Credit score stuck and not improving? Discover the real reasons and proven steps to increase your score fast in the USA (with real examples). Let’s talk about Credit Score Not Improving and how you can fix it.

If your credit score is not improving in the USA, it is usually due to high credit utilisation, lack of credit activity, limited credit mix, or errors in your credit report. The fastest way to fix it is by reducing your utilization below 10%, adding a new credit account, and ensuring your credit report is accurate.

Introduction

You did everything right.

You paid your bills on time.

You avoided late payments.

You even reduced your credit card usage.

But your credit score?

Still stuck.

Not going up. Not improving. Just… frozen.

And that’s where most people get confused.

Because no one tells you this clearly:

A credit score doesn’t improve just because you behave well.

It improves when you behave strategically.

If your score hasn’t moved in weeks (or months), there’s always a reason behind it.

Let’s break it down—and fix it.

Quick Answer Box – Credit Score Not Improving

If your credit score is not improving, the most common reasons are:

- High credit utilization (above 30%)

- No new credit activity

- Lack of credit mix

- Old negative marks still active

- Errors in your credit report

To fix it:

- Keep utilization below 10%

- Add a new credit account (secured card or builder loan)

- Check and correct your credit report

- Maintain consistent usage and payments

Why Your Credit Score Is Stuck (Real Reasons)

1. You’re “Too Safe” With Credit

A lot of people think:

“If I stop using credit, my score will go up.”

Wrong.

Credit scoring models reward activity, not silence.

If you’re not using your cards at all, your profile becomes inactive.

That slows down improvement.

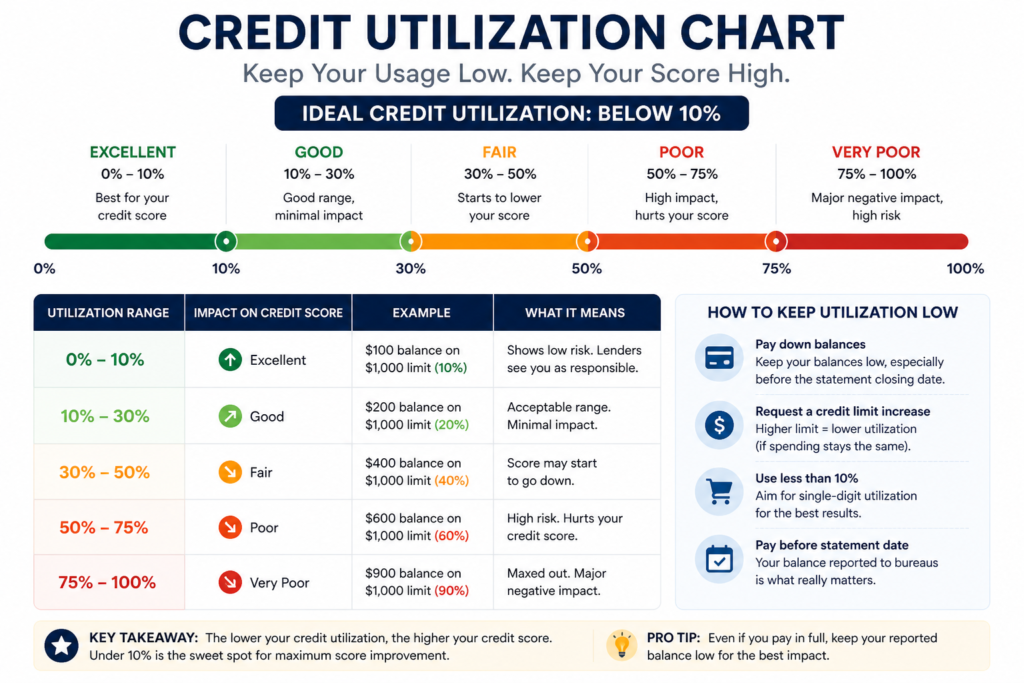

2. Your Credit Utilization Is Quietly High

Even if you pay on time, this can kill your progress.

Example:

- Limit: $2,000

- Usage: $600 → 30%

That’s already borderline.

