t handle EMI | Apply smaller loan |

| Too many inquiries | Risk behavior | Wait 30–45 days |

| Thin credit file | Lack of history | Build credit |

| Unstable job | Income risk | Show consistency |

| Application errors | Data mismatch | Recheck details |

Your Credit Utilization Spiked Recently

Even if your score is still high…

If your credit usage jumped from:

- 20% → 70% in last 1–2 months

Lenders see this as a stress signal

They think:

“Something changed financially”

Fix:

Bring utilization below 30% before applying again.

Hidden Reason #1: You’re Applying With the Wrong Lender

This is a big one most people ignore.

Example:

- Big banks → prefer stable salaried employees

- Online lenders → accept moderate risk

- Credit unions → more flexible

So even if you’re eligible…

wrong lender = rejection

Hidden Reason #2: Recent Big Financial Changes

Lenders get nervous if you recently:

- Changed jobs

- Moved cities/states

- Opened new accounts

- Closed old accounts

Even if positive, it creates uncertainty

Hidden Reason #3: Your Bank Statements Don’t Match Your Profile

This is insider-level:

You say:

- Income: $5,000

But bank shows:

- Irregular deposits

- Cash-heavy transactions

- No clear salary pattern

That’s a red flag.

Hidden Reason #4: You’re Asking for Unsecured Loan Without Strong Backup

Personal loans = high risk for banks.

Even with good credit:

- No assets

- No collateral

- Moderate income

→ Rejection probability increases

Fix Strategy (What Smart Borrowers Do)

Instead of applying directly again, do this:

Strategy 1: Pre-Qualification First

Use tools that show approval chances without hard inquiry.

Strategy 2: Apply for Smaller Loan First

Example:

- Want $30,000 → Apply for $10,000

- Build repayment history

- Then go bigger

Strategy 3: Use Co-Applicant or Guarantor

This instantly improves:

- Approval chances

- Interest rates

Especially useful for:

- Freelancers

- Low-income applicants

Strategy 4: Time Your Application

Best time to apply:

- After salary increment

- After debt reduction

- After 2–3 months stable banking

Timing matters more than people think.

Lender Psychology Deep Dive (Very Important)

Banks use something called:

“Behavioral Risk Modeling”

They track patterns like:

- Do you spend everything you earn?

- Do you carry balances every month?

- Do you rely on credit heavily?

Even with high score…

If your behavior = “credit dependent”

→ You look risky

Real Scenario Breakdown (What Actually Happens Internally)

When you apply:

- System checks credit score

- Algorithm checks DTI

- Flags risk signals

- Underwriter reviews profile

- Decision = Approve / Reject

Most rejections happen at Step 3 (Risk Flags)

NOT because of credit score.

Advanced Comparison Table (Approval Strategy)

| Situation | Wrong Move | Smart Move |

|---|---|---|

| High DTI | Apply anyway | Reduce debt first |

| Freelance income | Show estimate | Show 6-month proof |

| High credit usage | Ignore | Pay down before applying |

| Urgent money need | Multiple applications | Target 1 lender |

| Large loan | Direct apply | Step-up approach |

Additional Mistakes That Kill Approval

- Applying right after job change

- Closing old credit cards before loan

- Ignoring soft pre-check tools

- Not reading rejection reason codes

- Applying emotionally (urgency mode)

MaintainMarket Advanced Insight

Here’s something most people don’t realize:

Loan approval is a timing game + positioning game

Not just eligibility.

Two people with same profile:

- One gets approved

- One gets rejected

Why?

Presentation + timing + lender match

Micro Action Plan (Fast Recovery in 15–30 Days)

Week 1:

- Check credit report

- Calculate DTI

Week 2:

- Pay down balances

- Stop new applications

Week 3:

- Stabilize bank transactions

Week 4:

- Apply strategically (not randomly)

Bonus: If You Need Money Urgently (Backup Options)

If rejection already happened:

- Credit union loans (higher approval chances)

- Secured loans (against FD/car)

- Balance transfer options

- Employer salary advance

Mistakes People Make

- Applying to multiple lenders at once

- Ignoring DTI completely

- Assuming credit score = approval

- Applying for maximum loan amount

- Not checking credit report errors

MaintainMarket Expert Advice

If your loan gets rejected despite a good score:

Don’t panic. Don’t apply again immediately.

Instead:

- Diagnose the real reason

- Fix 1–2 core issues

- Reapply smartly

Most approvals fail due to strategy—not eligibility

Why MaintainMarket Is Different

Most sites tell you:

“Improve your credit score.”

That’s surface-level advice.

MaintainMarket focuses on:

- Real lender psychology

- Approval strategies (not theory)

- Practical fixes that work in real life

Because approval isn’t about numbers—

It’s about how lenders interpret your behavior.

Action Plan (Do This Now)

- Check your DTI ratio

- Reduce credit usage below 30%

- Stop new applications for 30 days

- Verify your credit report

- Apply for smaller loan first

- Choose lender based on your profile

Follow this—and your approval chances jump significantly.

Conclusion

A good credit score opens the door—but it doesn’t guarantee entry.

Banks look deeper:

- Your income

- Your behavior

- Your risk pattern

If you understand this, you stop guessing—and start getting approved.

FAQs – Reasons Your Loan Got Rejected

Q1. Can I get rejected with a 750 credit score?

Yes, due to high DTI, low income, or risk signals

Q2. How long should I wait after loan rejection?

At least 30–45 days before reapplying

Q3. Does loan rejection hurt credit score?

Slightly, due to hard inquiry.

Q4. What is the biggest reason for rejection?

High debt-to-income ratio.

Q5. Can I reapply immediately?

Not recommended—it reduces approval chances.

Q6. Do all lenders check the same factors?

No, but most evaluate similar risk metrics.

Q7. Is income more important than credit score?

In many cases, yes.

Q8. Can I fix loan rejection fast?

Yes—if you identify and correct the core issue.

Q9. Why do banks reject without explanation?

Because internal risk models are confidential.

Q10. Does income proof matter more than score?

Yes, especially for large loans.

Q11. Can self-employed people get rejected more?

Yes, due to income inconsistency.

Q12. What is a “thin credit file”?

Limited credit history despite good score.

Q13. Does bank balance affect loan approval?

Yes, it shows financial stability.

Q14. Can I fix rejection in 30 days?

Yes, if issue is DTI or utilization

People searched for: Missed a Payment? Your Credit Score Can Suffer for Years – How Long Late Payment Affects Credit Score USA

Also read: 7 Silent Reasons Destroying Your FICO Score Right Now – Fico score dropped without reason

7 Best Credit Builder Apps in the USA That Can Boost Your Score Even If It’s Below 600

Thank you for your valuable feedback! I’m glad you found the article useful. I appreciate your support and look forward to hearing your thoughts on future posts as well.