Student loans can either help or damage your credit score, depending on how you manage them. Learn the exact reasons scores drop and how to fix them fast. Let’s talk about Do Student Loans Affect Credit Score.

Introduction

Most people think student loans only become a problem when payments are missed.

That’s not true.

In reality, student loans can affect your credit score even when you’re doing everything “normally.” Some borrowers see their score drop after taking a loan. Others notice a sudden decrease after refinancing or even after fully paying off their student debt.

And honestly, this confuses almost everyone.

One day your credit score is healthy. Then suddenly it drops 40–80 points, and you have no idea why.

The worst part?

Banks do not explain this clearly. Credit bureaus don’t either.

For millions of Americans, student loans quietly become the reason:

- Credit card approvals get denied

- Car loan interest rates increase

- Mortgage approvals become harder

- Insurance premiums rise

- Credit utilization pressure increases

The good news is this problem is usually fixable.

But only if you understand how lenders actually look at student debt.

This guide explains the real relationship between student loans and credit scores — not the generic textbook version. You’ll learn:

- Why student loans can both help and hurt your score

- What causes sudden score drops

- How lenders secretly evaluate student debt

- What actions improve your score fastest

- Real strategies that actually work in 2026

Quick Answer Box

Do Student Loans Affect Credit Score?

Yes, student loans absolutely affect your credit score.

They can either improve or damage your score depending on:

- Payment history

- Loan age

- Credit mix

- Total debt amount

- Loan status

- Missed or late payments

Making on-time payments can help build strong credit over time. But missed payments, defaults, high balances, or refinancing mistakes can lower your score significantly.

For most borrowers, payment history is the biggest factor.

Why This Problem Happens

Student Loans Are Treated Like “Long-Term Trust”

Credit bureaus view student loans differently from credit cards.

A credit card measures short-term borrowing behavior.

Student loans measure long-term financial responsibility.

That means lenders pay close attention to:

- Whether you consistently pay over years

- How much debt you still owe

- Whether you panic refinance

- Whether your loans entered deferment or default

This is why student loans influence major financial decisions later in life.

How Student Loans Affect Your Credit Score

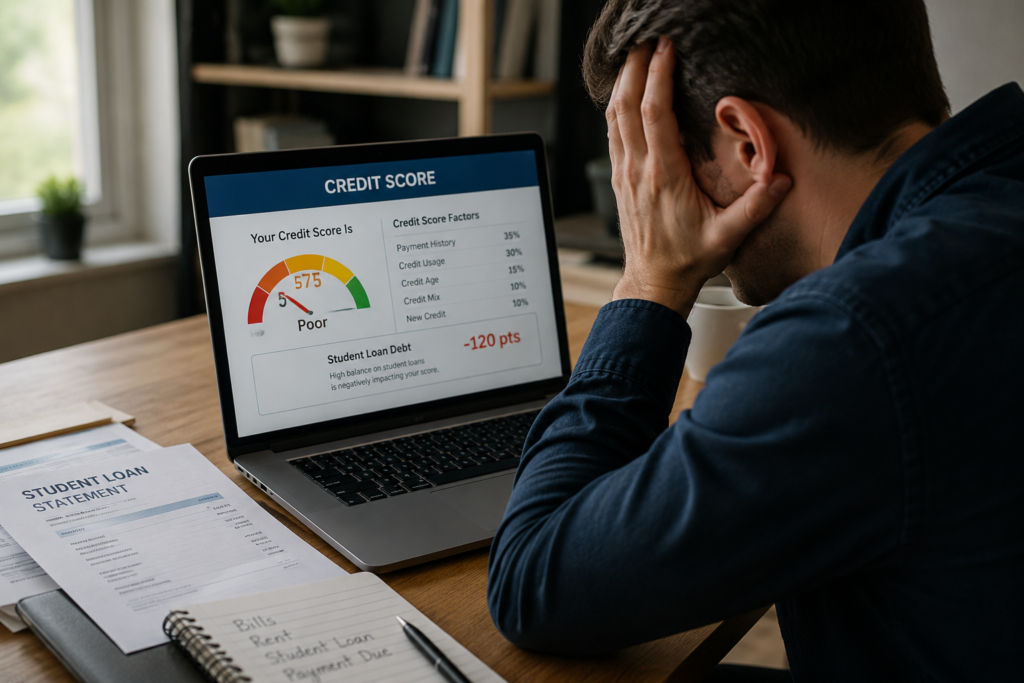

1. Payment History (Most Important)

Payment history makes up the largest portion of your FICO score.