Best range?

- Under 10% = ideal

- Under 30% = acceptable

Anything above that = slow growth

3. You Only Have One Type of Credit

If your profile only has:

- Credit cards (revolving)

But no:

- Installment loans

Your score stays limited.

Lenders want to see variety.

4. Old Negative Records Are Still Active

Late payments, collections, charge-offs…

These don’t disappear quickly.

In the US:

- They stay up to 7 years

So even if you’re perfect now, past mistakes still weigh you down.

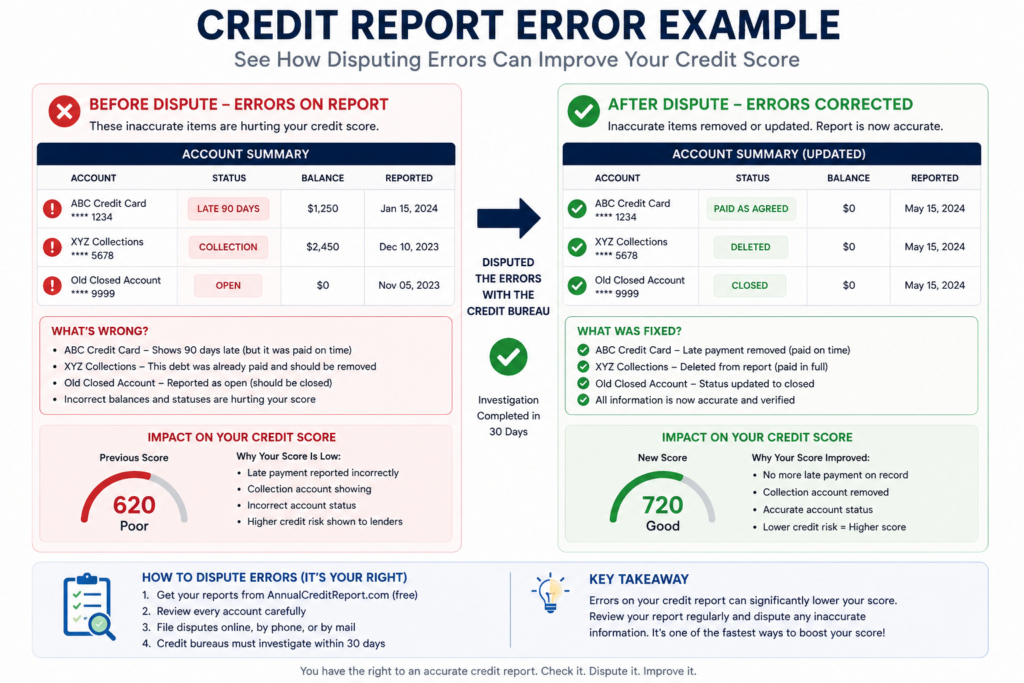

5. Your Credit Report Has Hidden Errors

This is more common than people think.

Wrong balances

Duplicate accounts

Incorrect late payments

These silently block your score.

6. Your “Credit Limit” Is Too Low

Even if your usage looks low…

👉 Small limits = less scoring power

Example:

- $300 limit, using $30 (10%)

Still weak profile

Better:

- $2,000 limit, using $200 (10%)

👉 Same percentage, but stronger signal

7. You Paid Off a Loan — And That Hurt Your Score

Yes, this surprises people.

When you close a loan:

- Your credit mix reduces

- Your active accounts drop

👉 Result: Score may stagnate or dip

8. Your Accounts Are Too New

If your credit history is:

- Less than 6–12 months

👉 Your score won’t grow fast

Lenders trust age + consistency, not just behavior.

9. You Applied for Too Much Credit Recently

Each hard inquiry:

- Slightly lowers your score

- Signals “credit hungry behavior”

👉 Multiple applications = slower growth

10. Your Statement Balance Is Always High

Even if you pay full:

👉 If your statement shows high balance → bad signal

Fix:

Pay before statement closing date

Step-by-Step Solution (What Actually Works)

Step 1: Fix Your Credit Utilization Immediately

This is the fastest win.

