Learn the real difference between soft pull vs hard pull credit checks and how they impact your loan approval. Avoid rejections and fix your credit fast. In this article, let’s talk about Soft Pull vs Hard Pull loan approval: The Hidden Reason Your Loan Gets Rejected.

Introduction

You applied for a loan thinking everything was fine.

Your credit score looked decent. Income stable. No major defaults.

Then suddenly — rejected.

No clear reason.

What most people don’t realize is this:

👉 The type of credit check (soft pull vs hard pull) can silently affect your approval chances — even before you understand what happened.

And yes, this happens in both the USA (FICO system) and India (CIBIL system).

This guide will break it down in the simplest way possible — no jargon, no confusion — just what actually matters when you apply for a loan.

Quick Answer Box (Featured Snippet)

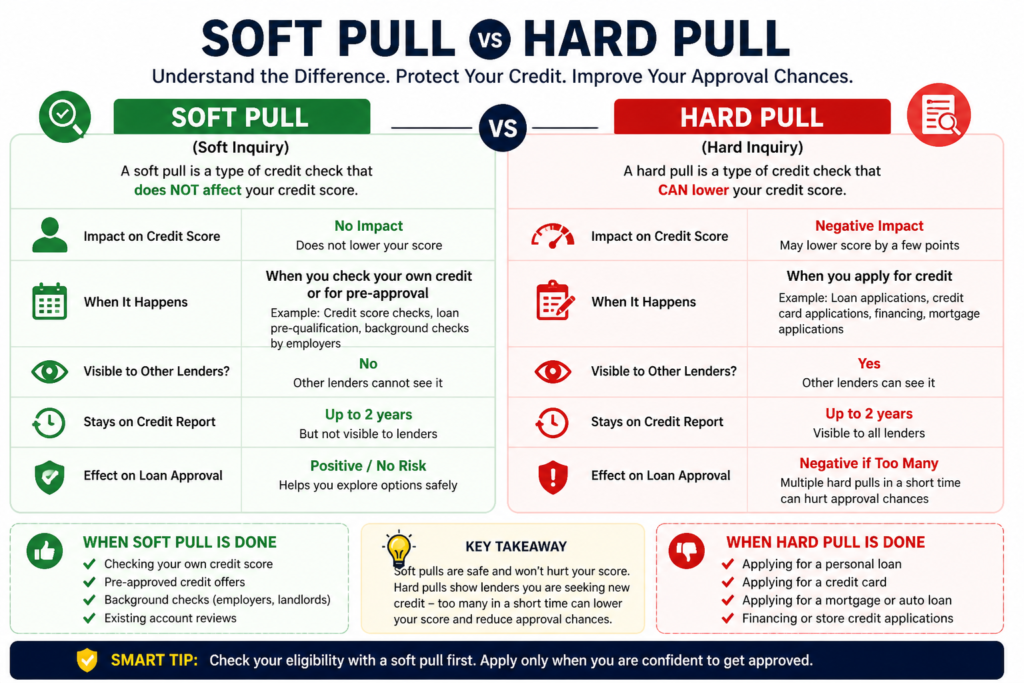

Soft Pull vs Hard Pull (Simple Difference):

| Type | Impact on Score | When It Happens | Visible to Lenders |

|---|---|---|---|

| Soft Pull | No impact | Pre-check, eligibility | No |

| Hard Pull | Lowers score (temporary) | Final loan/credit application | Yes |

👉 Too many hard pulls = higher rejection risk.

