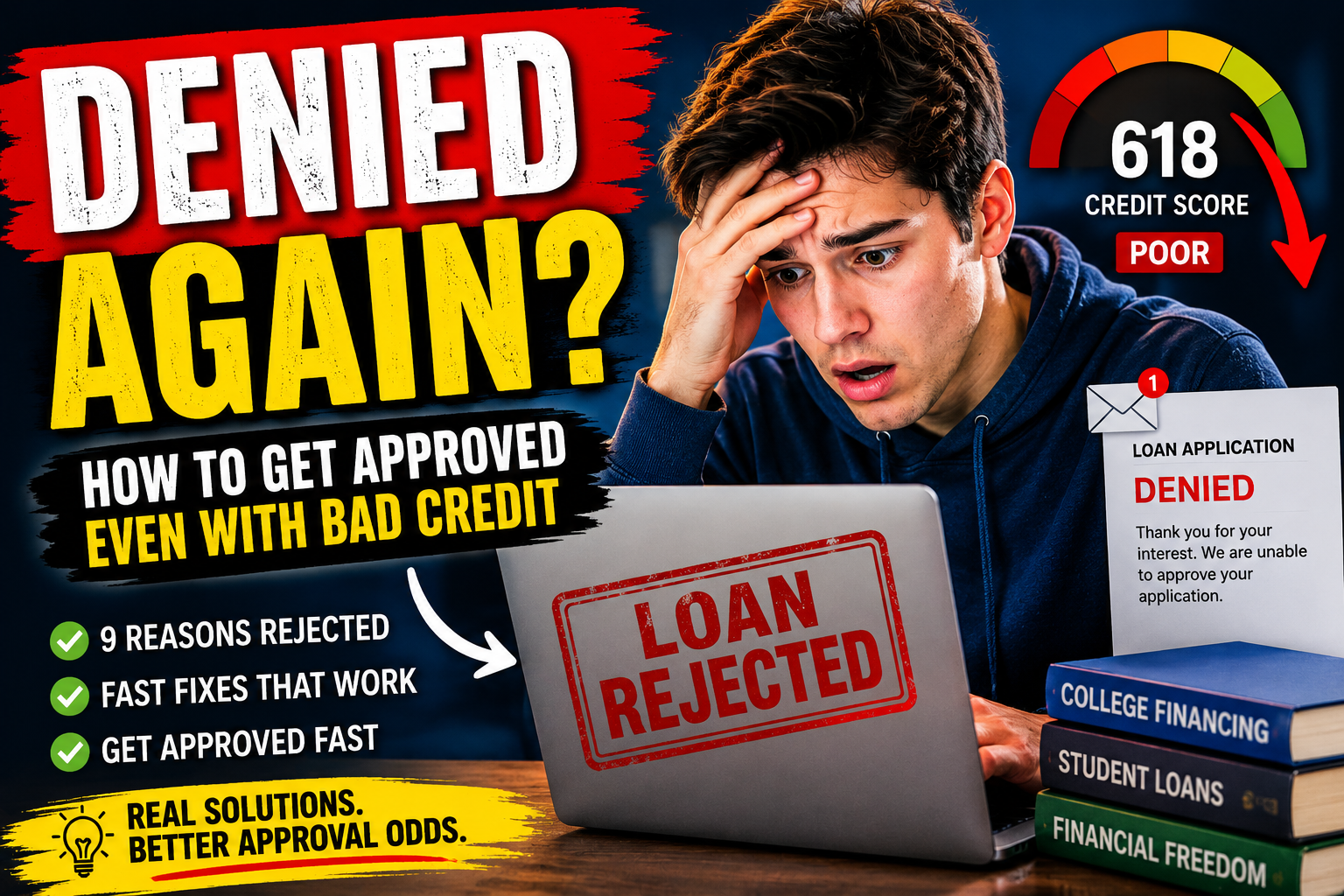

Private student loan denied? Learn the real reasons lenders reject applications and how to improve approval odds fast — even with bad credit or low income.

If your private student loan was denied, don’t rush into another application blindly. Take time to improve the factors lenders actually care about first. A smarter application can save you thousands later.

