Most people lose 20–40 points and don’t even know WHY. If you act within 48 hours, you can sometimes reverse the damage completely. Learn how to remove hard inquiries from your credit report legally. Step-by-step dispute process, insider tips, and fast fixes to recover your credit score. In this article, let’s talk about Remove Hard Inquiry from Credit Report.

Introduction

You checked your credit score… and suddenly it dropped.

No missed payments. No new debt. Nothing unusual.

Then you see it — a hard inquiry.

This is where most people get confused.

They think: “Can I remove this?”

The truth? Sometimes yes. Sometimes no.

And this is where most articles lie to you.

They either say:

- “You can remove everything” (not true)

- Or “you can’t do anything” (also not true)

In this guide, I’ll show you what actually works in real life, not theory.

Quick Answer Box (Featured Snippet)

Can you remove a hard inquiry from your credit report?

- Yes, if it’s unauthorized, duplicate, or incorrect

- No, if it’s legitimate (but you can reduce its impact)

Fastest method:

Dispute the inquiry with credit bureaus (Experian, Equifax, TransUnion)

Timeframe:

- 24–72 hours (rare cases)

- 7–30 days (standard process)

Why Hard Inquiries Hurt Your Credit Score

Let’s be real — the drop is usually 5–10 points, sometimes more.

But the real problem isn’t just the points.

It’s how lenders see you.

Here’s how banks think:

- “Too many inquiries = this person is desperate for credit”

- “High risk of default”

- “Possible loan rejection”

Even if you’re financially stable.

That’s the problem.

Why Hard Inquiries Appear (Real Reasons)

Not all inquiries are your fault.

