Credit card usage in India has grown rapidly in recent years, making it important to ensure better transparency and customer protection. To address rising complaints related to hidden charges, unsolicited credit cards, and billing issues, the Reserve Bank of India (RBI) has introduced new credit card rules.

These RBI New Credit Card Rules 2026 aim to make credit card usage safer by improving transparency, strengthening customer rights, and ensuring banks follow fair practices. In this article, we explain the latest RBI guidelines and what every credit card holder in India should know.

Quick Decision Box

The Reserve Bank of India (RBI) has introduced several important credit card rules to improve transparency and protect customers from unfair banking practices.

Key highlights of the RBI New Credit Card Rules 2026:

✔ Banks cannot issue credit cards without customer consent

✔ Credit card closure requests must be processed within 7 days

✔ Banks must clearly disclose all credit card charges and fees

✔ Credit limits cannot be increased without customer approval

✔ Customers receive stronger protection against unauthorized transactions

These rules aim to make the Indian credit card system more transparent, secure, and consumer-friendly.

Why RBI Introduced New Credit Card Rules

Over the last decade, credit card usage in India has grown rapidly. Millions of consumers now rely on credit cards for everyday payments, online shopping, travel bookings, and subscription services.

While this growth has improved financial convenience, it has also created several problems for customers.

Common complaints reported by credit card users include:

- Hidden charges on credit card statements

- Automatic credit limit increases without approval

- Difficulty in closing unwanted credit cards

- Lack of transparency in billing statements

- Unauthorized credit card activation

Many consumers also reported being charged annual fees on credit cards they never requested or activated.

To address these issues, the Reserve Bank of India introduced stricter regulations for banks and financial institutions issuing credit cards.

The goal of these rules is to:

- Protect consumers from unfair banking practices

- Improve transparency in credit card fees and charges

- Strengthen security against fraud and misuse

- Ensure responsible lending by banks

These guidelines apply to all banks and financial institutions operating in India.

Growth of Credit Card Usage in India

The increasing popularity of digital payments has significantly boosted credit card adoption.

Approximate credit card growth in India:

| Year | Credit Card Users |

|---|---|

| 2018 | 36 Million |

| 2019 | 47 Million |

| 2020 | 55 Million |

| 2021 | 66 Million |

| 2022 | 75 Million |

| 2023 | 85 Million |

| 2025 | 100+ Million |

With more people using credit cards, stronger regulations became necessary to ensure fair practices.

Major RBI Credit Card Rules 2026

1. Credit Cards Cannot Be Issued Without Customer Consent

Earlier, some banks issued credit cards automatically to customers who already had savings accounts.

Customers sometimes received credit cards in the mail without requesting them.

Under RBI guidelines:

- Banks cannot issue unsolicited credit cards

- Cards must only be issued after explicit customer consent

If a bank sends an unsolicited card and charges fees, the customer is not responsible for paying those charges.

Banks violating this rule may face penalties from the RBI.

2. Transparent Disclosure of All Credit Card Charges

One of the most important RBI rules is transparency in fees and charges.

Banks must clearly inform customers about:

- Annual membership fees

- Interest rates on outstanding balances

- Late payment penalties

- Cash withdrawal charges

- Foreign transaction fees

- EMI processing fees

This information must be provided before the credit card is issued.

Banks cannot hide these charges in complicated terms and conditions.

3. Credit Card Closure Must Be Processed Within 7 Days

Many credit card users complained that closing a credit card was unnecessarily complicated.

Some banks delayed closure requests or tried to convince customers to keep the card.

Under the new RBI rules:

- Credit card closure must be completed within 7 working days after the customer request.

If banks delay the closure process, they may have to pay daily penalties to the customer.

This rule ensures that customers can easily stop using unwanted credit cards.

4. Credit Limit Cannot Be Increased Without Permission

Banks sometimes increased customer credit limits automatically.

While higher limits may seem beneficial, they can encourage overspending.

