Paid off your loan, but your FICO score dropped? Learn the real reasons behind this and how to recover your credit score fast with proven strategies. In this article, let’s talk about why FICO Score Dropped After Paying Off Loan.

“If your profile has become thin after loan payoff, using a trusted credit builder tool can help restore activity faster.”

Introduction

You did everything right.

You paid off your loan. No missed payments. No defaults. You expected your credit score to go up… but instead, it dropped.

That moment feels confusing and honestly a bit unfair.

A lot of people think something is wrong with their credit report when this happens. But the truth is — this is actually a very common situation, especially in the US credit system.

And here’s the part most articles won’t tell you:

Your score didn’t drop because you did something wrong. It dropped because the system recalculated your profile differently.

Let’s break this down properly so you can fix it — fast.

Quick Answer (Featured Snippet Box)

Your FICO score may drop after paying off a loan because:

- Your credit mix changes (fewer types of credit)

- Your average account age decreases

- The active positive payment history stops

- Your credit profile becomes “thinner”

This drop is usually temporary and can be fixed within 30–90 days with the right actions.

Why This Happens (Real Reasons, Not Textbook)

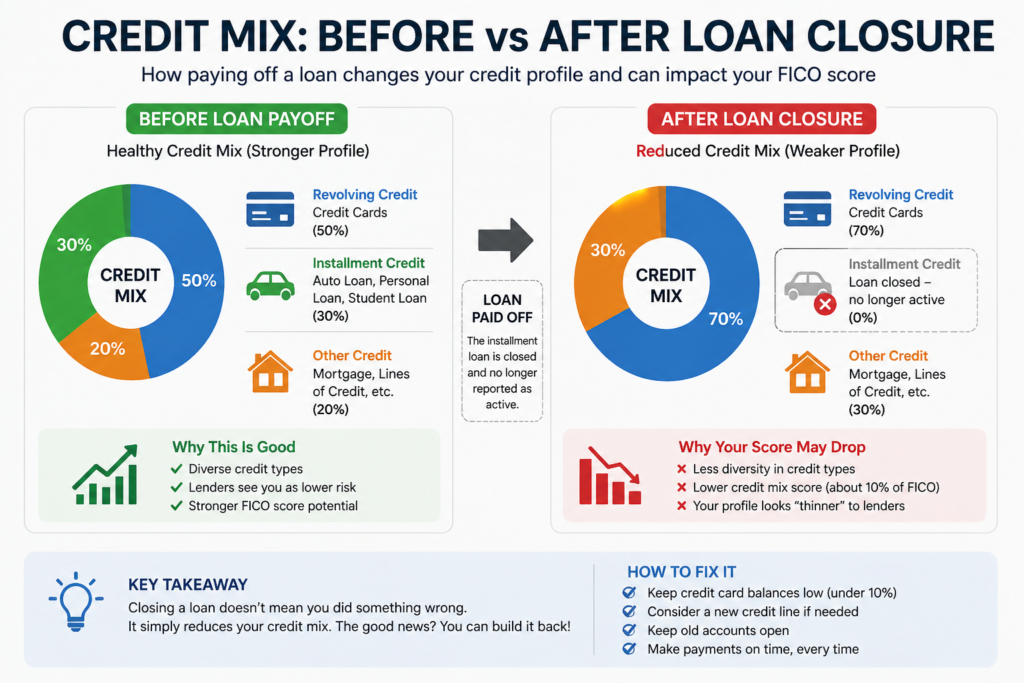

1. You Lost a Credit Type (Credit Mix Impact)

FICO loves diversity.

If your loan was an installment loan (personal loan, auto loan) and you paid it off, now your profile might only have credit cards.

That reduces your “credit mix” — which is around 10% of your score.

So the system thinks:

“This person now handles fewer types of credit.”

And your score dips.

2. Your Average Account Age Changed

This is the part most people don’t understand.

Even though the account stays on your report, once it’s closed:

- It stops aging actively

- Your overall average age can shift

If that loan was one of your older accounts, your credit history suddenly looks shorter.

Shorter history = slightly higher risk (in lender eyes)

3. You Lost Active Positive Activity

Before:

- You were making monthly payments → showing responsibility

Now:

- That activity is gone

Credit scoring models reward ongoing behavior, not just past success.

4. Your Profile Became “Less Active”

This is subtle but important.