Introduction

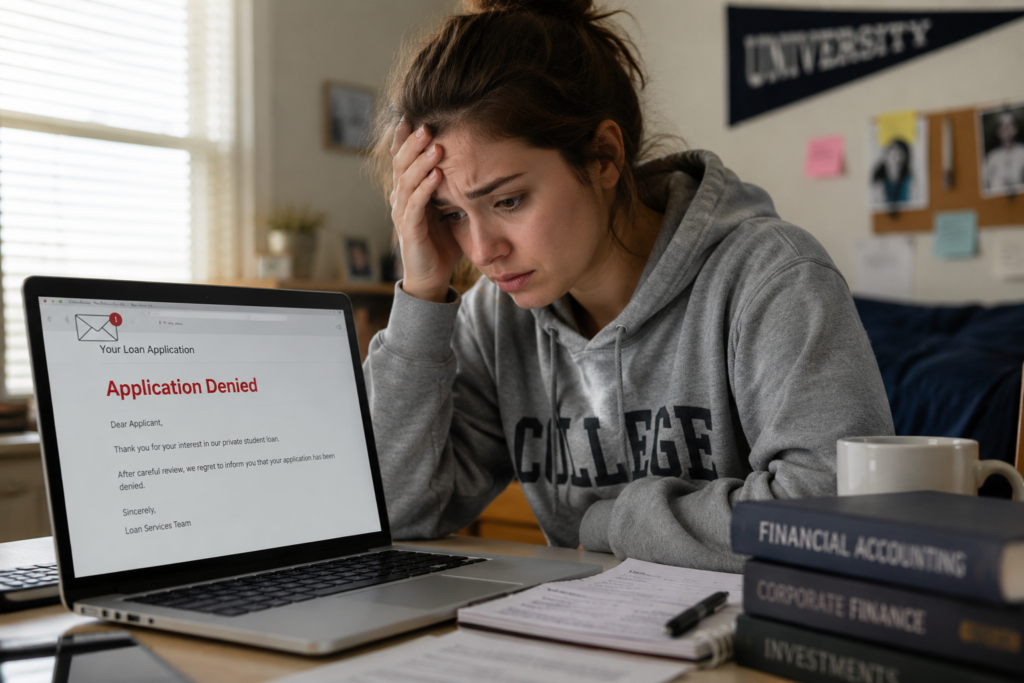

Getting denied for a private student loan feels personal.

You fill out the forms, submit your documents, wait for approval… and then suddenly you get that email:

“Unfortunately, we cannot approve your application at this time.”

For many students and parents in the U.S., that rejection creates panic immediately. Tuition deadlines get closer. Housing payments become uncertain. Some students even consider dropping semesters because they think they’ve run out of options.

But here’s the truth most finance websites never explain properly:

Private lenders are not rejecting you randomly.

They’re looking for very specific financial signals. And once you understand how lenders actually think, your chances of approval improve dramatically.

This guide will walk you through:

- Why private student loans get denied

- What lenders secretly care about most

- How to fix your application fast

- Ways to improve approval odds even with bad credit

- Real strategies students are using successfully in 2026

If you were denied recently, don’t apply again blindly.

That mistake alone can damage your credit even more.

Read this first.

Quick Answer Box

Why was your private student loan denied?

Most private student loan denials happen because of:

- Low credit score

- High debt-to-income ratio

- Insufficient income

- Thin credit history

- Missing cosigner

- Too many recent credit inquiries

- Enrollment verification issues

- Loan amount considered too risky

- Previous delinquent accounts

Fastest Ways to Improve Approval Odds

- Add a strong cosigner

- Reduce credit utilization below 30%

- Pay off small debts first

- Apply with lenders that accept fair credit

- Avoid multiple applications in short periods

- Check your credit report for errors

- Lower your requested loan amount

Why This Problem Happens

Most people think student loan approval is only about grades or college admission.

It’s not.

Private lenders care about risk.

They ask one question internally:

“Will this borrower realistically pay us back with interest?”

That’s it.

Unlike federal student loans, private lenders operate like businesses first. They analyze your financial profile almost the same way banks analyze personal loans or credit cards.

