Struggling to get a loan without income proof? Learn how to secure Emergency Loan Without Income Proof in 2026 in India & USA, even after rejection. Real methods, tips, and mistakes to avoid.

The Reality Nobody Tells You

You don’t need money when everything is going fine.

You need it when things break—medical bills, job loss, sudden expenses.

And that’s exactly when banks reject you.

No salary slip. No ITR. No approval.

But here’s the truth—getting an emergency loan without income proof is difficult, not impossible. You just need to play the system differently.

Quick Answer

Can you get a loan without income proof in 2026?

Yes—but not through traditional banks.

Best options:

- Digital lending apps (India & USA)

- Secured loans (gold, FD, crypto-backed)

- Co-applicant or guarantor-based loans

- BNPL or credit line services

- Peer-to-peer lending platforms

Approval depends on:

- Credit score

- Bank transaction history

- Assets or collateral

- Digital footprint

Why Banks Reject You Without Income Proof

Banks are not emotional—they’re risk machines.

Without income proof, you become:

- High risk

- Unpredictable borrower

- Low repayment confidence

So they reject instantly.

But here’s where you win:

New-age lenders don’t depend only on salary slips.

They check:

- Your spending pattern

- UPI transactions

- Savings behavior

- Digital credit profile

That’s your entry point.

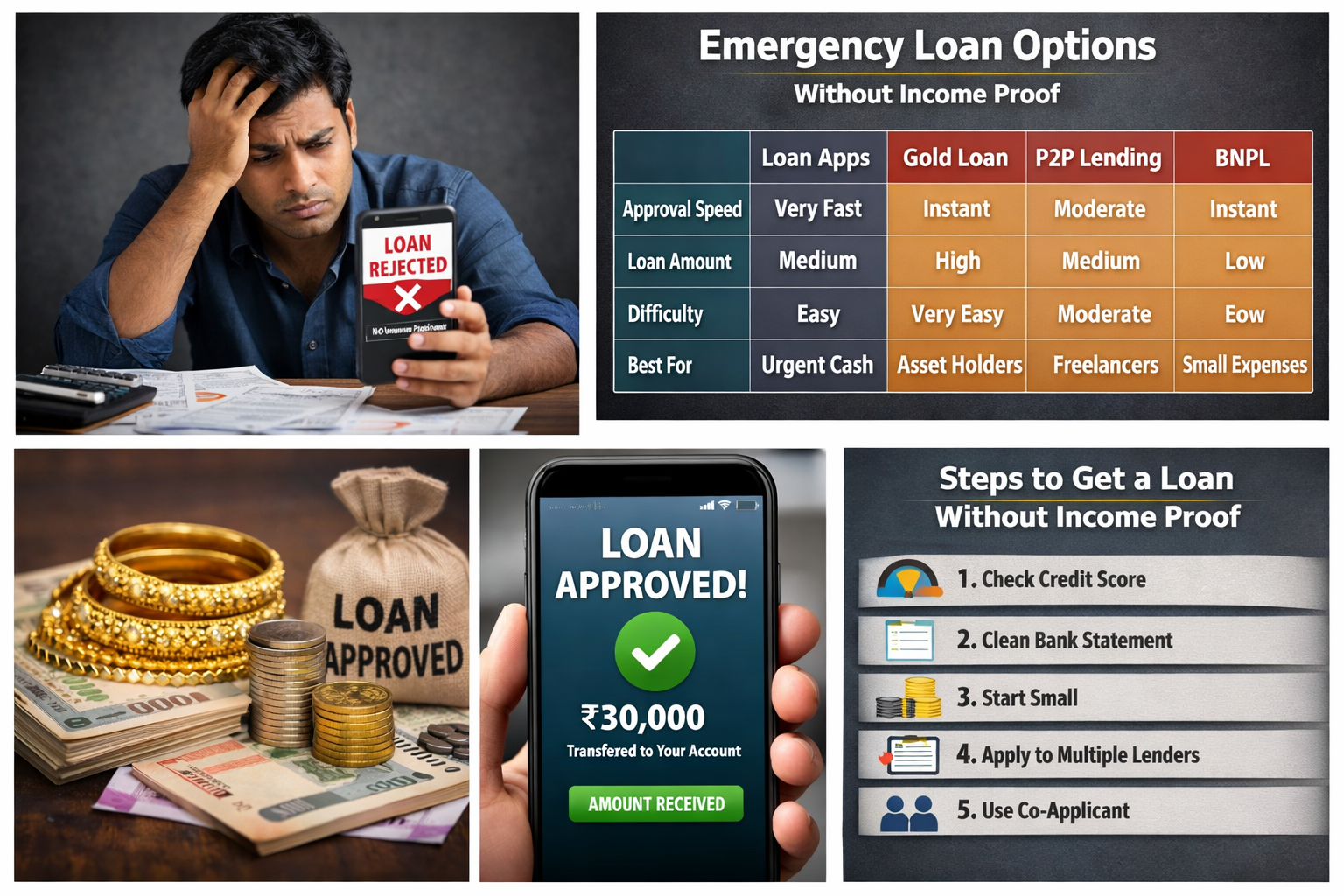

Best Ways to Get Emergency Loan Without Income Proof (India + USA)

1. Digital Loan Apps (Fastest Option)

These apps don’t ask for traditional income proof.