1. You applied for credit

- Credit card

- Personal loan

- Car loan

2. Dealer or agent ran multiple checks

One application → multiple inquiries

3. Unauthorized inquiry (this is GOLD opportunity)

- Someone used your details

- Or a company checked without permission

4. Pre-approved offers turned into hard checks

Happens more than you think

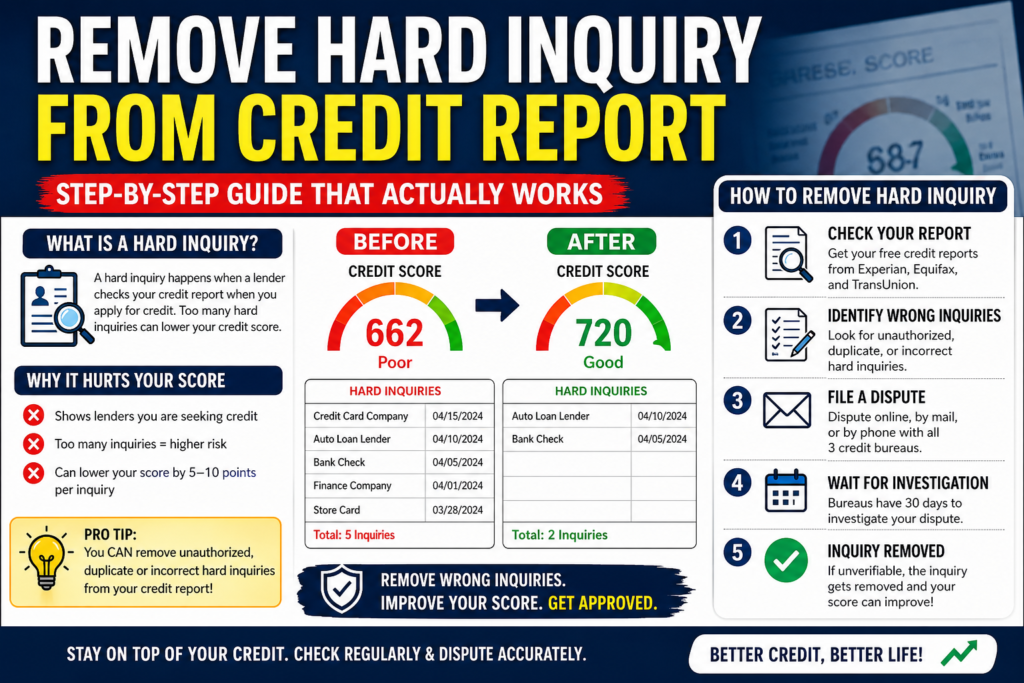

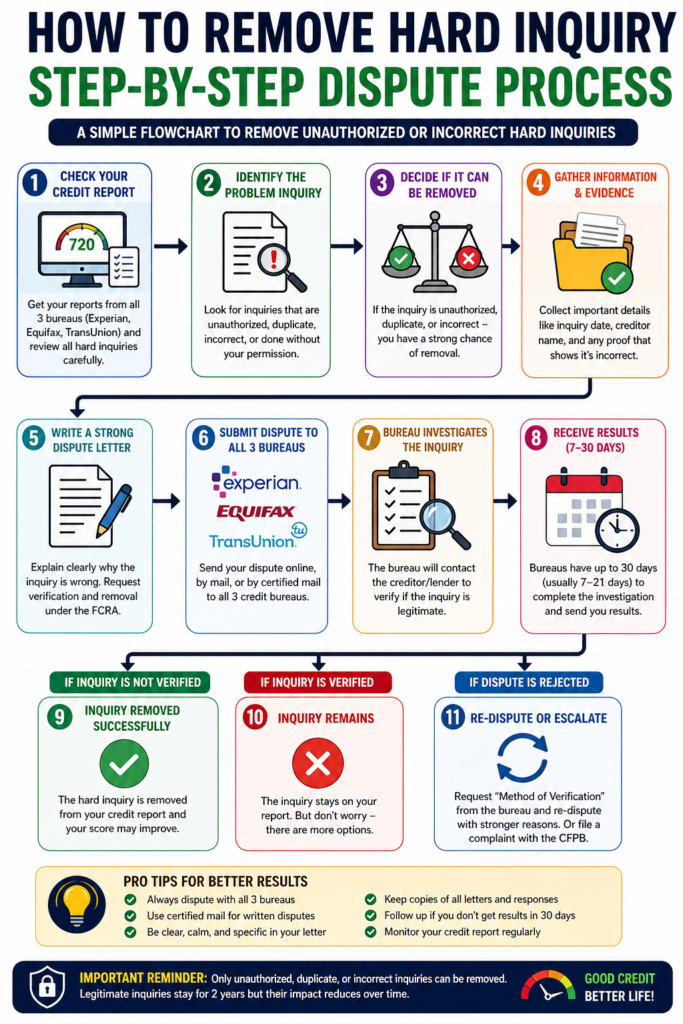

Step-by-Step: How to Remove Hard Inquiry (Real Process)

Step 1: Check Your Credit Report Properly

Use:

- Experian

- Equifax

- TransUnion

Look for:

- Unknown lenders

- Duplicate entries

- Wrong dates

Step 2: Identify If It’s Removable

| Situation | Can Remove? |

|---|---|

| Unauthorized inquiry | Yes |

| Duplicate inquiry | Yes |

| Incorrect details | Yes |

| Legitimate application | No |

Step 3: File a Dispute (Most Important Step)

You need to challenge the inquiry.

What to write:

- “I did not authorize this inquiry”

- Ask for verification proof

- Demand removal if unverifiable

Step 4: Send Dispute to All 3 Bureaus

- Experian

- Equifax

- TransUnion

Do NOT rely on just one.

Step 5: Wait for Investigation

- Bureau contacts lender

- If no proof → inquiry removed

This is where most people win.

Insider Insight: Why Disputes Actually Work

Here’s what no one tells you:

Credit bureaus don’t deeply investigate everything.

They:

- Send request to lender

- Wait for response

If lender:

- Doesn’t respond

- Gives weak proof

→ Inquiry gets removed

That’s your leverage.

