Lost 100 points on your credit score? Learn the real reasons and step-by-step strategies to recover your credit fast and avoid loan rejection. In this article, let’s talk about how to recover 100 point credit score drop.

Introduction

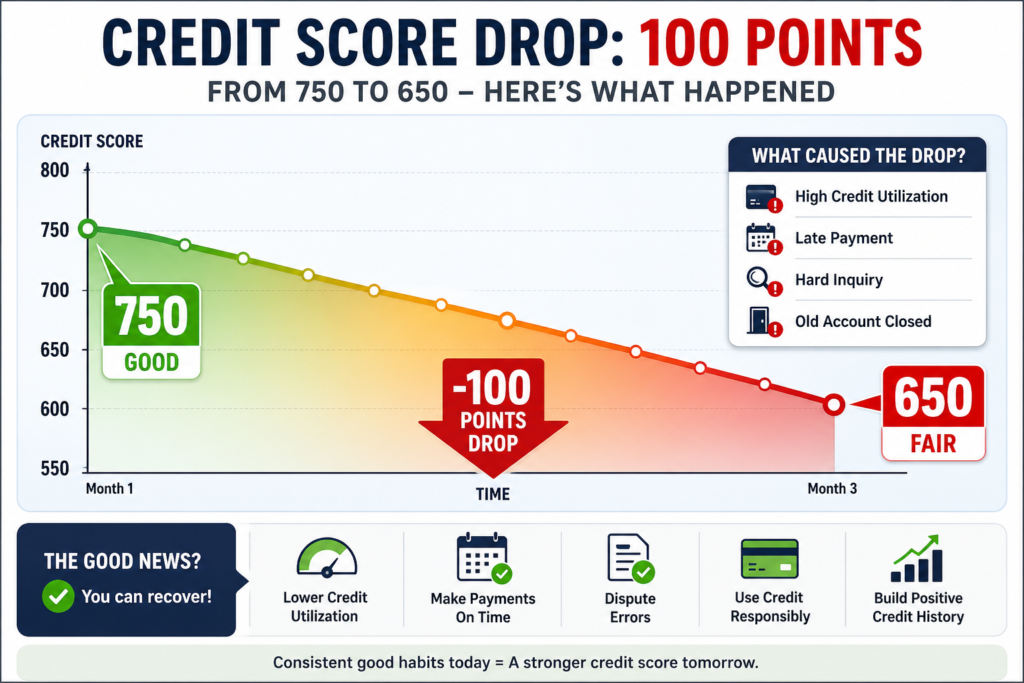

You wake up, check your credit score… and it’s down by 100 points.

No warning. No explanation. Just damage.

Suddenly:

- Your loan gets rejected

- Your credit card limit drops

- Your interest rates go up

And the worst part? You don’t even know what went wrong.

I’ve seen this happen to people who were doing “everything right.”

Here’s the truth — a 100-point drop is serious, but it’s NOT permanent.

And if you act smartly, you can recover faster than most people think.

Quick Answer Box

To recover a 100-point credit score drop:

- Identify the exact cause (late payment, utilization, hard inquiry, account closure)

- Reduce credit utilization below 30% (ideally 10%)

- Dispute errors on your credit report immediately

- Make all payments on time (no exceptions)

- Add positive credit (secured card or credit builder account)

- Avoid new hard inquiries for 60–90 days

Recovery time:

- Minor issue: 30–45 days

- Major issue: 3–6 months

Why This Problem Happens (Real Reasons)

Let’s be honest — credit score doesn’t drop randomly.

There’s ALWAYS a trigger.

1. Late Payment (Biggest Killer)

Even a single 30-day late payment can drop your score by 80–110 points.

Banks don’t care about your history. They care about recent behavior.