If you’re above 30%, reduce it ASAP.

If you want faster growth:

Target under 10%.

Step 2: Add One New Credit Line

Options:

- Secured credit card

- Credit builder loan

This improves:

- Credit mix

- Activity

- Score potential

Step 3: Pay Before the Statement Date

This is something most people don’t know.

If you pay AFTER statement generation:

Your high balance is already reported.

Instead:

Pay BEFORE the statement date.

Step 4: Check Your Credit Report

In the US:

You can access reports for free.

Check for:

- Wrong balances

- Fake late payments

- Unknown accounts

Fixing just ONE error can boost your score significantly.

Step 5: Stay Consistent for 60–90 Days

Credit score changes based on patterns.

Not one-time actions.

Consistency wins.

Step 6: Increase Your Credit Limit (Without Spending More)

Options:

- Request limit increase

- Open second card

👉 This lowers utilization instantly

Step 7: Use the “Small Activity Trick”

Use your card like this:

- Spend $20–$50

- Pay before statement

👉 Shows activity + low risk

Step 8: Add an Installment Account

Options:

- Credit builder loan

- Small personal loan

👉 Improves credit mix (important for FICO)

Step 9: Become an Authorized User

This is underrated.

👉 Join someone’s old, good credit account

Benefits:

- Longer history

- Better utilization

- Instant boost potential

Insider Insight (How Lenders Actually Think)

Banks don’t just check:

“Did you pay?”

They check:

- How much you depend on credit

- How often you use it

- How balanced your profile is

They prefer:

- Low utilization

- Regular usage

- Mixed credit

They don’t like:

- Zero usage

- High dependency

- Irregular activity

Insider Truth (What Credit Bureaus Don’t Tell You)

Your credit score is not just about:

👉 “Good vs bad behavior”

It’s about:

👉 Predictability of your behavior

Lenders ask:

- Will this person use credit responsibly?

- Or depend on it too much?

That’s why:

- Zero usage ❌

- High usage ❌

- Controlled usage ✅

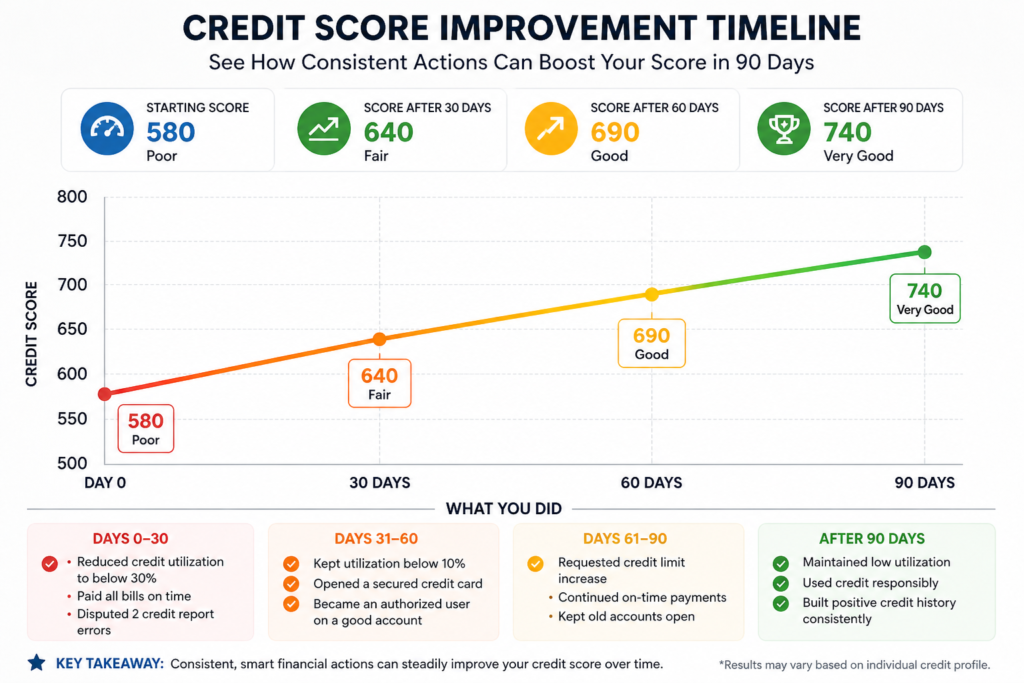

Real-Life Case Study (USA)