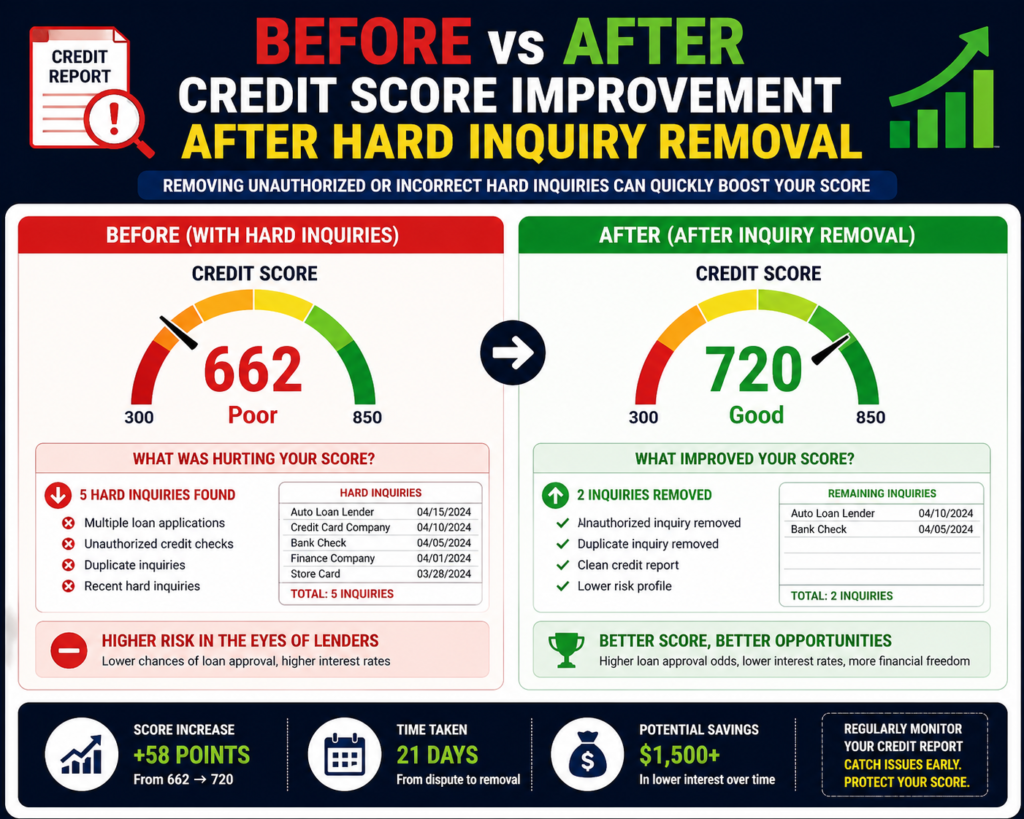

Real-Life Case Study (USA Example)

John from Texas applied for a car loan.

Dealer ran 5 hard inquiries instead of 1.

His score dropped from 720 → 682

What he did:

- Filed disputes with all bureaus

- Claimed duplicate/unauthorized checks

Result:

- 3 inquiries removed

- Score recovered to 705 in 21 days

This happens more often than you think.

Comparison Table: Removal Options

| Method | Speed | Success Rate | Best For |

|---|---|---|---|

| DIY dispute | Medium | High | Unauthorized inquiries |

| Credit repair service | Fast | Very High | Multiple issues |

| Waiting | Slow | Guaranteed | Legit inquiries |

| Goodwill request | Low | Low | Rare cases |

How Long Hard Inquiries Actually Affect Your Score (Reality vs Myth)

Most people hear “2 years” and panic.

But here’s the truth:

- Visible on report: 2 years

- Affects score heavily: First 3–6 months

- Minor impact after: 6–12 months

- Almost no impact: After 12 months

What this means for you:

If your inquiry is:

- Less than 30 days old → ACT FAST (dispute window advantage)

- 3+ months old → focus on score recovery instead of removal

This mindset shift alone can save you time.

Remove Multiple Inquiries at Once

If you applied for:

- Car loan

- Mortgage

- Student loan

You may see multiple inquiries in a short time.

Here’s the trick:

Credit scoring models often treat them as ONE inquiry (rate shopping window)

- Auto loans → 14–45 days window

- Mortgage → 14–45 days

What you should do:

- Dispute duplicate lenders

- Mention: “These were rate-shopping inquiries and should be treated as one”

This increases success rate.

Dispute Letter Template

Use this when filing disputes:

Subject: Unauthorized Hard Inquiry Dispute

I am writing to dispute a hard inquiry listed on my credit report.

Creditor Name: [Insert Name]

Date of Inquiry: [Insert Date]

I did not authorize this inquiry. Under the Fair Credit Reporting Act (FCRA), I request verification of this inquiry.

If you cannot provide valid proof, I request immediate removal from my credit report.

Sincerely,

[Your Name]

Simple. Direct. Works.

Pro Tip: Dispute Online vs Mail (What Actually Works Better)

| Method | Speed | Effectiveness |

|---|---|---|

| Online dispute | Fast | Medium |

| Mail dispute | Slower | High |

| Phone | Fast | Low |

Real insight:

- Online = quick but generic

- Mail = taken more seriously

If you’re serious about removal → use both

What If Your Dispute Gets Rejected? (Most People Get Stuck Here)

This is where 80% people give up.

Don’t.

Do this instead:

- Request method of verification

- Ask:

- Who verified it?