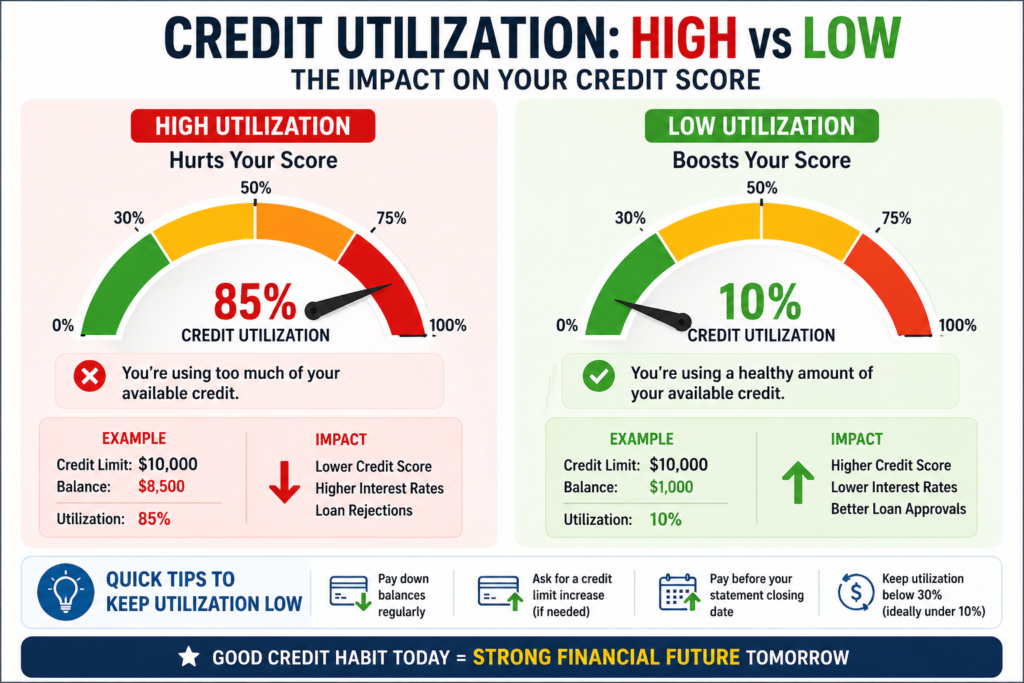

2. Credit Utilization Spike

If your credit card usage suddenly goes from:

- 20% → 80%

Your score can crash instantly.

This is one of the most common hidden reasons.

3. Hard Inquiries

Applying for multiple loans or credit cards in a short time = red flag.

Lenders see you as desperate for credit.

4. Account Closure

Closing an old credit card reduces:

- Your total credit limit

- Your credit history length

Both hurt your score.

5. Errors on Credit Report

This is more common than you think.

Wrong late payment. Duplicate account. Fraud.

And boom — your score drops.

Step-by-Step Solution (Real-World Fix)

Now let’s fix it properly.

Step 1: Check Your Credit Report (Immediately)

Use platforms like:

- Experian

- Equifax

- TransUnion

Look for:

- Late payments

- Incorrect balances

- Unknown accounts

Step 2: Fix Credit Utilization FAST

This is your quickest win.

If your card is maxed out:

- Pay it down below 30%

- Ideally below 10%

This alone can recover 20–40 points in weeks.

Step 3: Dispute Errors (If Any)

If you find something wrong:

- File dispute online

- Provide proof

- Follow up aggressively

Banks don’t fix things unless you push.

Step 4: Make Payments Perfectly On Time

No delay. Not even 1 day.

Set:

- Auto-pay

- Reminders

Your score rebuild depends on consistency.

Step 5: Add Positive Credit

If your profile got weak:

- Use a secured credit card

- Use credit builder apps

This adds fresh positive data.

Step 6: Stop Applying for Credit Temporarily

Give your profile time to stabilize.

Avoid:

- Loan applications

- Credit card applications

At least for 60–90 days.

ADVANCED RECOVERY STRATEGIES (MOST PEOPLE DON’T KNOW THIS)

1. The “Credit Limit Boost Hack” (Fast Score Jump)

If your score dropped due to high utilization, here’s a smart move:

Call your credit card issuer and ask for a credit limit increase WITHOUT a hard inquiry.

Why this works:

- Same balance

- Higher limit

- Lower utilization instantly

Example:

- Before: $4,000 balance / $5,000 limit = 80% utilization

- After: $4,000 / $10,000 = 40% utilization

Score impact: +20 to +50 points possible

2. Become an Authorized User (Fastest Hidden Trick)

If someone you trust has:

- Old credit card

- Perfect payment history

- Low utilization

Ask to be added as an authorized user.

What happens:

- Their positive history reflects on your report

This can boost your score within 30–45 days

3. The “Statement Date Strategy”

Most people don’t know this:

Your credit utilization is reported before your due date, not after.

So even if you pay on time, high usage can still hurt you.

Fix:

- Pay your card BEFORE statement date

- Keep reported balance low

This is a game-changing tactic

4. Remove Small Negative Accounts (Negotiation Method)

If you have:

- Collections

- Small unpaid accounts

Call the creditor and ask for:

- “Pay for delete”

Meaning:

- You pay

- They remove it from report

Not guaranteed, but works in many cases.

5. Use Multiple Small Payments (Score Optimization Trick)

Instead of paying once a month:

- Pay weekly or bi-weekly

This keeps your balance consistently low → improves score stability

CREDIT SCORE RECOVERY TIMELINE (REALISTIC)

| Action Taken | Timeline | Expected Impact |

|---|---|---|

| Reduce utilization | 7–30 days | Fast boost |

| Dispute errors | 30–60 days | High boost |

| On-time payments | 2–4 months | Strong recovery |

| Add secured card | 2–3 months | Moderate boost |

| Remove negatives | 1–3 months | Huge impact |

WHAT IF YOUR SCORE IS NOT IMPROVING?

This is where most people get stuck.

