Struggling with a 500 credit score? Learn real strategies to get approved for a loan even after rejection. Proven methods, lenders, and fixes explained. Let’s talk about How to Get a Loan with 500 Credit Score.

Before you apply again, do one thing:

Check lenders that allow pre-qualification without hurting your score.

Because the difference between:

- Rejection

and - Approval

Is not your credit score alone —

it’s how you apply.

Introduction

Let’s be honest.

If your credit score is around 500, you already know how frustrating it is.

You apply for a loan → instant rejection.

You try another lender → same result.

At some point, it starts feeling like the system is designed against you.

But here’s the truth most blogs won’t tell you:

You CAN still get a loan with a 500 credit score — but not the way you’re trying right now.

And if you keep applying blindly, you’ll actually make your situation worse.

This guide is not theory.

This is exactly how people in the US are still getting approved — even after multiple rejections.

Quick Answer Box

Can you get a loan with a 500 credit score?

Yes, but only through:

- Secured loans (with collateral)

- Bad credit lenders (higher interest)

- Co-signer-based loans

- Credit union programs

- Payday or emergency lenders (last option)

Best strategy:

Fix 2–3 key factors first → then apply smartly → not everywhere.

Why This Problem Happens (Real Reasons)

Let’s cut the nonsense.

Banks don’t reject you because they hate you.

They reject you because you look risky on paper.

Here’s what they actually see:

1. Missed Payments

Even 1–2 missed EMIs can crash your score.

2. High Credit Utilization

Using 80–90% of your credit card? Huge red flag.

3. Too Many Applications

Every application = hard inquiry = score drops further.

4. No Credit Mix

Only credit cards, no loans? Weak profile.

5. Collections / Defaults

This is where lenders completely lose trust.

Step-by-Step Solution (What Actually Works)

Step 1: Stop Applying Everywhere

This is your biggest mistake.

Every rejection:

- Drops your score

- Makes lenders more suspicious

Rule: No more than 1–2 applications in 30 days.

Step 2: Fix Credit Utilization (Fast Win)

If your credit card is maxed out:

- Pay it down to below 30%

- Ideal: below 10%

This alone can increase your score in 30–45 days.

Step 3: Use Secured Loan Strategy

If no one trusts you — give them security.

Options:

- Car title loan

- FD-backed loan

- Gold loan (India angle)

Why this works:

- Lender risk = low

- Approval chances = high

Step 4: Use a Co-Signer

This is the most underrated strategy.

If someone with good credit co-signs:

- You get approval

- You get better interest rate

Step 5: Target the RIGHT Lenders

Stop applying to big banks.

They don’t want risk.

Instead:

- Online bad credit lenders

- Credit unions

- Peer-to-peer platforms

Insider Insight (How Lenders Think)

Here’s something most people don’t understand:

Lenders don’t care about your past.

They care about your probability of repayment.

They look at:

- Income stability

- Recent behavior (last 3 months)

- Debt-to-income ratio

So even with 500 score, if:

- You have stable income

- Low current debt

You can still get approved.

Real-Life Case Study (USA)

Name: Jake (Texas)

Score: 512

Problem: 3 rejections from banks

What he did:

- Paid down credit card from 85% → 25%

- Waited 30 days

- Applied through bad credit lender

- Added co-signer

Result:

- Approved for $5,000 loan

- Interest: 18% (high, but manageable)

Lesson:

Preparation matters more than score.

Hidden Ways People Still Get Loan with 500 Credit Score

Most articles stop at “try bad credit lenders.”

That’s lazy advice.

Here are methods people actually use when they’re stuck:

1. Pre-Qualification Trick (Zero Risk Strategy)

Most people don’t know this.

Some lenders allow soft check pre-qualification.

Meaning:

- No impact on your credit score

- You see approval chances before applying

Why this matters:

If you apply blindly → rejection → score drops → worse situation

Smart move:

Only apply where you’re pre-qualified

2. Income Stacking Strategy (Game Changer)

Lenders don’t just look at credit score.

They look at income consistency.

If your salary is low, you can:

- Add freelance income

- Add side income (Uber, gigs, online work)

Even an extra $300–$500/month can:

- Increase approval chances

- Reduce perceived risk

This is how many “low score” borrowers still get approved.

3. Debt-to-Income (DTI) Optimization

This is something almost nobody talks about.