Under RBI regulations:

- Banks must obtain customer consent before increasing the credit limit.

Customers can also request a reduction in their credit limit if they want to control spending.

5. Protection Against Unauthorized Transactions

Credit card fraud is a major concern in the digital payment ecosystem.

RBI guidelines provide stronger protection against unauthorized transactions.

If a customer reports fraudulent activity:

- The bank must investigate the complaint quickly

- If the fraud occurred without customer negligence, the customer may have zero liability

Customers should report suspicious transactions as soon as possible.

RBI Rules on Credit Card Billing Transparency

Another important rule requires banks to provide clear and detailed billing statements.

Credit card statements must clearly show:

| Statement Item | Explanation |

|---|---|

| Total Outstanding Amount | Total amount owed by the customer |

| Minimum Due Amount | Minimum payment required |

| Interest Charges | Interest applied on unpaid balance |

| Late Payment Fee | Penalty for missing payment |

| Payment Due Date | Final payment deadline |

This helps customers understand the true cost of using their credit card.

RBI Penalties for Banks Violating Credit Card Rules

Banks that fail to follow RBI guidelines may face regulatory penalties.

Possible penalties include:

- Monetary fines

- Operational restrictions

- Mandatory refunds to customers

- Regulatory warnings from RBI

These penalties ensure that banks comply with consumer protection standards.

Old RBI Credit Card Rules vs New RBI Rules

| Old System | New RBI Rules |

|---|---|

| Banks could increase credit limits automatically | Customer consent required |

| Credit card closure could take weeks | Closure must be completed within 7 days |

| Fees often hidden in fine print | Full transparency required |

| Unsolicited cards sometimes issued | Cards require explicit customer approval |

The new system is designed to be much more consumer-friendly.

Real Case Study: Why RBI Introduced These Rules

A customer received a credit card from a bank without applying for it.

After several months, the bank charged an annual fee on the inactive card.

When the customer contacted the bank to close the card, the closure process was delayed.

Similar complaints were reported by thousands of consumers across India.

Due to these increasing complaints, the RBI introduced stricter credit card regulations.

These rules ensure that customers are not forced into unwanted financial products.

How RBI Credit Card Rules Benefit Customers

The new RBI guidelines provide several advantages for credit card users.

Key benefits include:

Greater Transparency

Customers now receive clear information about all charges before accepting a credit card.

Better Consumer Protection

Fraudulent transactions and unauthorized charges can be reported more easily.

Easier Credit Card Management

Customers can close credit cards quickly without unnecessary delays.

Responsible Lending

Banks must follow fair practices when issuing credit cards.