Possible Reasons:

1. You Fixed One Problem, Not All

Example:

- Reduced utilization

BUT - Still have late payment

Result: No major improvement

2. Credit Profile Too Thin

If you have:

- Only 1 account

- No history

Your score won’t grow fast

Fix:

- Add 1–2 more accounts (smartly)

3. Negative Mark Still Active

Late payments stay for up to 7 years.

But impact reduces over time.

4. You’re Applying Too Often

Too many applications = score stagnation

LENDER PSYCHOLOGY BREAKDOWN (VERY IMPORTANT)

Banks classify you into 3 types:

1. Stable Borrower

- Low usage

- Consistent payments

→ Best rates, easy approvals

2. Risky Borrower

- High usage

- Recent drop

→ Higher interest rates

3. Desperate Borrower

- Multiple applications

- Missed payments

→ Immediate rejection

Your goal:

Move back to Stable Borrower category

EXTRA MISTAKES THAT DESTROY RECOVERY

- Paying only minimum dues

- Ignoring old accounts

- Using BNPL excessively

- Taking payday loans

- Closing oldest credit card

MAINTAINMARKET TESTED STRATEGY (PRACTICAL FRAMEWORK)

If your score dropped 100 points, follow this exact system:

Phase 1 (First 7 Days)

- Identify issue

- Pay down balances

- Stop all applications

Phase 2 (Next 30 Days)

- Fix utilization

- Dispute errors

- Start auto-pay

Phase 3 (Next 90 Days)

- Build positive credit

- Maintain low usage

- Avoid risky behavior

Phase 4 (Long-Term)

- Keep utilization under 30%

- Maintain 100% payment history

- Use credit strategically

Insider Insights (How Lenders Actually Think)

Here’s what most people don’t understand:

Banks don’t just look at your score.

They look at your behavior pattern.

If they see:

- Sudden high usage

- Multiple inquiries

- Payment inconsistency

They assume:

“This person is becoming risky.”

Even if your score looks decent.

That’s why fixing behavior matters more than just numbers.

Real-Life Case Study (USA)

John (Texas)

- Credit Score: 742 → 638 (lost 104 points)

- Reason: Missed 1 payment + high credit usage

What he did:

- Paid down credit cards from 78% → 18%

- Set auto-pay

- Disputed one incorrect late payment

Results:

- 45 days: +38 points

- 90 days: +72 points

- 5 months: back to 720+

Lesson: Recovery is possible if you act fast.

Comparison Table (Best Recovery Methods)

| Strategy | Speed | Impact | Difficulty |

|---|---|---|---|

| Reduce utilization | Fast | High | Easy |

| Fix errors | Medium | High | Medium |

| On-time payments | Slow | Very High | Easy |

| Add secured credit | Medium | Medium | Easy |

| Avoid inquiries | Medium | Medium | Easy |

Mistakes People Make

- Ignoring the drop

- Applying for more loans

- Closing credit cards

- Paying minimum balance only

- Not checking credit report

These mistakes make recovery slower.

MaintainMarket Expert Advice

If your score dropped 100 points, don’t panic — but don’t ignore it either.

Focus on 3 things only:

- Utilization

- Payment behavior

- Credit report accuracy

Forget everything else.

That’s how real recovery happens.

Why MaintainMarket is Different

Most websites give textbook advice.

We focus on:

- Real financial behavior

- Lender psychology

- Practical recovery steps

No theory. Just what works in real life.

Action Plan (Do This Now)

Today:

- Check your credit report

- Identify the cause

Next 7 days:

- Reduce credit usage

- Fix any errors

Next 30 days:

- Maintain perfect payments

- Avoid new credit

Next 90 days:

- Add positive credit if needed

Conclusion

A 100-point drop feels like a financial disaster.

But it’s actually a signal.

It’s telling you something changed — and you need to fix it fast.

If you follow the right steps, you won’t just recover…

You’ll come back stronger.

FAQs – How to Recover 100 Point Credit Score Drop

Q1. Can a credit score drop 100 points in one day?

Yes. Late payments or high utilization can cause instant drops.

Q2. How long does it take to recover 100 points?

Usually 3–6 months depending on the issue.

Q3. Can I fix my credit score in 30 days?

Partial recovery is possible, full recovery takes longer.

Q4. Does paying off debt increase score immediately?

Yes, especially if utilization was high.

Q5. Should I close unused credit cards?

No, it can reduce your score.

Q6. Can errors cause big drops?

Yes, and they are fixable.

Q7. How many points does a late payment drop?

Typically 80–110 points.

Q8. Is credit repair company worth it?

Only if you don’t want to handle disputes yourself.

People searched for: 15 Best Side Hustles From Home USA (Earn $1000+/Month) – Real Guide 2026

Also read: 10 Safest Investment with High Returns in USA 2026 – Low Risk Options Ranked by Stability

500 Credit Score? Get a Credit Card Approval in the USA (2026 Hidden Tricks Banks Don’t Tell You)

5 thoughts on “How to Recover 100 Point Credit Score Drop Fast – Hacks Banks Won’t Tell You”