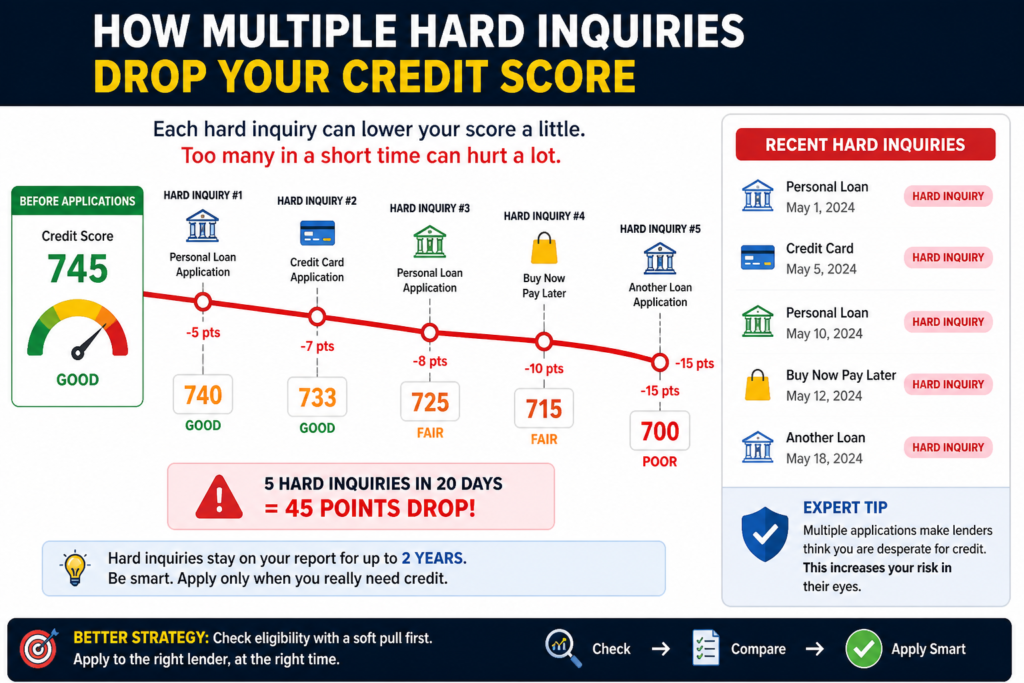

Why This Problem Happens (Real Truth)

Here’s where most articles lie to you.

They say:

“Hard inquiry only reduces 5–10 points”

That’s incomplete.

Reality:

- One hard pull = small drop

- Multiple hard pulls in short time = red flag

Lenders think:

👉 “This person is desperate for credit”

And that triggers:

- Rejection

- Lower limits

- Higher interest rates

USA Example:

Under FICO Score

- 3–5 inquiries in 30 days = risk signal

India Example:

Under CIBIL Score

- Multiple loan checks = “credit hungry behavior”

Soft Pull vs Hard Pull (Deep Explanation)

Soft Pull (Safe Zone)

This happens when:

- You check your own score

- Pre-approved offers

- Some apps verify eligibility

No impact.

Think of it like:

👉 “Window shopping”

Hard Pull (Risk Zone)

This happens when:

- You apply for a loan

- Credit card application

- Final lender verification

Impact:

- Score drops slightly

- Visible to all lenders

Think of it like:

👉 “Final purchase attempt”

Step-by-Step: How to Avoid Loan Rejection

Step 1: Always Start With Soft Pull

Use:

- Pre-approval tools

- Eligibility checkers

Never directly apply blindly.

Step 2: Limit Hard Inquiries

Golden Rule:

👉 Max 2–3 applications in 30 days

More than that = risk.

Step 3: Time Your Applications

Bad move:

Applying to 5 lenders in 1 week

Smart move:

- Wait 30–45 days between applications

Step 4: Improve Score Before Hard Pull

Before applying:

- Reduce credit utilization (<30%)

- Pay dues

- Avoid late payments

Hidden Impact: Hard Pulls Don’t Work Alone (They Combine With Other Factors)

Most people think:

👉 “Hard inquiry = small issue”

Wrong.

Hard pulls become dangerous when combined with:

- High credit utilization (above 50%)

- Recent late payments

- Thin credit history

- New accounts opened recently

Real Insight:

A single hard pull + high utilization = double negative signal

In systems like FICO Score and CIBIL Score:

👉 Risk is calculated using patterns, not isolated actions.

Loan Shopping vs Credit Hungry Behavior (VERY IMPORTANT)

This is where most people lose approvals.

Good Behavior (Loan Shopping):

- Applying for same loan type (auto loan, home loan)

- Within 14–45 days window (USA)

👉 Counted as ONE inquiry in many cases

Bad Behavior (Credit Hungry):

- Applying for:

- Personal loan

- Credit card

- Buy Now Pay Later

- Multiple apps

👉 Seen as desperation

USA vs India Difference (Underrated SEO Angle)

| Factor | USA (FICO) | India (CIBIL) |

|---|---|---|

| Inquiry Grouping | Yes (rate shopping) | Limited |

| Score Sensitivity | Medium | High |

| Loan Approval Logic | Data-driven | Conservative |

| Multiple Inquiries Impact | Slightly flexible | Strict |

👉 In India, even 2–3 hard pulls can hurt faster

Pre-Approval vs Pre-Qualified (Confusing But Important)

People mix these up.

Pre-Qualified:

- Based on soft pull

- Less accurate

- Marketing-driven

Pre-Approved:

- Stronger validation

- Higher approval chance

- Still may convert to hard pull later

👉 Always prefer pre-approved offers

Advanced Strategy: How Smart Borrowers Use Soft Pulls

Instead of applying randomly:

- Check eligibility on 3–4 platforms (soft pull)

- Compare:

- Interest rate

- Approval chance

- Apply only to BEST option

👉 This reduces risk by 70%+

Timing Strategy (Highly Ignored)

Best time to apply for loan:

- After salary credit cycle

- After clearing dues

- When credit utilization is low

Worst time:

- After missed payment

- After recent loan closure (temporary score fluctuation)

- After multiple inquiries

Psychological Trigger (How Banks Judge You)

Banks don’t say this openly:

But internally they think:

- “Is this person stable?”