Here’s where students usually struggle.

Most students:

- Don’t have stable income

- Have little credit history

- Already carry credit card debt

- Depend on part-time jobs

- Have high future uncertainty

From the lender’s perspective, that creates risk.

And during economic uncertainty, lenders become even stricter.

The 9 Real Reasons You Got Denied

1. Your Credit Score Is Too Low

This is the biggest reason.

Most major private lenders prefer:

- 670+ for decent approval odds

- 700+ for strong rates

- 750+ for best terms

If your score is below 620, approvals become much harder without a cosigner.

What hurts scores most:

- Late payments

- Maxed-out cards

- Collections

- High utilization

- Multiple hard inquiries

What to Do

- Pay down revolving debt immediately

- Dispute credit errors

- Avoid new credit applications for 60 days

- Use autopay on existing accounts

2. You Don’t Have Enough Income

Even students with okay credit get denied because lenders don’t see enough repayment ability.

Many lenders want proof of:

- Stable employment

- Consistent income

- Low debt burden

Part-time income often isn’t enough.

This is why cosigners matter so much.

3. Your Debt-to-Income Ratio Is Too High

This number matters more than most students realize.

If you already owe:

- Credit cards

- Car loans

- Personal loans

- Buy-now-pay-later balances

…lenders worry you’re stretched too thin.

Ideal Debt-to-Income Ratio

Under 35% is safest.

Above 45% becomes risky.

4. Your Credit History Is Too Thin

This surprises many students.

You may have:

- No missed payments

- No collections

- No major debt

…but still get denied.

Why?

Because lenders don’t just want “clean” credit.

They want proven borrowing history.

A student with:

- 4 years of responsible credit usage

often gets approved faster than someone with:

- zero borrowing history

5. You Applied for Too Much Money

Many students request the maximum amount immediately.

That can trigger automatic rejection.

Lenders analyze:

- School type

- Expected future salary

- Graduation likelihood

- Major/field

- Existing aid

A $70,000 request for a low-income career field looks risky to lenders.

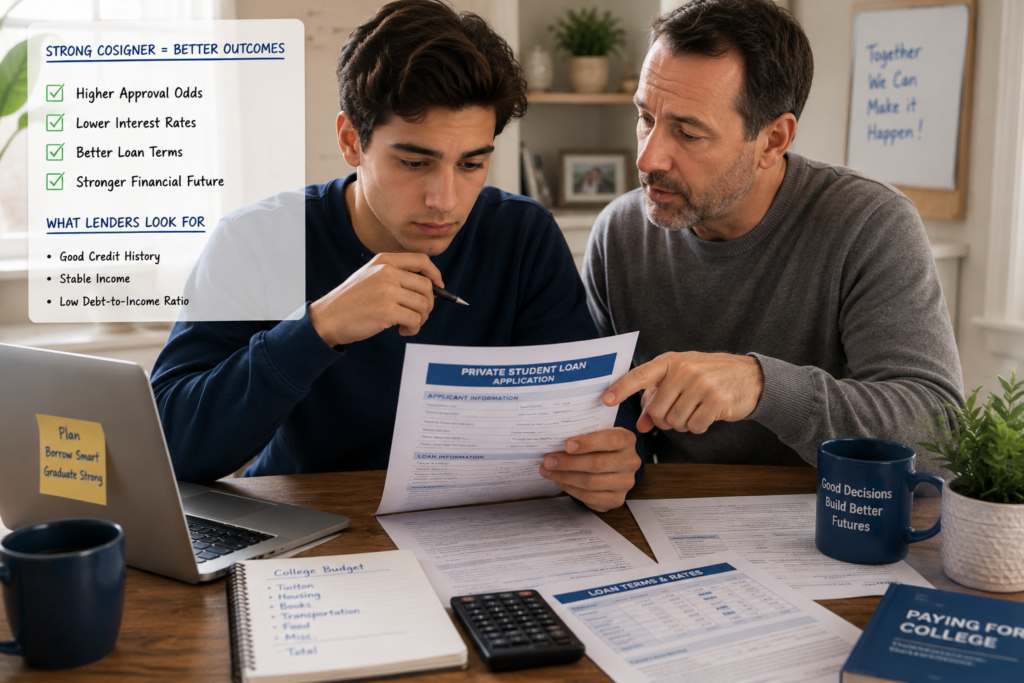

6. Your Cosigner Was Weak

Adding a cosigner doesn’t automatically solve approval issues.

