Learn how a home equity loan works, how much you can borrow, interest rates, risks, approval requirements, and smart ways homeowners use home equity in 2026. In this article, let’s talk about how does a home equity loan works.

A home equity loan allows homeowners to borrow money against the equity in their property. The loan is typically paid as a lump sum with fixed monthly payments and fixed interest rates. Your home acts as collateral, which helps lenders offer lower interest rates compared to credit cards or personal loans.

How Does a Home Equity Loan Work? The Truth Most Homeowners Learn Too Late

Introduction

A lot of homeowners think their house is just a place to live.

Banks think differently.

To lenders, your home is also a financial asset sitting on untapped cash.

That’s exactly why millions of Americans use home equity loans every year — not because they’re rich, but because they need money for something important:

- Paying off high-interest credit card debt

- Emergency medical expenses

- Home renovations

- College tuition

- Business funding

- Major life emergencies

But here’s the dangerous part most articles don’t explain clearly:

A home equity loan can either become one of the smartest financial moves you ever make… or a decision that traps you in debt for years.

And the reason depends entirely on whether you truly understand how it works.

This guide breaks everything down in simple language — no confusing banker jargon, no generic textbook explanations.

By the end, you’ll know:

- How a home equity loan actually works

- How banks calculate your borrowing power

- Interest rates and monthly payments

- Hidden risks most lenders avoid discussing

- When using home equity makes sense

- When it’s a terrible idea

Quick Answer Box

What Is a Home Equity Loan?

A home equity loan lets homeowners borrow money against the value they’ve built in their property.

It works like this:

- Your home acts as collateral

- The lender gives you a lump sum payment

- You repay it in fixed monthly installments

- Interest rates are usually lower than credit cards or personal loans

Example:

If your home is worth $500,000 and you still owe $300,000 on your mortgage, you may have around $200,000 in equity.

Many lenders allow you to borrow 80%–85% of your available equity.

What Is Home Equity in Simple Words?

Home equity is the portion of your house you actually own.

Formula:

Home Equity=Home Value−Mortgage Balance

Example:

| Home Value | Mortgage Left | Your Equity |

|---|---|---|

| $600,000 | $350,000 | $250,000 |

That $250,000 becomes potential borrowing power.

The more mortgage you pay off — and the more your property value rises — the more equity you build.

How Does a Home Equity Loan Work?

Think of it as a second mortgage.

You already have your original mortgage.

Now you borrow another loan against the same property.

Here’s the process:

Step 1: The Lender Checks Your Home Value

The bank determines your property’s current market value.

Usually through:

- Appraisal

- Automated valuation models

- Market comparisons

Step 2: They Calculate Your Equity

They subtract what you still owe from your home’s value.

Example:

| Item | Amount |

|---|---|

| Home Value | $700,000 |

| Remaining Mortgage | $400,000 |

| Available Equity | $300,000 |

Step 3: The Bank Decides How Much You Can Borrow

Most lenders won’t let you borrow 100% of your equity.

Typically they allow:

- 80%

- 85%

- Sometimes 90% combined loan-to-value (CLTV)

Example:

| Equity | Borrowing Limit (80%) |

|---|---|

| $300,000 | $240,000 |

Step 4: You Receive a Lump Sum

Unlike a HELOC (Home Equity Line of Credit), a home equity loan gives you money all at once.

That’s why people often use it for:

- Debt consolidation

- Renovation projects

- Large expenses

Step 5: Fixed Monthly Payments Begin

Most home equity loans have:

- Fixed interest rates

- Fixed repayment terms

- Predictable monthly payments

Common repayment periods:

- 5 years

- 10 years

- 15 years

- 20 years

Also read: Best Lenders for Low Credit Score USA (2026) | Fast Approval Options

Why So Many Americans Use Home Equity Loans

Because they’re usually cheaper than:

- Credit cards

- Personal loans

- Payday loans

Here’s why.

The lender has collateral.

Your house.

That lowers the bank’s risk.

Lower risk usually means lower interest rates.