Even with a 500 score:

If your DTI is low → approval chances go UP

Example:

| Scenario | Result |

|---|---|

| High income + low debt | Higher approval |

| Low income + high debt | Almost guaranteed rejection |

Target:

Keep DTI below 40%

4. Apply Right After Score Update

Timing matters more than people think.

If you:

- Pay down credit card

- Clear one EMI

Your score updates in 30–45 days

Apply RIGHT after that update.

That’s your best approval window

5. Use Smaller Loan First (Build Trust)

Stop trying for big loans.

That’s why you’re getting rejected.

Instead:

- Apply for $500–$1000 loan

- Repay on time

This builds:

- Credit history

- Trust with lenders

Then go for bigger loans.

BEST TYPES OF LOANS FOR 500 CREDIT SCORE (DETAILED BREAKDOWN)

Secured Personal Loans

- Backed by collateral

- Much higher approval chances

- Lower interest than bad credit loans

Best for:

People who have assets but low score

Also read: Credit Score 580? Personal Loan Approval Blueprint – USA (Step-by-Step Guide)

Credit Builder Loans

This is underrated.

How it works:

- You don’t get money upfront

- You pay monthly

- At end, you receive the amount

Benefit:

- Builds credit score fast

- Improves future approvals

Bad Credit Personal Loans

These are designed for people like you.

But:

- Interest rates can be 20–35%

- Terms are strict

Use only if:

You really need money urgently

Payday Loans (Reality Check)

Yes, they approve easily.

But here’s the truth:

- Interest can go 300%+ annually

- Can trap you in debt cycle

Only use if:

No other option exists

HOW TO INCREASE APPROVAL CHANCES (CHECKLIST)

Before applying, make sure:

- Credit utilization below 30%

- No recent missed payments (last 30 days clean)

- Stable income proof ready

- Only 1–2 recent inquiries

- Correct errors in credit report

If you ignore this → rejection probability shoots up.

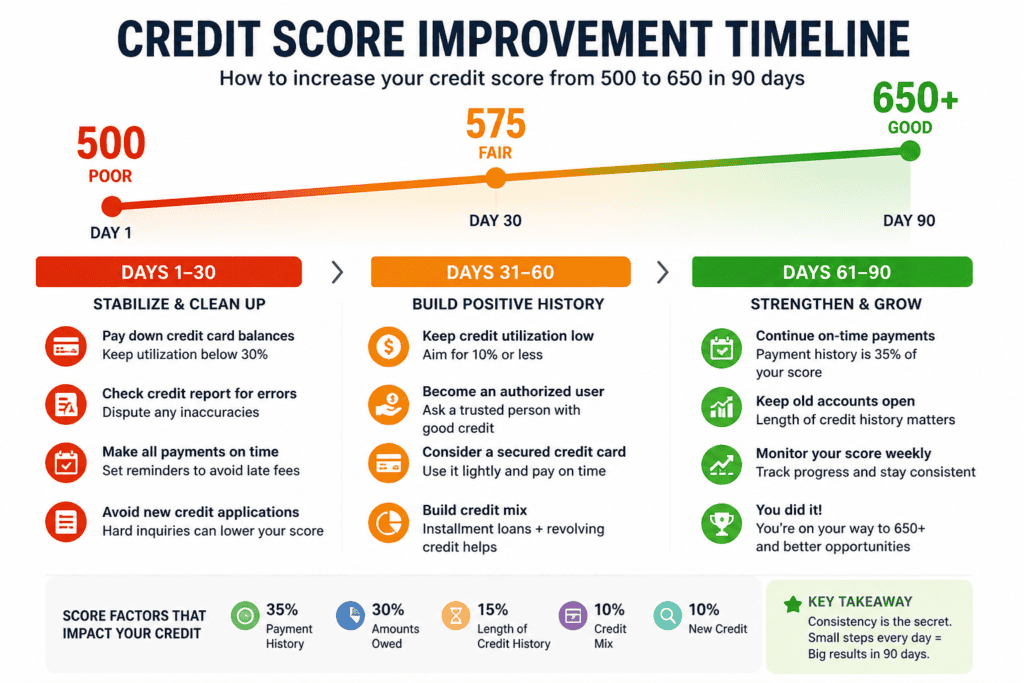

CREDIT SCORE RECOVERY PLAN (90-DAY STRATEGY)

This is where real transformation happens.