They analyze your digital behavior instead.

What they check:

- Bank account activity

- Mobile usage pattern

- Credit history (if any)

Typical loan range:

- India: ₹5,000 – ₹2,00,000

- USA: $100 – $5,000

Approval time: 10 minutes to 24 hours

2. Secured Loans (Easiest Approval)

If you have any asset, you can get money instantly.

| Asset Type | Loan Approval Speed | Risk | Interest Rate |

|---|---|---|---|

| Gold Loan | Very Fast | Low | Low |

| Fixed Deposit Loan | Instant | Very Low | Very Low |

| Crypto-backed Loan | Fast | Medium | Medium |

| Vehicle Loan | Medium | Medium | Medium |

Why this works:

Lenders don’t care about your income—they care about your asset.

3. Peer-to-Peer (P2P) Lending

Instead of banks, you borrow from individuals.

Best for:

- Freelancers

- Students

- Unemployed individuals

How it works:

- Create profile

- Explain your need

- Investors fund your loan

Advantage: Flexible approval

Disadvantage: Slightly higher interest

4. BNPL & Credit Lines

Buy Now Pay Later services act like micro-loans.

Examples of usage:

- Pay medical bills

- Cover emergency expenses

- Short-term cash flow

Limit: Smaller amounts but easy approval

5. Guarantor or Co-Applicant Loan

This is your backup strategy.

If someone with:

- Stable income

- Good credit score

joins your application, your approval chances increase massively.

Step-by-Step Process to Get Approved (Even Without Income Proof)

Step 1: Check Your Credit Score

Even without income, a good credit score is your weapon.

- India: 650+ works

- USA: 600+ minimum

If low, start with small loans first.

Step 2: Clean Your Bank Statement

Lenders check your last 3–6 months activity.

Avoid:

- Frequent zero balance

- Too many failed transactions

- Irregular deposits

Step 3: Start Small

Don’t apply for ₹2 lakh or $5,000 immediately.

Start with:

- ₹5,000–₹20,000

- $100–$500

Build trust → Increase limit later

Step 4: Apply Through Multiple Channels

Don’t depend on one lender.

Apply across:

- Apps

- P2P platforms

- Secured loan providers

Step 5: Use a Co-Applicant if Needed

If rejected 2–3 times, don’t keep applying.

Add a co-applicant and retry.

Real-Life Example

Rohit, 27, lost his job in Bangalore.

No salary slip. No income proof.

Urgent need: ₹30,000 for medical emergency.

What he did:

- Applied via 3 loan apps → rejected

- Used gold chain → got ₹40,000 gold loan in 30 minutes

Lesson:

When unsecured fails, secured wins instantly.

Comparison: Which Option is Best for You?

| Method | Approval Speed | Loan Amount | Difficulty | Best For |

|---|---|---|---|---|

| Loan Apps | Very Fast | Medium | Easy | Urgent needs |

| Gold/FD Loan | Instant | High | Very Easy | Asset holders |

| P2P Lending | Medium | Medium | Moderate | Freelancers |

| BNPL | Instant | Low | Very Easy | Small expenses |

| Co-applicant Loan | Medium | High | Easy | Rejected applicants |

Common Mistakes That Kill Your Approval

1. Applying Everywhere at Once

Too many applications = credit score drop

2. Choosing Fake Loan Apps

If it asks for upfront fees → RUN

3. Ignoring Interest Rates

Emergency doesn’t mean blind acceptance

4. Using Multiple Loans Together

Debt trap starts here

5. Not Reading Terms

Hidden charges can destroy you later

Expert Tips That Actually Work

- Always keep ₹5,000–₹10,000 buffer in bank

- Maintain minimum credit score above 650

- Use one small loan and repay on time

- Avoid payday loans unless last option

- Prefer secured loan for large amount

Hidden Ways Lenders Judge You (Even Without Income Proof)

Most people think income proof is everything. It’s not.

Lenders silently check:

- UPI transaction consistency (India)

- Card spending behavior (USA)

- Average monthly balance

- EMI repayment history (if any)

- Mobile app permissions (yes, some apps analyze behavior)

Pro Tip:

Even ₹10,000 monthly inflow consistently looks better than random ₹50,000 deposits.