Let’s say:

- You had 1 loan + 1 credit card

After payoff:

- You now only have 1 active account

To lenders, that looks like:

“We have less data to evaluate this person.”

Less data = slightly more risk = score drop

5. Installment Loan Closure Changes Your Risk Profile

Here’s something most people miss:

When you had a loan:

- You were managing fixed monthly obligations

- That signals discipline to lenders

After payoff:

- That obligation disappears

- Your profile looks “less tested”

So even though you’re financially stronger,

your credit profile becomes less predictable

6. Your “Credit Mix Weight” Was Carrying More Than You Think

Credit mix is officially ~10%, but in reality:

If your profile is thin (few accounts),

that 10% can behave like 20–25% influence

Example:

- 1 credit card + 1 loan → balanced

- After payoff → only 1 card → weak profile

That’s why some people see a bigger drop than expected.

7. Your Score Was Boosted by “Active Installment History”

While your loan was open:

- Every EMI/payment was adding positive signals monthly

Once closed:

- That “ongoing boost” disappears

It’s like:

You stopped feeding the system fresh data

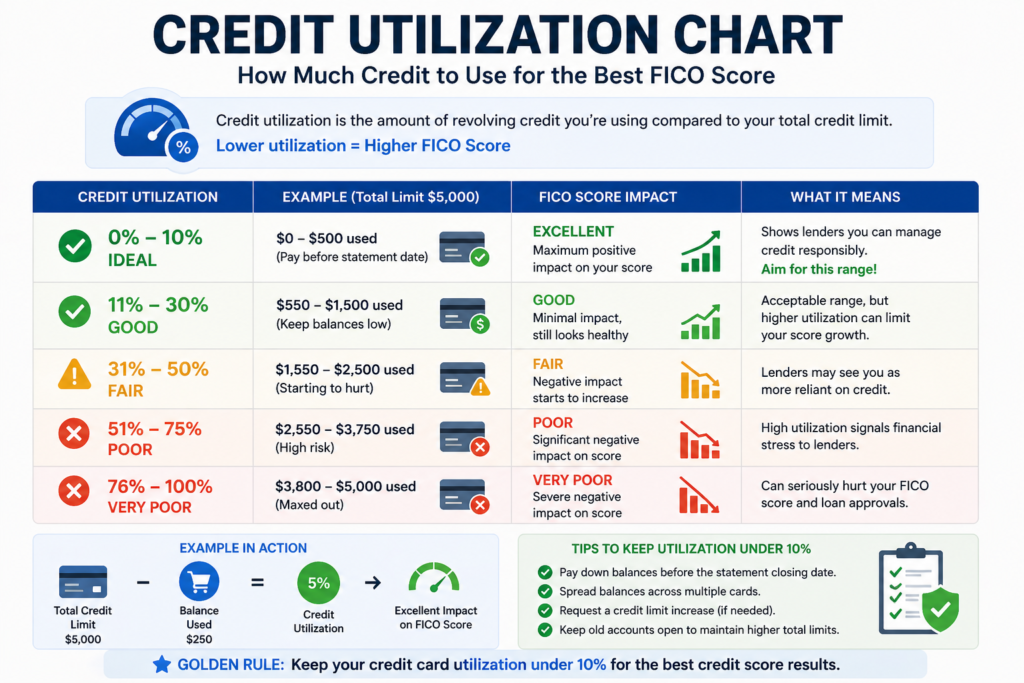

8. Credit Utilization Suddenly Becomes More Important

After loan closure:

FICO shifts more weight to:

- Credit card usage

- Payment behavior

So if your utilization is:

- 30–50% → score drops further

- Under 10% → score recovers faster

ADVANCED FIX STRATEGIES (REAL EDGE)

Strategy 1: The 10% Utilization Hack (Most Powerful)

Don’t just “keep low utilization”

Do this instead:

- Spend normally

- Pay down before statement date

- Report only 5–10% usage

This creates an illusion of:

“Active but highly controlled borrower”

Strategy 2: The “Two Card Optimization Method”

If you have only 1 card:

→ Your profile is weak

Fix:

- Keep 2–3 credit cards

- Use only 1 actively

- Keep others at 0 balance

This improves:

- Credit mix perception

- Risk diversification

Strategy 3: Add a Small Installment Loan (If Needed)

If your score dropped heavily (30+ points):

You can:

- Take a small credit-builder loan ($500–$1000)

Why it works:

- Restores installment mix

- Adds fresh activity

- Improves scoring model balance

Step-by-Step: How to Fix It Fast

Step 1: Keep Your Credit Card Utilization Low

This is your biggest weapon now.