If your cosigner has:

- High debt

- Poor credit

- Recent delinquencies

- Low income

…the application can still fail.

Strong cosigners usually have:

- 700+ credit score

- Stable employment

- Low debt ratios

- Long credit history

7. Too Many Recent Credit Applications

Applying repeatedly within weeks can scare lenders.

It signals desperation financially.

Each hard inquiry may also lower your score slightly.

One of the biggest mistakes students make:

Applying to 8–10 lenders immediately after rejection.

That usually worsens approval chances.

8. Enrollment or School Issues

Some lenders deny applications because:

- The school isn’t eligible

- Enrollment status changed

- Documentation was incomplete

- Program eligibility issues exist

This happens more often with:

- Online programs

- Certificate courses

- Unaccredited schools

9. Previous Financial Problems

Collections, defaults, bankruptcies, or charge-offs heavily impact approvals.

Even old issues matter.

Many lenders use automated underwriting systems that instantly flag:

- Recent collections

- Default history

- Charge-offs

- Missed payments

Step-by-Step Solution to Improve Approval Odds

Step 1: Stop Applying Repeatedly

Pause immediately.

Too many applications can damage your profile further.

Instead:

- Review denial reasons carefully

- Pull your credit report

- Fix weaknesses first

Step 2: Check Your Credit Report

Use:

- Experian

- Equifax

- TransUnion

Look for:

- Wrong late payments

- Duplicate debts

- Incorrect balances

- Fraudulent accounts

Credit report errors are more common than people think.

Step 3: Lower Credit Utilization Fast

This can improve scores surprisingly quickly.

Ideal Utilization

Under 30%

Best Range

Under 10%

Example:

If your limit is $2,000:

- Keep balances under $600

- Ideally under $200

Step 4: Get a Better Cosigner

This changes approval odds dramatically.

A strong cosigner can:

- Increase approval chances

- Reduce interest rates

- Improve loan limits

Many students get approved purely because of the cosigner profile.

Step 5: Reduce the Requested Amount

Sometimes asking for:

- $12,000 instead of $25,000

changes lender risk calculations completely.

Try:

- Scholarships

- Grants

- Payment plans

- Part-time work

- Community college transfer routes

to reduce borrowing needs.

Step 6: Compare the Right Lenders

Not all lenders use identical approval standards.

Some are more flexible toward:

- International students

- Fair credit

- No cosigner applicants

- Graduate students

This is where smart comparison matters.

Also read: $100 Only? Here’s How Beginners Are Growing It Safely in 2026

Insider Insights: How Lenders Actually Think

Most finance blogs never explain this properly.

Private lenders care less about your current situation and more about your future earning probability.

They analyze:

- Degree type

- School reputation

- Graduation likelihood

- Future salary potential

A medical student may get approved easier than someone pursuing a lower-income field because lenders expect stronger repayment ability later.

This is why two students with similar credit scores can receive completely different outcomes.

Another insider detail:

Lenders love stability.

Even small things help:

- Same address for years

- Stable phone number

- Consistent employment

- Low account turnover

Risk models reward predictable behavior.

Real-Life Case Study

How Jake From Texas Got Approved After 3 Rejections

Jake was a 22-year-old engineering student.

Initial Situation

- Credit score: 618

- Credit card debt: $3,200

- Requested loan: $28,000

- No cosigner

Result:

Rejected by 3 lenders.

What He Changed

- Paid down card balances to 15% utilization

- Reduced loan request to $14,000

- Added his aunt as cosigner (742 score)

- Waited 45 days before reapplying

Final Result

- Approved within 48 hours

- Interest rate dropped by 5.1%

- Saved nearly $9,000 long-term

The biggest difference wasn’t luck.

It was understanding lender psychology.