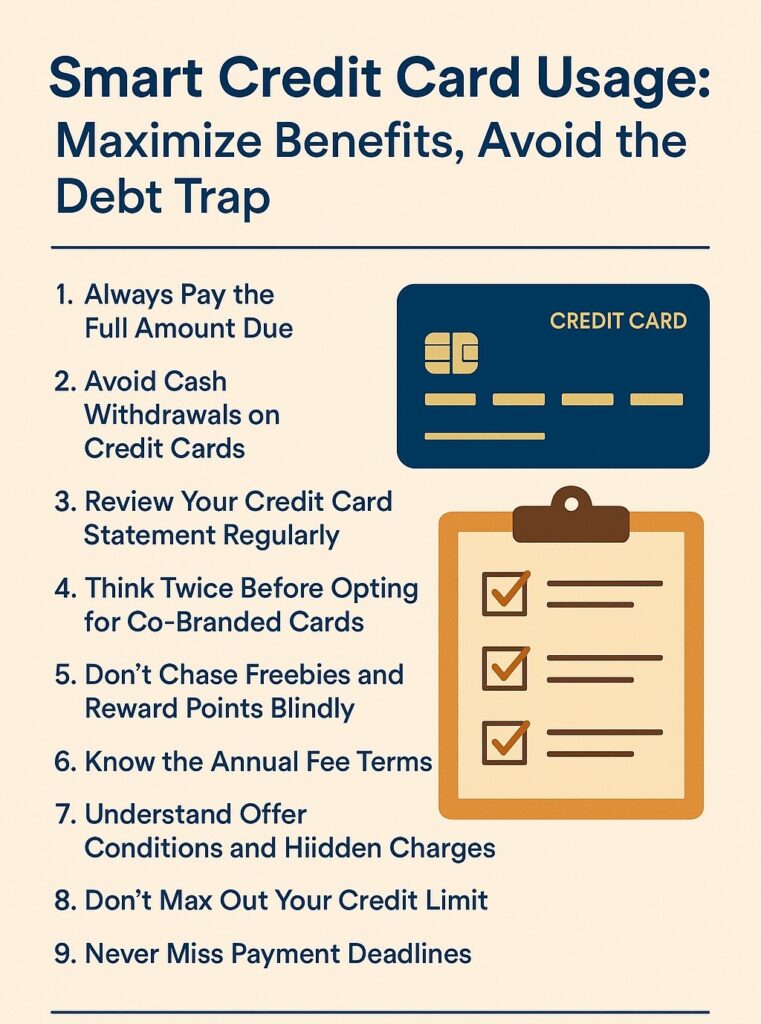

Common Mistakes Credit Card Users Still Make

Even with stronger regulations, many users still make costly mistakes.

Common credit card mistakes include:

- Paying only the minimum due amount

- Missing payment deadlines

- Using credit cards for ATM cash withdrawals

- Ignoring credit card statements

- Applying for too many credit cards

Avoiding these mistakes can help you save money and maintain a healthy credit score.

MaintainMarket Tested Advice for Credit Card Users

Based on common financial mistakes, here are the safest ways to use credit cards.

Always Pay the Full Bill

Paying only the minimum due leads to high interest charges.

Always pay the full outstanding balance before the due date.

Keep Credit Utilization Below 30%

Example:

Credit limit = ₹1,00,000

Recommended spending = ₹30,000 or less

This helps maintain a good credit score.

Enable Auto-Pay

Auto-pay ensures your credit card bill is automatically paid every month.

This prevents late payment penalties.

Monitor Your Monthly Statement

Check your statement for:

- Unauthorized transactions

- Hidden fees

- Subscription renewals

How to File a Complaint Against a Bank

If you face issues with your credit card provider, you can file a complaint.

Steps to follow:

- Contact your bank’s customer support.

- If unresolved, file a complaint through the RBI Banking Ombudsman Scheme.

- Submit the complaint through the RBI complaint portal.

The RBI reviews complaints and may take action against banks violating regulations.

Good vs Bad Credit Card Habits

| Smart Usage | Risky Usage |

|---|---|

| Pay full bill monthly | Pay minimum due |

| Track statements | Ignore charges |

| Use credit wisely | Overspend |

| Report fraud quickly | Delay reporting |

Responsible usage helps maintain financial stability and a strong credit score.

Final Action Plan

If you use a credit card in India, follow these steps:

✔ Always read the terms and conditions before activating a card

✔ Check all fees and charges carefully

✔ Monitor your monthly credit card statements

✔ Report suspicious transactions immediately

✔ Close unused credit cards to avoid unnecessary charges

Understanding RBI regulations helps you use credit cards safely while protecting your finances.

FAQs – RBI New Credit Card Rules

Q1. What are the new RBI credit card rules?

The RBI rules ensure transparency in charges, require customer consent before issuing cards, and make it easier to close credit cards.

Q2. Can banks increase credit card limits automatically?

No. Banks must obtain customer approval before increasing credit limits.

Q3. How quickly must banks close credit cards?

Banks must process credit card closure requests within 7 days.

Q4. What should I do if my credit card is misused?

Report the transaction to the bank immediately. Customers may have zero liability for unauthorized transactions.