- Keep usage under 30% (ideally 10%)

- Pay before statement date

Example:

Limit: $1000

Usage: Keep under $100–$300

Step 2: Don’t Close Old Credit Cards

Big mistake people make:

They pay off loan → feel debt-free → close cards

That destroys:

- Credit history length

- Available credit

Keep old accounts open.

Step 3: Add a New Credit Line (If Needed)

If your profile became thin:

- Consider a secured credit card

- Or a small credit-builder loan

This restores:

- Activity

- Credit mix

Step 4: Make 100% On-Time Payments

This is 35% of your score.

Even one delay now can make things worse.

Step 5: Let Time Do Its Job (Important)

Most drops from loan payoff recover in:

- 30–60 days (minor drop)

- 60–90 days (bigger drop)

If you’re doing things right, your score will bounce back.

Insider Insight: How Lenders Actually See This

Banks don’t think like you.

You think:

“I paid my loan → I’m safer”

They think:

“This person now has less active credit behavior”

Credit scoring is not emotional. It’s pattern-based.

Lenders want to see:

- Consistent activity

- Controlled usage

- Long history

Not just “paid off debt”

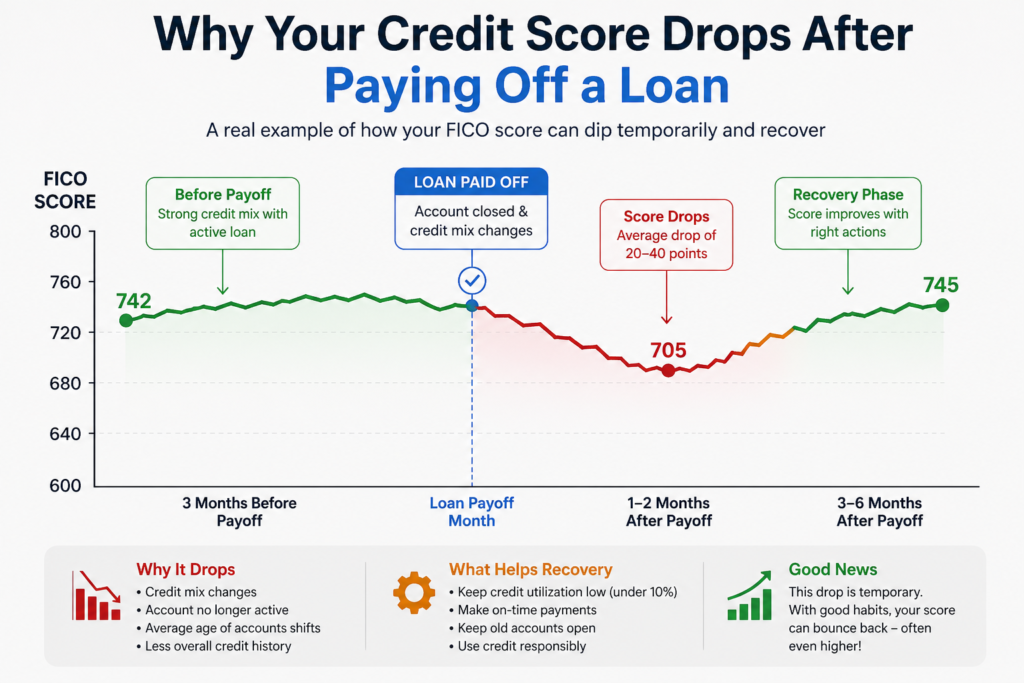

Real-Life Case Study (USA)

John, Texas (2025)

- FICO Score: 742

- Paid off $15,000 auto loan

- Score dropped to: 705

Why?