Average Home Equity Loan Interest Rates (2026)

Rates vary based on:

- Credit score

- Debt-to-income ratio

- Home equity amount

- Income

- Market interest rates

Estimated Rate Breakdown

| Credit Score | Estimated Rate |

|---|---|

| 760+ | 6.5% – 7.2% |

| 700–759 | 7.3% – 8.5% |

| 640–699 | 8.6% – 10.5% |

| Below 640 | Difficult approval |

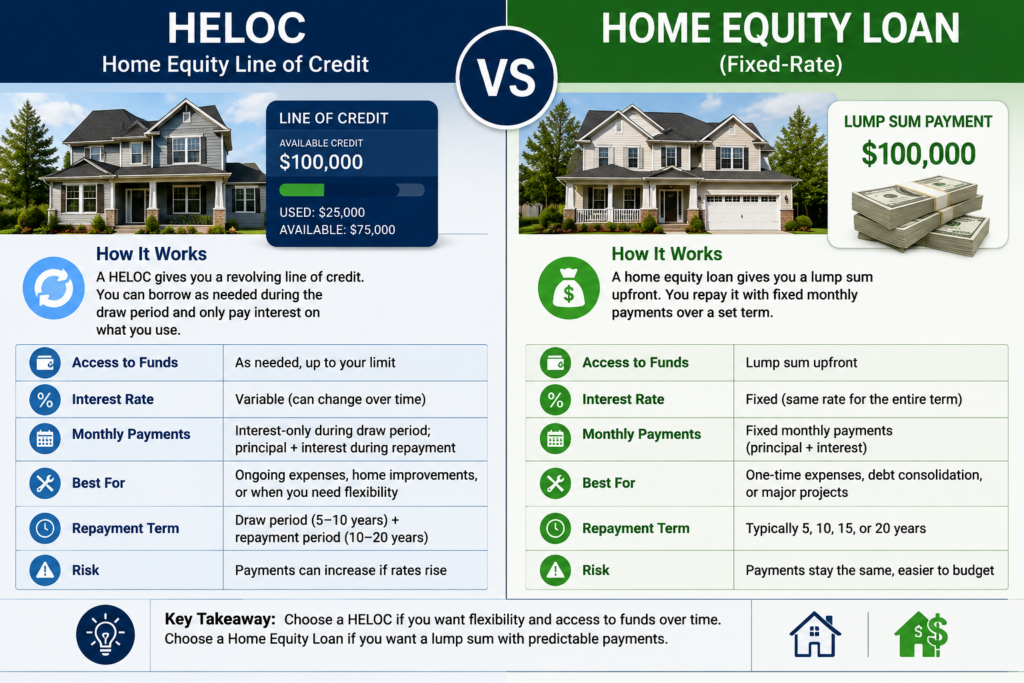

Home Equity Loan vs HELOC

Many homeowners confuse these two.

They are NOT the same.

| Feature | Home Equity Loan | HELOC |

|---|---|---|

| Money Received | Lump sum | Credit line |

| Interest Rate | Fixed | Variable |

| Monthly Payments | Predictable | Can change |

| Best For | One-time large expense | Ongoing expenses |

| Risk Level | More stable | Can become expensive |

If you hate unpredictable payments, fixed-rate home equity loans are usually safer.

Why Banks Love Home Equity Loans

Banks make serious money from these loans.

But they also like them because borrowers rarely walk away from debt tied to their home.

This is important to understand.

When you miss payments on a credit card, your credit score gets damaged.

When you miss payments on a home equity loan, you could lose your house.

That changes borrower behavior dramatically.

Insider Insight: How Lenders Actually Think

Most people believe loan approval is mainly about income.

Not true.

Lenders focus heavily on risk.

Here’s what they secretly analyze:

1. Stability

Banks prefer borrowers who:

- Stay at the same job longer

- Have consistent income

- Show stable banking activity

2. Debt-to-Income Ratio (DTI)

This matters massively.

Most lenders want DTI below 43%.

Formula:

DTI Ratio=Gross Monthly IncomeMonthly Debt Payments×100

If your debt is too high already, approval becomes difficult.

3. Credit Behavior

Banks study:

- Late payments

- Credit utilization

- Collections

- Hard inquiries

- Bankruptcy history

Even wealthy borrowers get denied if their financial behavior looks risky.