Smart Hack: Use “Self-Employed” Strategy

If you don’t have a job, don’t position yourself as unemployed.

Instead:

Say you are:

- Freelancer

- Consultant

- Small business operator

Then support it with:

- Bank transactions

- UPI receipts

- Basic invoice screenshots (if needed)

This increases approval probability significantly.

Loan Stacking Strategy (Advanced)

This is what experienced borrowers do.

Instead of applying for one big loan:

- Take a small loan (₹5k / $100)

- Repay it quickly (within 7–15 days)

- Reapply → higher limit unlocked

Repeat 2–3 times → you can unlock:

- ₹50,000+ in India

- $1,000+ in USA

Best Timing to Apply for Emergency Loans

Timing actually matters.

Best days:

- Monday to Wednesday

- During working hours (10 AM – 6 PM)

Avoid:

- Late night applications

- Weekends

- Bank holidays

Why?

Because manual verification teams are active during working hours.

Warning: When NOT to Take an Emergency Loan

You should avoid taking a loan if:

- You don’t have any repayment plan

- You’re already paying 2+ EMIs

- You’re borrowing just for lifestyle spending

- Interest rate is above 30% annually

Emergency loan is a tool—not a solution.

Income Alternatives You Can Show (Instead of Salary Slip)

If you don’t have salary proof, you can still show:

- Freelance payments

- Rental income

- Bank transfers from family

- Online earnings (YouTube, affiliate, trading)

- Business cash flow

Even informal income can work if it’s consistent and traceable.

USA-Specific Tip (Very Important)

In the USA, lenders rely heavily on:

- Bank account cash flow analysis

- FICO score behavior

- Employment history (not just current income)

Even if you’re unemployed:

- A strong past record helps

- Stable banking activity increases approval

India-Specific Tip (Game Changer)

In India, your approval chances increase if:

- Your bank account is older than 1 year

- You have regular UPI usage

- You maintain ₹2,000–₹5,000 minimum balance

Even without income proof, this creates trust signals.

Psychological Trick That Increases Approval

When filling loan application:

Don’t write:

- “Emergency need”

- “Urgent money required”

Instead write:

- “Short-term personal expense”

- “Medical contingency support”

- “Working capital support”

Why?

Lenders prefer controlled borrowers, not desperate ones.

Red Flags That Instantly Reject Your Application

- Multiple bounced payments

- Negative bank balance

- Too many recent loan inquiries

- Fake or inconsistent information

- Frequent job changes (USA context)

How Much Loan Should You Actually Take?

Follow this simple rule:

Loan Amount ≤ 30% of your expected repayment capacity

Example:

- If you can repay ₹10,000 → take max ₹3,000–₹5,000 initially

This keeps you safe from debt traps.

Long-Term Fix (So You Never Face This Again)

Emergency loans are temporary.

Build this system:

- Create emergency fund (3–6 months expenses)

- Maintain one active credit line

- Keep credit score above 700

- Avoid zero balance accounts

- Use small credit regularly

This makes future loans effortless.

MaintainMarket Tested Insight

Based on borrower behavior patterns:

- People with small active loans + timely repayment

get approvals faster than those with no credit history - Even one ₹2,000 loan repaid on time

can unlock ₹20,000+ limit later

Bonus: Fast Approval Checklist

Before applying, check this:

- Bank account active (last 3 months)

- No negative balance

- At least some inflow visible

- Credit score checked

- Applying during working hours

- Not applied to 5+ lenders already

If all YES → your chances are high.

Internal Linking Suggestions (For MaintainMarket)

- “Best Personal Loan Apps in India 2026”

- “How to Improve Credit Score Fast”

- “Instant Loan Approval Tips”

Why MaintainMarket is Different from Others

Most websites give you theory.

MaintainMarket focuses on:

- Real approval strategies

- Practical methods that work in India + USA

- No fluff, only execution-based guidance

- Content designed for actual earning and decision-making

FAQs

Q1. Can I get a loan with zero income?

Yes, through secured loans or alternative lenders.

Q2. What is the easiest loan to get without income proof?

Gold loan or FD-backed loan.

Q3. Do loan apps verify income?

Not always. They check digital and financial behavior instead.

Q4. Is it safe to take emergency loans?

Yes, if you choose trusted platforms and read terms carefully.

Q5. What credit score is required?

650+ is ideal, but some apps approve even lower scores.

Final Action Plan

If you need money urgently:

- Try loan apps (fastest)

- If rejected → go for gold/FD loan

- If no asset → use P2P or co-applicant

- Start small → build trust → increase limit

Don’t chase approval.

Build eligibility.

3 thoughts on “Get Emergency Loan Without Income Proof in 2026: How to Get Money Fast When Banks Say No”