Fico score dropped without reason: Your FICO score dropped without warning? Discover the hidden reasons lenders don’t tell you and step-by-step ways to fix your credit score fast. In this article. let’s talk about how fico score dropped without reason.

Introduction

You check your credit score expecting it to go up…

Instead, it drops. Hard.

No missed payments. No new loans. Nothing unusual.

And now you’re stuck wondering — what just happened?

This is one of the most frustrating financial situations. Because when your score drops without an obvious reason, it feels like you’ve lost control.

But here’s the truth most people don’t realize:

Your credit score never drops “randomly.” There’s always a trigger — it’s just not always visible.

In this guide, I’ll break down:

- The hidden reasons your score dropped

- What banks actually look at (not what blogs say)

- And how to recover your score fast

2. Quick Answer Box (Featured Snippet)

Why did my FICO score drop suddenly?

Your FICO score can drop suddenly due to:

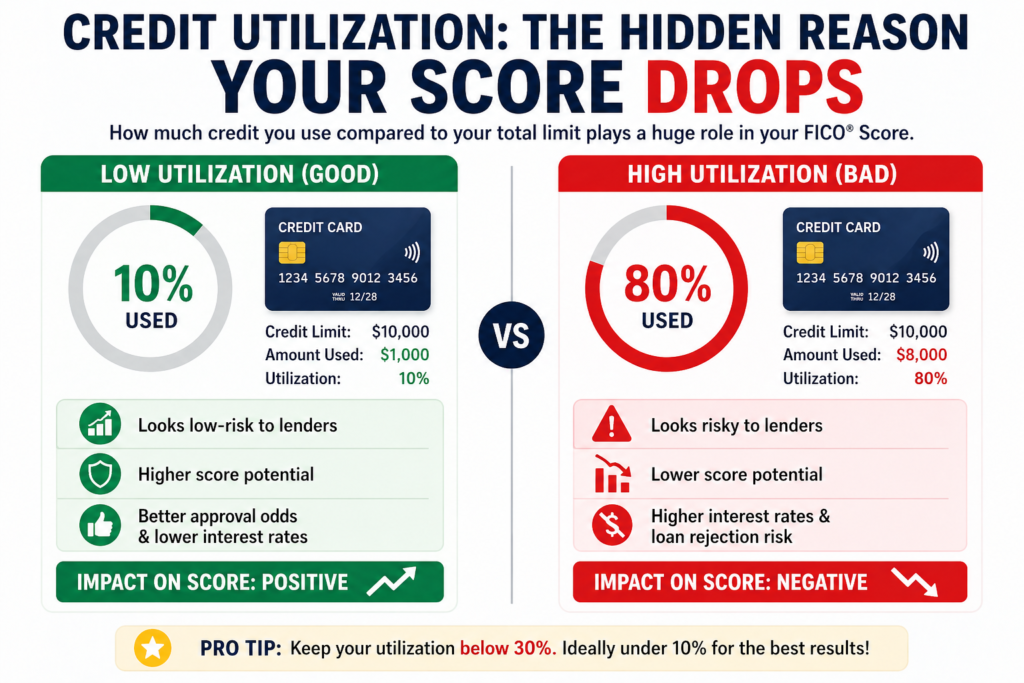

- Increased credit utilization

- New hard inquiries

- Closed accounts (by you or the bank)

- Late payments (even 1 day reported)

- Errors in your credit report

- Changes in credit mix or account age

How to fix it fast:

- Check your credit report for errors

- Reduce credit utilization below 30% (ideally 10%)

- Avoid new credit applications

- Pay all dues before statement date

- Dispute inaccuracies immediately

3. Why This Problem Happens (Real Reasons)

Let’s get real — banks don’t “punish randomly.” They react to risk signals.

Here are the actual triggers:

1. Credit Utilization Spike (Biggest Silent Killer)

Even if you paid on time…

If your card usage went from 20% → 70%, your score can drop.

Example:

- Limit: $5,000

- Earlier usage: $1,000

- Now: $3,500

That alone can drop your score by 30–80 points.

2. Statement Date Trap (Most People Ignore This)

You might think:

“I paid my bill, so I’m safe.”

Wrong.

Banks report balance at statement date, not payment date.

So even if you pay later, the high usage gets reported.

3. Hard Inquiry (Invisible Damage)

Applied for:

- Credit card

- Personal loan

- BNPL

Each application = hard inquiry

1–2 inquiries = fine

3–5 in short time = risky behavior

4. Old Account Closed

Either:

- You closed it

- Bank closed inactive account

This reduces:

- Credit history length

- Total available credit

Both hurt your score.