Month 1:

- Pay down credit card

- Stop all new applications

- Check credit report errors

Month 2:

- Keep utilization low

- Make all payments on time

- Add small secured credit line

Month 3:

- Score improves (usually +50 to +100 points)

- Apply strategically

This is how people move from:

500 → 600+ → approval unlocked

PSYCHOLOGY OF REJECTION (IMPORTANT)

After 2–3 rejections, people panic.

They:

- Apply everywhere

- Take bad loans

- Accept horrible terms

This is exactly what lenders expect.

Why?

Because desperate borrowers:

- Accept higher interest

- Become profitable customers

You need to stay strategic, not emotional.

ALTERNATIVE OPTIONS (IF LOAN IS NOT URGENT)

If you don’t need money immediately:

1. Credit Builder Cards

- Easy approval

- Improves score

2. Secured Credit Cards

- Deposit-based

- Safe and effective

3. Borrow from Credit Union

- Lower rates

- More flexible approval

RED FLAGS (AVOID THESE SCAMS)

When you’re desperate, scams increase.

Avoid lenders who:

- Ask upfront fees before approval

- Guarantee approval without checks

- Don’t have proper website or reviews

Golden rule:

Real lenders never ask money before giving loan

Also read: Credit Score Not Improving? Fix It Fast (2026 Guide)

ADVANCED COMPARISON (REAL DECISION TABLE)

| Strategy | Speed | Cost | Approval Rate | Best Use Case |

|---|---|---|---|---|

| Pre-qualification | Fast | Free | High | Safe application |

| Secured loan | Medium | Low | Very High | Asset owners |

| Co-signer | Medium | Medium | High | Better rates |

| Payday loan | Instant | Very High | Very High | Emergency only |

| Credit builder | Slow | Low | Guaranteed | Long-term fix |

Comparison Table – Loan with 500 Credit Score

| Option | Approval Chance | Interest Rate | Risk Level | Best For |

|---|---|---|---|---|

| Secured Loan | High | Low–Medium | Low | Fast approval |

| Bad Credit Lenders | Medium | High | Medium | Emergency |

| Co-Signer Loan | High | Medium | Low | Better rates |

| Payday Loan | Very High | Very High | Very High | Last resort |

| Credit Union | Medium | Low | Low | Safe borrowing |

Mistakes People Make

- Applying to 10+ lenders at once

- Ignoring credit utilization

- Taking payday loans blindly

- Not checking credit report errors

- Applying without income proof

MaintainMarket Expert Advice

If your score is 500:

Don’t chase approval.

Build approval conditions.

Focus on:

- Lowering utilization

- Stabilizing income proof

- Applying strategically

That’s the difference between rejection and approval.

Why MaintainMarket is Different

Most sites:

- Tell you “try lenders”

- Give generic advice

We:

- Show real strategies

- Explain lender psychology

- Focus on results, not theory

Action Plan (Do This Now)

- Check your credit report

- Pay down credit card below 30%

- Stop applying randomly

- Wait 30–45 days

- Apply with:

- secured loan OR

- co-signer OR

- bad credit lender

Conclusion

A 500 credit score is not the end.

But if you keep making the same mistakes —

it will feel like one.

The difference is simple:

Desperate applications vs smart strategy.

Choose wisely.

FAQs

Q1. Can I get a loan instantly with 500 score?

Yes, but mostly high-interest lenders.

Q2. What is the easiest loan to get?

Secured loans or payday loans.

Q3. Will my score improve after loan?

Yes, if you repay on time.

Q4. How long to improve from 500 to 650?

Usually 3–6 months with discipline.

Q5. Do all lenders check credit score?

Most do, but some focus on income.

Q6. Is payday loan safe?

Only for emergency — very high interest.

Q7. Can I get loan without job?

Very difficult unless collateral exists

Q8. Does checking my score reduce it?

No (soft Inquiry)

People searched for: How to Recover 100 Point Credit Score Drop Fast – Hacks Banks Won’t Tell You

Alos read: Why FICO Score Dropped After Paying Off Loan (Fix Fast 2026)

You Earn Well But Still Got Rejected? 5 Hidden Reasons Banks Won’t Approve Your Loan USA

1 thought on “How to Get a Loan with 500 Credit Score (Guaranteed Best Options 2026) – USA”