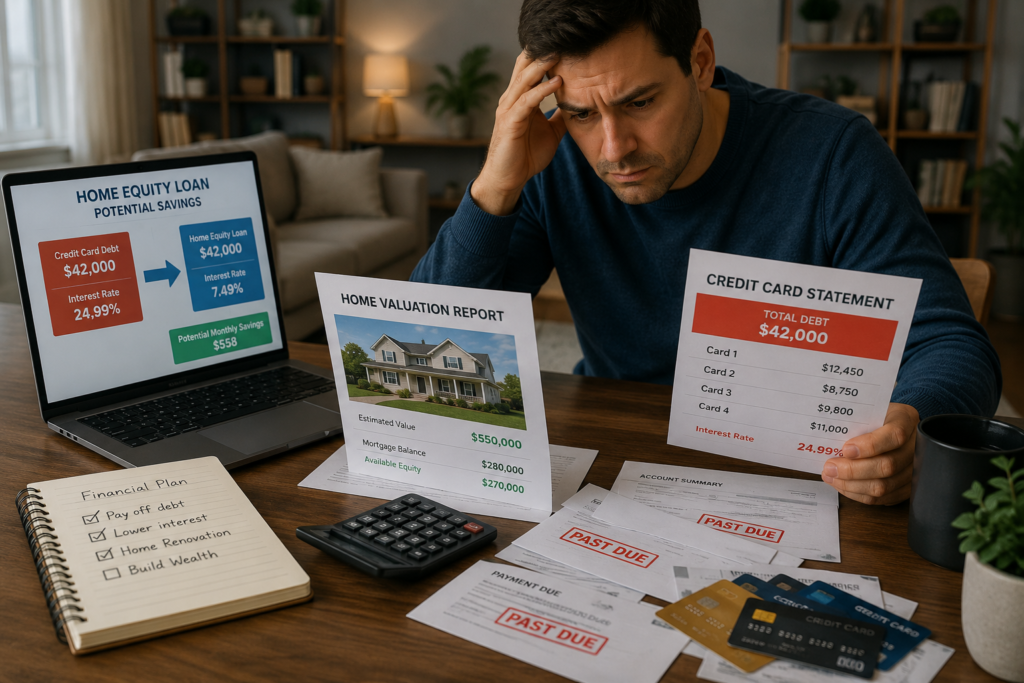

Real-Life Case Study

How One Texas Homeowner Used a Home Equity Loan to Escape Credit Card Debt

Mark, a homeowner in Texas, had:

- $42,000 in credit card debt

- Average interest rate: 24%

- Monthly minimum payments eating his paycheck

His house appreciated heavily during the housing boom.

Home value: $520,000

Mortgage balance: $310,000

Available equity: $210,000

He took a $50,000 home equity loan at 7.4%.

Result:

| Before | After |

|---|---|

| Credit Card APR: 24% | Home Equity Loan: 7.4% |

| Multiple payments | One fixed payment |

| High interest trap | Faster debt payoff |

His monthly financial pressure dropped significantly.

But here’s the important part:

He also stopped using credit cards recklessly.

Otherwise, many people end up with BOTH:

- Home equity debt

- New credit card debt

That’s how financial disasters begin.

Also read: How to Refinance Student Loans in 2026 | Lower Monthly Payments Fast

When a Home Equity Loan Is a Smart Idea

Good Reasons

Home Renovations

Especially improvements that increase property value:

- Kitchen remodeling

- Roof replacement

- Solar installation

Debt Consolidation

If you’re replacing:

- 20%+ credit card debt

- High-interest loans

with lower-rate home equity borrowing.

Emergency Medical Expenses

Lower rates can help reduce financial damage.

Business Investment

Only if:

- Cash flow is predictable

- Risk is controlled

Using home equity for risky startups is dangerous.

When It’s a Bad Idea

Vacations

Never risk your house for temporary lifestyle spending.

Luxury Purchases

Cars depreciate.

Your house should not be collateral for depreciating assets.

Gambling on Investments

Some people borrow against home equity to buy stocks or crypto.

That can destroy families financially during market crashes.

Hidden Risks Most Articles Ignore

1. Foreclosure Risk

Miss payments long enough…

The lender can legally take your home.