- Lost installment credit

- Only 1 credit card left

- Credit mix reduced

What he did:

- Opened a secured card

- Kept utilization under 10%

- No late payments

After 60 days:

- Score went back to 735

After 120 days:

- Score reached 755

Sarah, California (2026)

- Score before payoff: 768

- Paid off student loan

- Score dropped to: 728

What went wrong:

- Only 1 credit card left

- Utilization at 40%

- No new activity

Fix applied:

- Reduced utilization to 8%

- Opened second credit card

- Set auto-pay

Result:

- 45 days → 750

- 90 days → 770

Comparison Table: What Helps vs What Hurts

| Action | Impact on Score | Speed |

|---|---|---|

| Keep utilization under 10% | High positive | Fast |

| Open new credit line | Moderate positive | Medium |

| Close old accounts | High negative | Immediate |

| Miss payments | Severe negative | Immediate |

| Wait with good behavior | Positive | Slow |

WHAT BANKS REALLY CHECK (INSIDER LAYER)

Let’s be honest — FICO score is just the surface.

When you apply for credit, lenders also check:

- Active tradelines

- Recent activity (last 3 months)

- Stability patterns

If you paid off a loan and:

- Stopped using credit

- Have low activity

They may see you as:

“Inactive borrower → unpredictable”

REAL PATTERN OBSERVATION (VERY IMPORTANT)

From real credit behavior trends:

People who recover fastest are NOT:

- Debt-free people

They are:

- People who use credit strategically

That means:

- Controlled usage

- Active accounts

- Consistent payments

Mistakes People Make

- Closing credit cards after loan payoff

- Applying for too many loans at once

- Ignoring credit utilization

- Panicking and doing nothing

- Not checking credit report

COMPARISON TABLE (ACTION FOCUSED)

| Situation | What Happens | What You Should Do |

|---|---|---|

| Loan closed + no other credit | Score drops | Add credit line |

| High utilization after payoff | Score drops more | Reduce to <10% |

| No activity for 2 months | Score stagnates | Use card monthly |

| Multiple hard inquiries | Score drops | Pause applications |

HIDDEN MISTAKE (VERY COMMON)

People think:

“I paid off debt → I should stop using credit”

This is the biggest trap.

In the US system:

No credit usage = no credit growth

MAINTAINMARKET PRO TIP (ADVANCED)

If your goal is 750+ score, follow this formula:

- 2–3 active accounts

- Utilization under 10%

- No missed payments

- At least 1 installment + 1 revolving credit

That combination is what top scorers maintain.

MaintainMarket Expert Advice

Here’s the truth:

A credit score drop after loan payoff is not a problem — it’s a phase.

The real problem is what you do next.

Most people:

- Stop using credit

- Lose activity

- Score stagnates

Smart users:

- Maintain activity

- Optimize utilization

- Build stronger profile

That’s how they cross 750+.

Why MaintainMarket is Different

Most websites explain what happened.

We show you:

- How lenders think

- What actually works in real life

- What actions move your score fast

No theory. Only practical strategy.

Action Plan (Do This Now)

- Check your credit utilization (reduce it today)

- Keep all old accounts active

- Avoid new hard inquiries for 30 days

- Add one active credit line if needed

- Track your score weekly

FINAL REALITY CHECK

If your score dropped after loan payoff:

- You are NOT in danger

- You are NOT doing anything wrong

- You are simply in a transition phase

The difference between:

- People who stay stuck

- People who grow

Is how they respond after this moment.

Conclusion

Your score didn’t drop because you failed.

It dropped because your credit profile changed.

And once you understand that — you can control it.

Fix your utilization. Keep activity alive. Be consistent.

Your score won’t just recover — it can become stronger than before.

FAQs – FICO Score Dropped After Paying Off Loan

Q1. How much can my FICO score drop after paying off a loan?

Usually 10–40 points depending on your credit profile.

Q2. How long does it take to recover?

30–90 days in most cases.

Q3. Should I avoid paying off loans early?

No. Financial health is more important than a temporary score drop.

Q4. Does closing a loan hurt credit permanently?

No, the impact is temporary.

Q5. Should I open a new loan to fix it?

Only if your profile becomes too thin.

Q6. Why did my score drop even with perfect payment history?

Because credit scoring also depends on active accounts and mix.

Q7. Will my score increase again automatically?

Yes, if you maintain good habits.

Q8. Is this normal in the USA credit system?

Yes, very common with FICO scoring.

People searched for: How to Recover 100 Point Credit Score Drop Fast – Hacks Banks Won’t Tell You

Also read: 15 Best Side Hustles From Home USA (Earn $1000+/Month) – Real Guide 2026]

10 Safest Investment with High Returns in USA 2026 – Low Risk Options Ranked by Stabilit

1 thought on “Why FICO Score Dropped After Paying Off Loan (Fix Fast 2026)”