If you miss even one student loan payment by 30+ days:

- Your score can drop sharply

- Negative marks may stay for 7 years

- Future lenders may consider you risky

A single missed payment can hurt more than people expect.

Especially for younger borrowers with shorter credit histories.

2. Credit Age

Student loans often stay open for many years.

This helps your average account age, which improves credit stability.

Ironically, some people see their score DROP after paying off student loans because:

- Their oldest account closes

- Average credit age decreases

This feels unfair, but it’s extremely common.

3. Credit Mix

Lenders like seeing different types of credit:

- Credit cards

- Installment loans

- Auto loans

- Mortgages

- Student loans

Student loans improve your “credit mix,” which slightly helps scores over time.

4. Debt-to-Income Pressure

Even if your credit score looks decent, lenders still analyze your debt burden.

This is where many borrowers struggle.

You may have:

- 720 credit score

- Perfect payment history

- Stable income

But if your student debt is too high, lenders may still reject applications.

Especially mortgages.

Banks care about risk exposure, not just your score.

5. Default and Collections

This is where real damage happens.

Federal or private student loan defaults can:

- Crush your credit score

- Trigger collections

- Lead to wage garnishment

- Stay on reports for years

Recovery becomes much harder after default.

Signs Your Student Loans Are Hurting Your Credit

Here are warning signs many borrowers ignore:

| Warning Sign | What It Usually Means |

|---|---|

| Credit score suddenly dropped | Late payment or utilization issue |

| Loan balance barely decreasing | Interest-heavy repayment |

| Mortgage denied | Debt-to-income problem |

| Credit card limit reduced | Lender risk reassessment |

| Refinancing lowered score | Hard inquiry + account changes |

| Multiple missed payments | High-risk borrower status |

Step-by-Step Solution to Protect and Improve Your Credit Score

Step 1: Check Your Loan Status Immediately

Many borrowers assume everything is fine.

Then they discover:

- A servicer error

- Missed autopay setup

- Deferred loan reporting issue

- Incorrect late payment

Start by checking:

- Payment history

- Loan balances

- Account status

- Reporting errors

Use:

- AnnualCreditReport

- Loan servicer dashboard

- FICO monitoring tools

Step 2: Never Miss a Payment Again

This matters more than almost anything else.

Set:

- Autopay

- Calendar reminders

- Backup payment methods

Even one missed payment can cost years of progress.

Step 3: Lower Your Overall Debt Pressure

Your score improves faster when lenders see lower financial stress.

Ways to reduce pressure:

- Pay down credit cards first

- Avoid unnecessary personal loans

- Refinance only if rates improve meaningfully

- Increase income temporarily through side work

This is why some borrowers with student debt still maintain 760+ scores.

Step 4: Use Income-Driven Repayment If Necessary

Many people avoid this because they think it “looks bad.”

It usually doesn’t.

If an income-driven plan helps you avoid missed payments, it is often the smarter move.

A smaller payment is better than damaged credit.

Step 5: Avoid Dangerous Refinancing Decisions

Refinancing sounds attractive because of lower interest rates.

But borrowers often ignore the hidden risks:

- Hard credit inquiry

- Shorter credit age

- Federal benefit loss

- Temporary score drops

Refinance only when:

- Income is stable

- Score is already strong

- New rate creates meaningful savings

Insider Insights: How Banks Actually Think

Here’s something most finance articles never explain.

Banks do not just care about whether you pay.

They care about whether your debt controls your future income.

A borrower earning $80,000 with:

- $15,000 student debt

looks safer than someone earning: - $80,000 with $150,000 debt

Even with identical credit scores.

Why?

Because lenders predict future stress.

Heavy student debt statistically increases:

- Default risk

- Credit card dependency

- Delayed mortgage payments

- Financial instability

That’s why lowering debt perception matters almost as much as improving your score.

Also read: How Does a Home Equity Loan Work? Complete Beginner’s Guide (2026)

Real-Life Case Study

How Emily’s Credit Score Fell 72 Points After Refinancing

Emily, a 29-year-old marketing executive in Texas, had:

- 748 credit score

- $62,000 federal student debt

- Perfect payment history

She refinanced her loans hoping to reduce monthly payments.

Within 45 days:

- Her score dropped to 676

Why?

Three things happened:

- Hard inquiry hit her report

- Old accounts closed

- New account age reset

She panicked.

But after:

- 8 months of on-time payments

- Lower credit utilization

- No new inquiries

Her score recovered to 735.