That’s the biggest risk.

2. Falling Home Prices

If housing prices crash, you could owe more than your home is worth.

3. Fees and Closing Costs

Many borrowers forget about:

- Appraisal fees

- Origination fees

- Closing costs

- Annual fees

These can total thousands.

4. Long-Term Debt Trap

A 15-year loan may lower monthly payments…

But increase total interest paid dramatically.

Comparison Table: Home Equity Loan vs Other Borrowing Options

| Loan Type | Average Rate | Collateral Required | Risk Level |

|—|—|—|

| Home Equity Loan | Lower | Yes (House) | High |

| Personal Loan | Medium | No | Medium |

| Credit Card | Very High | No | High Interest |

| HELOC | Variable | Yes | Moderate |

| Cash-Out Refinance | Lower | Yes | High |

Biggest Mistakes Homeowners Make

Borrowing Too Much

Just because the bank approves a huge amount doesn’t mean you should take it.

Ignoring Variable Debt Elsewhere

People consolidate debt…

Then start spending again.

That creates double debt.

Not Shopping Around

Rates vary heavily between lenders.

Even a 1% difference can cost thousands over time.

Using Home Equity Emotionally

Some borrowers treat equity like “free money.”

It’s not.

It’s tied directly to your home ownership.

MaintainMarket Expert Advice

At MaintainMarket, we believe home equity loans should solve problems — not create new ones.

The smartest borrowers usually follow three rules:

- Borrow only for assets or financial improvement

- Keep payments manageable even during emergencies

- Never use home equity to support unstable spending habits

The biggest red flag?

Using home equity because income problems are becoming permanent.

That often signals a deeper financial issue that borrowing alone cannot fix.

Why MaintainMarket Is Different

Most finance websites only explain definitions.

They rarely explain:

- Real borrower psychology

- Lender risk analysis

- Approval behavior

- Financial traps

- Long-term consequences

MaintainMarket focuses on real-world financial survival and smart decision-making — not just textbook explanations.

That’s why our guides are written to help readers actually make better money decisions, not simply generate pageviews.

Action Plan: What You Should Do Before Applying

Step 1

Check your current home value.

Step 2

Know exactly how much equity you have.

Step 3

Calculate your monthly affordability honestly.

Not based on optimism.

Based on worst-case scenarios too.

Step 4

Improve your credit score before applying.

Even a small improvement can lower rates significantly.

Step 5

Compare at least 4–5 lenders.

Never accept the first offer blindly.

Conclusion

A home equity loan can be either:

- A financial reset button

- Or the beginning of a major debt problem

The difference usually comes down to one thing:

Why you’re borrowing.

Using home equity strategically for debt reduction, renovations, or real financial improvement can make sense.

Using it emotionally or carelessly can put your entire home at risk.

Before signing anything, remember:

You are not borrowing “extra money.”

You are borrowing against the roof over your head.

That changes everything.

FAQs

Q1. Is a home equity loan a second mortgage?

Yes. A home equity loan is commonly considered a second mortgage because it’s separate from your original mortgage.

Q2. How much can I borrow with a home equity loan?

Most lenders allow borrowing up to 80%–85% of your home equity.

Q3. Do home equity loans have fixed rates?

Usually yes. Most traditional home equity loans come with fixed interest rates.

Q4. Usually yes. Most traditional home equity loans come with fixed interest rates.

Many lenders prefer 680+, but stronger rates usually require 720+.

Q5. Can I lose my home?

Yes. Defaulting on payments could eventually lead to foreclosure.

Q6. Is a HELOC better than a home equity loan?

Depends on your situation. HELOCs offer flexibility, while home equity loans offer payment stability.

Q7. Are home equity loan interest rates lower than credit cards?

Usually yes, often significantly lower.

Q8. How long does approval take?

Typically between 2–6 weeks depending on the lender and documentation.

People searched for: Loan Rejected? Get Emergency Cash with Bad Credit in USA (2026 Proven Hacks)

Also read: 10 Best Debt Consolidation Loans for Poor Credit in the USA (2026) – Easy Approval Options

1 thought on “How Does a Home Equity Loan Work? Complete Beginner’s Guide (2026) – USA”