- “Are they desperate?”

- “Will they default?”

Hard pulls = behavioral stress signal

👉 That’s why timing matters more than score sometimes.

Real Case Study (India)

Rahul (Bangalore):

- CIBIL Score: 735

- Applied to 3 apps + 2 banks in 7 days

- Score dropped to 708

- Loan rejected

Fix:

- Waited 40 days

- Used pre-approved offer

- Got approval with lower interest

Comparison Table (User Decision Level)

| Situation | Best Action | Why |

|---|---|---|

| First-time borrower | Soft pull only | Build safe profile |

| Low score (<650) | Improve before applying | Avoid rejection |

| Urgent need | Apply to 1 lender only | Minimize damage |

| Already rejected | Wait 30–60 days | Reset behavior signal |

What Happens After a Hard Pull (Behind the Scenes)

When a lender does a hard pull:

- Your report is accessed

- Inquiry is recorded

- Risk model updates instantly

- Other lenders see this activity

👉 This is why multiple applications backfire fast

Recovery Strategy (If You Already Made Mistake)

If you’ve already done multiple hard pulls:

Do this immediately:

- Stop all applications

- Wait minimum 30 days

- Reduce utilization below 30%

- Pay all dues on time

- Apply via pre-approved lender only

👉 Recovery timeline: 30–90 days

Insider Insight (How Lenders Actually Think)

Banks don’t just see your score.

They analyze behavior:

- “Why is this person applying everywhere?”

- “Is there hidden financial stress?”

- “Will they default?”

Hard inquiries = behavior signal

👉 Not just numbers.

Real-Life Case Study (USA)

John (Texas):

- Score: 710

- Applied to 4 lenders in 10 days

- Score dropped to 685

- Loan rejected

What went wrong?

👉 Too many hard pulls.

What fixed it?

- Waited 45 days

- Applied via pre-approved lender

- Got approved

Comparison Table (Best Strategy)

| Strategy | Approval Chance | Risk Level | Best For |

|---|---|---|---|

| Direct Hard Apply | Medium | High | Experienced users |

| Soft Pull First | High | Low | Beginners |

| Multiple Applications | Low | Very High | Avoid |

| Pre-Approved Offer | Very High | Low | Smart users |

Mistakes People Make

- Applying to multiple lenders same day

- Ignoring inquiry count

- Not using pre-approval tools

- Panic applying after rejection

- Believing “more attempts = higher chance”

That last one kills approvals.

MaintainMarket Expert Advice

If you remember only one thing, remember this:

👉 Your behavior matters more than your score

A 680 score with smart behavior can get approved.

A 720 score with panic applications can get rejected.

Why MaintainMarket is Different

Most websites explain definitions.

We focus on:

- Real-world approval strategy

- Lender psychology

- Action-based solutions

Because knowing is useless if you still get rejected.

Action Plan (Do This Now)

- Check your credit (soft pull only)

- Stop applying everywhere

- Wait at least 30 days if already applied

- Use pre-approved offers

- Apply only when confident

Conclusion

Soft pull vs hard pull is not just a technical difference.

It’s the difference between:

👉 Getting approved

👉 Getting silently rejected

If you understand this early, you avoid one of the biggest mistakes beginners make.

FAQs – Soft Pull vs Hard Pull Loan Approval

Q1. Does soft pull affect credit score?

No, it has zero impact.

Q2. How many hard inquiries are too many?

More than 3 in a short period is risky.

Q3. Can I remove hard inquiries?

Only if incorrect.

Q4. How long do hard inquiries stay?

Up to 2 years (USA & India).

Q5. Do all lenders do hard pulls?

Most do before final approval.

Q6. What is better: pre-approval or direct apply?

Pre-approval (soft pull) is safer.

Q7. Why was my loan rejected after good score?

Likely due to multiple inquiries or risk signals.

Q8. How to recover from too many inquiries?

Wait 30–60 days and avoid new applications.

People searched for: How to Recover 100 Point Credit Score Drop Fast – Hacks Banks Won’t Tell You

Also read: Get ₹20,000 Loan Instantly – No CIBIL Score Required (Real Options) – 2026 Guide

15 Best Side Hustles From Home USA (Earn $1000+/Month) – Real Guide 2026

2 thoughts on “Soft Pull vs Hard Pull Loan Approval: The Hidden Reason Your Loan Gets Rejected (Fix It Before It’s Too Late)”