The key lesson:

Temporary score drops are common after refinancing.

Panic decisions make things worse.

Comparison Table: Which Strategy Helps Most?

| Strategy | Credit Score Impact | Risk Level | Best For |

|---|---|---|---|

| On-time payments | Very Positive | Low | Everyone |

| Autopay setup | Positive | Very Low | Busy borrowers |

| Refinancing | Mixed | Medium | Strong-credit borrowers |

| Income-driven repayment | Neutral/Positive | Low | Income pressure |

| Loan default | Extremely Negative | Very High | Avoid completely |

| Paying off oldest loan early | Sometimes negative short-term | Low | Long-term debt freedom |

Mistakes People Make

1. Ignoring Small Late Payments

Even a 30-day delay matters.

Many borrowers think:

“I’ll fix it next month.”

But the damage may already be reported.

2. Closing Old Credit Accounts

People aggressively close old accounts after paying debt.

This can reduce credit age and hurt scores.

3. Refinancing Too Early

Borrowers refinance while:

- Income is unstable

- Credit score is weak

- Job situation is uncertain

This creates unnecessary risk.

4. Only Focusing on Credit Score

Your score matters.

But lenders also evaluate:

- Debt-to-income ratio

- Employment stability

- Cash flow

- Financial behavior

A high score alone doesn’t guarantee approval.

Also read: How to Refinance Student Loans in 2026 | Lower Monthly Payments Fast

MaintainMarket Expert Advice

At MaintainMarket, we’ve noticed something interesting.

Most borrowers trying to “fix” their credit focus on complicated tricks:

- Credit hacks

- Disputes

- Random apps

- Quick-fix videos

But the borrowers who improve fastest usually do three simple things consistently:

- Never miss payments

- Lower revolving debt

- Stop applying for unnecessary credit

Credit repair is usually behavioral, not magical.

And honestly, patience matters more than shortcuts.

Why MaintainMarket Is Different

Most finance websites repeat generic advice copied from everywhere else.

MaintainMarket focuses on:

- Real financial behavior

- Lender psychology

- Actual approval patterns

- Practical solutions normal people can use

We don’t just explain what a credit score is.

We explain:

- Why lenders react the way they do

- What borrowers do wrong

- What actually changes approval odds

That difference matters.

Especially when your financial future depends on it.

Action Plan: What You Should Do Today

If your student loans are affecting your credit score, do this immediately:

Today

- Check all loan accounts

- Verify payment history

- Set autopay

- Review credit report

This Week

- Reduce credit card balances

- Avoid unnecessary applications

- Create repayment strategy

This Month

- Build emergency savings

- Track score changes

- Review refinancing carefully

Next 6 Months

- Maintain perfect payment history

- Lower overall debt pressure

- Improve financial consistency

This is how long-term credit improvement actually happens.

Conclusion

Student loans are not automatically bad for your credit score.

In fact, they can help build strong credit over time.

But when mismanaged — even slightly — they can quietly damage your financial future for years.

The biggest mistake borrowers make is reacting emotionally:

- Panic refinancing

- Ignoring payments

- Applying for too much credit

- Chasing quick fixes

Strong credit is built through consistency.

And the sooner you understand how lenders think, the easier it becomes to protect your score, qualify for better rates, and regain financial control.

FAQs

Q1. Do student loans lower your credit score immediately?

Sometimes. A new loan can temporarily lower your score because of hard inquiries and increased debt exposure.

Q2. Does paying student loans improve credit?

Yes. Consistent on-time payments usually improve credit over time.

Q3. Why did my score drop after paying off student loans?

Closing an old account can reduce your average credit age, causing a temporary drop.

Q4. Can student loans stop me from buying a house?

Yes. High student debt can increase your debt-to-income ratio and affect mortgage approval.

Q5. Is refinancing student loans bad for credit?

Not always. But refinancing may temporarily lower your score due to inquiries and account changes.

Q6. How long do student loans stay on credit reports?

Most student loans remain on reports until fully paid. Negative marks may stay for 7 years.

Q7. What hurts credit more: credit cards or student loans?

Missed credit card payments usually hurt faster, but student loan defaults can create severe long-term damage.

Q8. Can I rebuild my credit after student loan default?

Yes, but recovery takes time. Consistent payments, rehabilitation programs, and debt management help rebuild scores gradually.

People searched for: Best Lenders for Low Credit Score USA (2026) | Fast Approval Options

Also read: Secured vs Unsecured Credit Card USA (2026): Which One Builds Credit Faster?