5. Hidden Late Payment Reporting

Sometimes:

- You paid 2–3 days late

- Bank reports it anyway

Even one late mark can drop 50–100 points.

6. Credit Report Error (More Common Than You Think)

Wrong data like:

- Loan you never took

- Duplicate accounts

- Incorrect balances

And boom — your score drops.

4. Step-by-Step Solution (Real Fix)

Step 1: Pull Your Credit Report

Use:

- Experian

- Equifax

- TransUnion

Check:

- Accounts

- Payment history

- Credit limits

Step 2: Fix Utilization Immediately

Target:

- Below 30% (minimum)

- Below 10% (ideal)

Pro tip:

Pay before statement date, not due date.

Step 3: Stop Applying for Credit

No:

- New cards

- Loans

- BNPL

Give your profile time to stabilize.

Step 4: Dispute Errors Fast

If something looks wrong:

- File dispute online

- Attach proof

Resolution usually takes 7–30 days

Step 5: Increase Available Credit (Smart Move)

Options:

- Request credit limit increase

- Keep old cards active

This reduces utilization ratio instantly.

5. Insider Insights (How Lenders Actually Think)

Banks don’t care if you’re “responsible.”

They care about risk patterns.

Here’s what triggers them:

- Sudden spending spike = possible financial stress

- Multiple credit applications = desperate borrowing

- High utilization = dependency on credit

Their logic:

“Will this person default in the next 6 months?”

Your score reflects that prediction.

6. Real-Life Case Study (USA)

Case: John (California)

- Score: 742 → dropped to 682

- No missed payments

What happened?

- Bought furniture on credit card ($4,000)

- Utilization jumped to 78%

Fix:

- Paid down to 15%

- Requested limit increase

Result:

- Score back to 730 in 45 days

7. Comparison Table (Solutions)

| Problem Trigger | Impact Level | Fix Time | Best Solution |

|---|---|---|---|

| High utilization | Very High | 15–45 days | Pay down balance |

| Hard inquiries | Medium | 30–90 days | Stop applications |

| Closed account | Medium | 2–3 months | Keep old accounts active |

| Late payment | Very High | 3–6 months | On-time payments only |

| Credit report error | High | 7–30 days | Dispute immediately |

8. Mistakes People Make (That Make the Drop Worse)

This is where most people unknowingly destroy their chances of recovery.

1. Paying Only on Due Date

You think you’re being responsible.

But lenders don’t care about due date — they care about statement balance.

So even if you pay on time:

- High balance gets reported

- Score drops anyway

2. Closing Old Credit Cards

People think:

“I don’t use this card, let me close it.”

Big mistake.

You lose:

- Credit history length

- Total available limit

Both are critical for your score.

3. Applying for Multiple Loans/Cards

After a score drop, panic kicks in.

People apply everywhere:

- Credit cards

- Personal loans

- BNPL

This adds multiple hard inquiries → making things worse.

4. Ignoring Small Late Payments

Even a delay of a few days can sometimes get reported.

And one late mark can:

- Stay for years

- Drop score significantly

5. Not Checking Credit Report

Most people only check the score.

But the real issue is inside the report.

If you don’t check:

- You won’t spot errors

- You won’t fix the root cause

9. Action Plan (Do This Immediately)

If your score just dropped, follow this exactly:

Step 1: Check Your Credit Report

Don’t guess — verify.

Look for:

- High balances

- Unknown accounts

- Errors

Step 2: Calculate Your Utilization

Use this formula:

(Total Credit Used ÷ Total Credit Limit) × 100

Target:

- Below 30% (safe)

- Below 10% (ideal)

Step 3: Pay Down Balances NOW

Don’t wait for due date.

Pay immediately — especially before statement date.

Step 4: Pause All Credit Applications

No:

- New cards

- Loans

- EMI offers

Give your profile time to stabilize.

Step 5: Dispute Any Errors

If you find anything wrong:

- File dispute online

- Add supporting proof

Fixing one error can boost your score instantly.

Step 6: Keep Old Accounts Active

Use them occasionally:

- Small purchases

- Pay immediately

This keeps your history alive.

10. Mistakes People Make

- Paying only on due date (not statement date)

- Closing old credit cards

- Applying for multiple loans at once

- Ignoring small late payments

- Not checking credit report regularly

11. MaintainMarket Expert Advice

If your score dropped suddenly, don’t panic.

Instead:

- Focus on utilization first

- Then check for errors

- Then stabilize your behavior

Most drops are reversible within 30–60 days.

12. Why MaintainMarket is Different

Most websites give generic advice like:

“Pay bills on time.”

That’s obvious.