Michael (California):

- Credit score: 598

- Problem: High utilization + inactive account

What he did:

- Reduced usage from 75% to 8%

- Opened secured card ($300 limit)

- Paid before statement date

- Disputed one incorrect late payment

Result:

598 → 703 in 3 months

Comparison Table

| Problem | Impact | Fix |

|---|---|---|

| High utilization | Score stuck | Reduce below 10% |

| No activity | Slow growth | Use credit monthly |

| No credit mix | Weak profile | Add loan/card |

| Errors | Blocked score | Dispute report |

| Old negatives | Long-term drag | Wait + offset with good behavior |

Best Tools to Fix a Stuck Credit Score (USA)

| Tool | Best For | Why Use |

|---|---|---|

| Experian Boost | Instant score boost | Adds utility payments |

| Credit Karma | Monitoring | Free alerts + reports |

| Self Credit Builder | Build score | Helps create credit history |

| Kikoff | Low-cost credit building | Easy approval |

| Chime Credit Builder | Beginners | No credit check |

Mistakes People Make

- Paying only minimum due

- Closing old credit cards

- Applying for too many loans

- Ignoring credit reports

- Thinking time alone will fix score

Reality Check (Very Important Section)

If your score is stuck:

👉 It’s not broken

👉 It’s just not getting the right signals

Most people:

- Pay bills

- Wait

- Expect results

But credit doesn’t reward waiting.

It rewards strategy + consistency

Advanced Mistakes (People Don’t Realize)

- Using full limit then paying later

- Ignoring statement date

- Not increasing credit limit

- Having only 1 account

- Depending only on time

STRONGER ACTION PLAN (UPGRADE THIS)

Week 1:

- Check credit report

- Reduce utilization

Week 2:

- Add new credit account

- Start small usage

Week 3:

- Fix errors

- Increase limit

Week 4:

- Maintain low usage pattern

👉 Result:

Visible movement in 30–60 days

Also Read: How to Recover 100 Point Credit Score Drop Fast – Hacks Banks Won’t Tell You

MaintainMarket Expert Advice

If your score is stuck, don’t panic and apply for more credit blindly.

That makes it worse.

Instead:

Fix structure first.

Credit score growth is about controlled behavior, not quick hacks.

Why MaintainMarket is Different

Most websites tell you:

“Pay on time and your score will improve.”

That’s incomplete advice.

We focus on:

- Real-world strategies

- Practical execution

- Understanding how lenders think

Action Plan

Start today:

- Check your credit utilization

- Reduce balances immediately

- Get your credit report

- Fix any errors

- Add one new credit account

- Maintain consistency for 90 days

Conclusion

Your credit score is not stuck because it’s broken.

It’s stuck because:

👉 You’re doing basic things… not strategic things

Once you:

- Control utilization

- Add activity

- Improve structure

Your score WILL move.

FAQs – Credit Score Not Improving

Q1. Why is my credit score not increasing even after paying on time?

Because utilization, credit mix, and activity also matter.

Q2. How long does it take to improve a credit score?

Typically 30–90 days with proper strategy.

Q3. Does checking credit score hurt it?

No, soft checks don’t affect your score.

Q4. What is ideal credit utilization?

Below 10% for best results.

Q5. Can errors affect my credit score?

Yes, significantly.

Q6. Should I close old credit cards?

No, it reduces your credit history.

Q7. Can I increase my score quickly?

Yes, by reducing utilization and fixing errors.

Q8. Does taking a loan help?

Yes, if managed properly.

People searched for: Why FICO Score Dropped After Paying Off Loan (Fix Fast 2026)

Also read: 15 Best Side Hustles From Home USA (Earn $1000+/Month) – Real Guide 2026

3 thoughts on “Credit Score Not Improving? Fix It Fast (2026 Guide)”