- What proof was provided?

- Re-dispute with stronger wording

Why this works:

Credit bureaus hate repeated legal pressure.

Little-Known Trick: Contact the Creditor Directly

Instead of only fighting bureaus…

Go to the source.

Steps:

- Call lender directly

- Say:

“I did not authorize this inquiry. Please remove it from your end.”

If they agree → they notify bureau → removal happens faster

Soft Inquiry Conversion Trick (Advanced)

Some inquiries can be reclassified.

Example:

- Pre-approval → should be soft inquiry

- Employer check → soft inquiry

What to do:

Dispute with this wording:

“This inquiry should be classified as a soft inquiry, not hard.”

This works in specific cases.

Score Recovery Strategy (If Removal Fails)

Let’s be practical — not everything gets removed.

So here’s how to recover fast:

1. Reduce Credit Utilization

Keep below 30% (ideal: 10%)

2. Pay Bills Before Due Date

Not on due date — before

3. Become Authorized User

Piggyback on strong credit account

4. Avoid New Applications

Each inquiry adds damage

Hidden Danger: Too Many Hard Inquiries

If you have:

- 1–2 inquiries → normal

- 3–5 → risky

- 6+ → red flag

Lender psychology:

More inquiries = credit hungry behavior

That leads to:

- Loan rejection

- Lower limits

- Higher interest rates

When You SHOULD NOT Dispute Hard Inquiries

This is important.

Do NOT dispute if:

- You actually applied

- It’s correctly reported

- It’s recent and valid

Why?

Too many disputes can:

- Flag your profile

- Reduce credibility

Best Tools to Monitor and Fix Faster

Recommended tools:

- Credit monitoring apps

- Identity theft protection services

- Credit repair platforms

Psychological Trigger: Why People Panic After Inquiry

Let’s be real.

People don’t panic because of 10 points drop.

They panic because:

- Loan might get rejected

- Credit card may not approve

- Financial image looks weak

Mistakes People Make (Very Important)

- Disputing legitimate inquiries

→ wastes time - Not checking all 3 bureaus

→ incomplete fix - Writing weak dispute

→ rejected instantly - Expecting instant removal

→ unrealistic - Applying for more credit

→ makes things worse

MaintainMarket Expert Advice

If your inquiry is unauthorized, act immediately.

If it’s legitimate, don’t chase removal blindly.

Instead:

- Pay bills on time

- Keep utilization low

- Avoid new applications

Within 3–6 months, impact reduces significantly.

Why MaintainMarket is Different

Most websites:

- Give generic advice

- Copy textbook definitions

We focus on:

- Real scenarios

- Actual success strategies

- Lender psychology

Because that’s what actually moves your score.

Action Plan (Do This Now)

- Pull your credit report

- Highlight suspicious inquiries

- Dispute unauthorized ones

- Monitor status weekly

- Avoid new credit applications

Conclusion

A hard inquiry is not the end of your credit score.

But ignoring it? That’s where damage happens.

If it’s wrong — remove it.

If it’s right — manage it smartly.

That’s the difference between:

- A rejected loan

- And an approved one

FAQs

Q1. Can I remove hard inquiries in 24 hours?

Rare, but possible if lender doesn’t verify quickly.

Q2. How many points does a hard inquiry drop?

Usually 5–10 points.

Q3. Do hard inquiries go away automatically?

Yes, after 2 years.

Q4. Can I remove legitimate inquiries?

No, but you can reduce impact.

Q5. Is credit repair service worth it?

Yes, if you have multiple issues.

Q6. Does checking my own score hurt?

No (soft inquiry).

Q7. Can multiple inquiries be grouped?

Yes (rate shopping window).

Q8. Which bureau is easiest to dispute?

Depends, but all follow similar process.

Q9. Can I sue for unauthorized hard inquiry?

Yes, under FCRA if damage is proven.

Q10. How many disputes can I file?

No strict limit, but avoid spam disputes.

Q11. Do all lenders report inquiries?

Most do, but not all.

Q12. Does removing inquiry increase score instantly?

Sometimes yes, but not always

People searched for: 7 Silent Reasons Destroying Your FICO Score Right Now – Fico score dropped without reason

Also read: 7 Best Credit Builder Apps in the USA That Can Boost Your Score Even If It’s Below 600

1 thought on “Hard Inquiry Ruined Your Credit Score? Here’s How to Remove Hard Inquiry from Credit Report”