What we do differently:

- Break down real triggers banks use

- Explain timing hacks (statement vs due date)

- Provide action-based solutions

This is practical finance — not theory.

13. Hidden Triggers Almost Nobody Talks About

This is where things get interesting.

Credit Limit Decrease (Bank Move)

Banks can reduce your limit anytime.

If your limit drops:

- Your utilization increases

- Score drops instantly

Authorized User Removal

If you were linked to someone else’s card:

- Their history was helping you

- Once removed → score drops

Loan Paid Off Effect

Closing a loan can:

- Reduce credit mix

- Reduce active accounts

Short-term dip is normal.

Reporting Timing Issue

Even if you paid:

If reporting happened before payment → high balance recorded.

Dormant Account Closure

Unused cards can get closed.

This reduces:

- Credit history

- Available limit

14. Score Drop Breakdown (Reality Check)

| Trigger | Expected Impact |

|---|---|

| High utilization | 40–100 points |

| Late payment | 60–120 points |

| Hard inquiries | 10–40 points |

| Account closure | 20–50 points |

| Credit error | 50–150 points |

16. Recovery Timeline

| Action | Time |

|---|---|

| Reduce utilization | 15–45 days |

| Fix errors | 7–30 days |

| Inquiry impact fades | 30–90 days |

| Late payment recovery | 3–6 months |

15. Advanced Strategy (Pro Level)

Pay Twice Monthly

Keeps utilization low consistently.

AZEO Method

All cards zero, one card small balance.

Rapid Rescore (USA)

Lenders can update score in 3–7 days with proof.

16. Psychological Mistake

People panic and apply for more credit.

That’s the worst move.

Correct approach:

- Stabilize

- Improve

- Then apply

17. Lender Risk Zones

| Score | Risk Level |

|---|---|

| 750+ | Very Low |

| 700–749 | Safe |

| 650–699 | Medium |

| 600–649 | Risky |

| <600 | High Risk |

18. Pre-Approval Killer Signals

Even with a good score, lenders check:

- Recent activity

- Balance spikes

- New accounts

These can block approvals.

19. Credit Score vs Approval Truth

Score alone is not enough.

Lenders also check:

- Income

- Debt ratio

- Behavior patterns

20. Smart Monitoring Strategy

Track:

- Utilization

- Account activity

- Inquiry count

Check weekly, not obsessively daily.

Most people think credit score drops are random. In reality, they are pattern-based reactions from lender risk models. Even small changes in balance reporting or credit usage timing can significantly impact your score. Understanding these patterns gives you a clear advantage in fixing and controlling your credit profile.

“If you want to stay ahead of sudden drops, using a reliable credit monitoring tool can help you detect changes early and fix them before they affect your approvals.”

Final Power Line

Your credit score didn’t drop randomly.

It reacted.

And once you understand that reaction…

You’re no longer confused — you’re in control.

FAQs:-

Q1. How many points can a FICO score drop suddenly?

Anywhere between 20 to 100+ points depending on the trigger.

Q2. Can my score drop even if I paid on time?

Yes, due to high utilization or new inquiries.

Q3. How long does it take to recover?

Usually 30–90 days if corrected quickly.

Q4. Do soft inquiries affect score?

No, only hard inquiries do.

Q5. Does checking my own score reduce it?

No, that’s a soft inquiry.

Q6. Can closing a credit card hurt my score?

Yes, it reduces available credit and history length.

Q7. What is ideal credit utilization?

Below 30%, ideally under 10%.

Q8. How often should I check my credit report?

At least once a month.

Q9. Why did my FICO score drop suddenly?

Usually due to utilization increase, new inquiries, account closure, or reporting changes.

Q10. Can my score drop even if I didn’t miss a payment?

Yes. Payment history is only one factor — utilization and behavior matter more short-term.

Q11. How many points can a score drop?

Anywhere from 20 to 100+ points depending on the trigger.

Q12. How fast can I recover my credit score?

Typically within 30–90 days if the issue is fixed quickly.

Q13. Does checking my own credit score hurt it?

No. That’s a soft inquiry.

Q14. What is the biggest reason for sudden drops?

High credit utilization is the most common cause.

Q15. Can errors in credit report reduce my score?

Yes, and they are more common than people think.

People searched for: 7 Best Credit Builder Apps in the USA That Can Boost Your Score Even If It’s Below 600

Also read: One Utilization Hack Can Boost Your Credit Score in 30 Days

How to Get a High Credit Limit Card in 2026 (Banks Are Quietly Changing Approval Rules)

3 thoughts on “7 Silent Reasons Destroying Your FICO Score Right Now – Fico score dropped without reason”