Comparison Table: Best Ways to Improve Approval Odds

| Strategy | Impact Level | Speed | Difficulty |

|---|---|---|---|

| Add strong cosigner | Very High | Fast | Medium |

| Lower credit utilization | High | Medium | Medium |

| Reduce loan amount | High | Fast | Easy |

| Improve credit score | Very High | Slow | Hard |

| Avoid multiple inquiries | Medium | Fast | Easy |

| Fix credit report errors | Medium | Medium | Medium |

| Increase income | High | Slow | Hard |

Mistakes People Make After Getting Denied

Applying Again Immediately

This hurts more than helps.

Ignoring Credit Report Errors

Small reporting mistakes can cost approvals.

Taking Extremely High-Interest Loans

Some desperate borrowers accept terrible rates.

That can become financially dangerous for years.

Borrowing More Than Necessary

Many students borrow for lifestyle costs rather than essential education expenses.

That creates long-term repayment pressure.

Choosing Variable Rates Without Understanding Risk

Variable rates may look cheaper initially.

But future payment increases can become painful.

Also read: How Does a Home Equity Loan Work? Complete Beginner’s Guide (2026)

MaintainMarket Expert Advice

If you’ve been denied, focus on fixing the root issue rather than chasing approvals emotionally.

The fastest path usually looks like this:

- Improve credit utilization

- Add a strong cosigner

- Reduce requested amount

- Wait 30–60 days

- Apply strategically

Also remember:

Federal student loans should almost always be explored before private loans because:

- They offer better protections

- Income-driven repayment exists

- Forgiveness programs may apply

- Credit requirements are less strict

Private loans should usually fill the remaining gap — not replace federal aid entirely.

Why MaintainMarket Is Different

Most finance websites:

- Repeat generic textbook information

- Don’t explain lender psychology

- Ignore real-world approval behavior

At MaintainMarket, we focus on:

- Real financial problems

- Actionable solutions

- Human explanations

- Practical strategies people can actually use

We write the kind of content we wish existed when people are stressed financially and searching for real answers at 2 AM.

Action Plan: What You Should Do Next

If Your Loan Was Denied Today

Within 24 Hours

- Pull your credit reports

- Review denial reasons carefully

- Stop multiple applications

Within 7 Days

- Pay down card balances

- Identify better cosigner options

- Reduce requested amount if possible

Within 30–60 Days

- Improve utilization

- Avoid late payments

- Reapply strategically

Before Reapplying

Ask yourself:

- Did my financial profile actually improve?

- Am I applying with the right lender?

- Is my requested amount realistic?

If the answer is no, wait longer.

Patience often improves approval odds more than repeated applications.

Conclusion

Getting denied for a private student loan feels discouraging, but it does not mean you’ve failed financially.

In most cases, lenders are reacting to risk signals — not your personal worth.

Once you understand:

- credit utilization,

- debt ratios,

- cosigner strength,

- and lender psychology,

…the process starts making far more sense.

The biggest mistake students make is panicking after rejection.

The smartest move is improving the application before trying again.

That single shift can save thousands of dollars in interest and dramatically increase approval chances.

FAQs

Q1. What credit score do I need for a private student loan?

Most lenders prefer at least 670, though some approvals happen below that with strong cosigners.

Q2. Can I get a private student loan with bad credit?

Yes, but approval is much easier with a qualified cosigner.

Q3. Does getting denied hurt my credit score?

The denial itself does not, but hard inquiries from applications may slightly reduce scores.

Q4. How long should I wait before applying again?

Usually 30–60 days after improving your financial profile.

Q5. Can I get approved without a cosigner?

Yes, though it’s harder for students with limited income or credit history.

Q6. Are federal loans better than private loans?

In most cases, yes. Federal loans typically offer stronger borrower protections.

Q7. Why did I get denied with a decent credit score?

Income, debt ratios, loan amount, or thin credit history may still create risk concerns.

Q8. Should I apply to multiple lenders at once?

Too many applications can hurt your profile. Compare carefully and apply strategically.

People also searched for: Credit Score 580? Personal Loan Approval Blueprint – USA (Step-by-Step Guide)

Also read: Do Student Loans Affect Credit Score? Hidden Truth + Fast Fixes (2026) – USA