Struggling with a 300–580 credit score? Discover credit cards that still approve you fast, how to qualify, and the exact strategy to rebuild your credit quickly. Let’s talk about the best credit cards for Bad Credit USA (300–580).

“Check your eligibility for this card here — it takes less than 60 seconds and doesn’t affect your credit score.”

Introduction

If your credit score is sitting somewhere between 300 and 580, you already know the feeling.

You apply → get rejected.

Try another → rejected again.

At some point, it starts feeling like the system is just closed for you.

Here’s the truth most websites won’t tell you:

Banks are not rejecting you randomly. They’re rejecting you predictably.

And once you understand that, getting approved becomes much easier.

This guide is not going to list random cards.

I’ll show you:

- Why you’re getting rejected

- Which cards actually approve bad credit

- And how to force approval strategically

Quick Answer Box

Best credit cards for very bad credit (300–580):

- Capital One Secured Mastercard

- Discover it® Secured Credit Card

- OpenSky Secured Visa

- Self Credit Builder Card

Best strategy:

Start with a secured card → use under 10% limit → pay on time → upgrade in 6 months.

Why You Keep Getting Rejected (Real Reasons)

Let’s be honest — it’s not just your score.

1. You look risky to lenders

Banks don’t see your “potential.”

They see patterns:

- Late payments

- High credit usage

- Collections

- No recent activity

That screams: “High chance of default.”

2. You’re applying for the wrong cards

This is the biggest mistake.

You’re applying for cards meant for:

- 650+ credit score

- Stable history

- Low utilization users

So rejection is guaranteed.

3. Too many applications (silent killer)

Every application = hard inquiry

Too many = desperation signal.

Banks think:

“This person is being rejected everywhere.”

Step-by-Step: How to Get Approved (Even With 300 Score)

Step 1: Stop applying randomly

Pause everything.

Every wrong application is hurting you.

Step 2: Go for secured cards ONLY

If your score is below 580, don’t fight reality.

Secured cards = your entry point

You deposit money → bank takes zero risk → approval chances shoot up.

Step 3: Apply to THESE specific cards

1. Capital One Secured Mastercard

Why it works:

- Low deposit (as low as $49)

- Reports to all 3 bureaus

- High approval rate

2. Discover it® Secured Card

Why it works:

- Cashback rewards (rare for bad credit)

- Upgrade possible in 7 months

- No annual fee

3. OpenSky Secured Visa

Why it works:

- No credit check

- Almost guaranteed approval

- Perfect for 300–450 scores

4. Self Credit Builder Card

Why it works:

- Builds credit + savings

- Ideal if you’ve been rejected everywhere

Also read: How to Recover 100 Point Credit Score Drop Fast – Hacks Banks Won’t Tell You

Hidden Approval Hacks (Almost No One Talks About)

This is where most people lose.

1. Apply right after paycheck hits your account

Banks sometimes check your banking activity (soft signals).

More balance = more trust.

2. Choose lower deposit first

If you try $1000 deposit:

→ looks like desperation

Start with:

→ $200–$300

Looks more “normal behavior”

3. Use pre-qualification tools first

Cards like:

- Capital One

- Discover

Let you check eligibility without hurting your score.

This alone can save 20–40 points.

4. Avoid weekend applications

Sounds weird, but real:

- Automated systems dominate weekends

- Less human review

Weekdays = slightly better outcomes

Psychology of Lenders (This Changes Everything)

Let’s simplify how lenders think:

They are not asking:

“Can this person improve?”

They are asking:

“Will I lose money?”

So they check:

- Recent activity (last 90 days matters most)

- Payment behavior (even 1 late = huge red flag)

- Utilization pattern (not just current %)

Key insight:

Consistency beats everything.

Even with bad history:

→ 3 months clean behavior = major trust boost

Advanced Strategy: The “2 Card Method”

Once you get your first secured card:

After 60–90 days:

Apply for second secured card (only if score improves slightly)

Why?

- Improves credit mix

- Increases total limit

- Lowers utilization %

Example:

| Card | Limit | Usage |

|---|---|---|

| Card 1 | $200 | $20 |

| Card 2 | $300 | $20 |

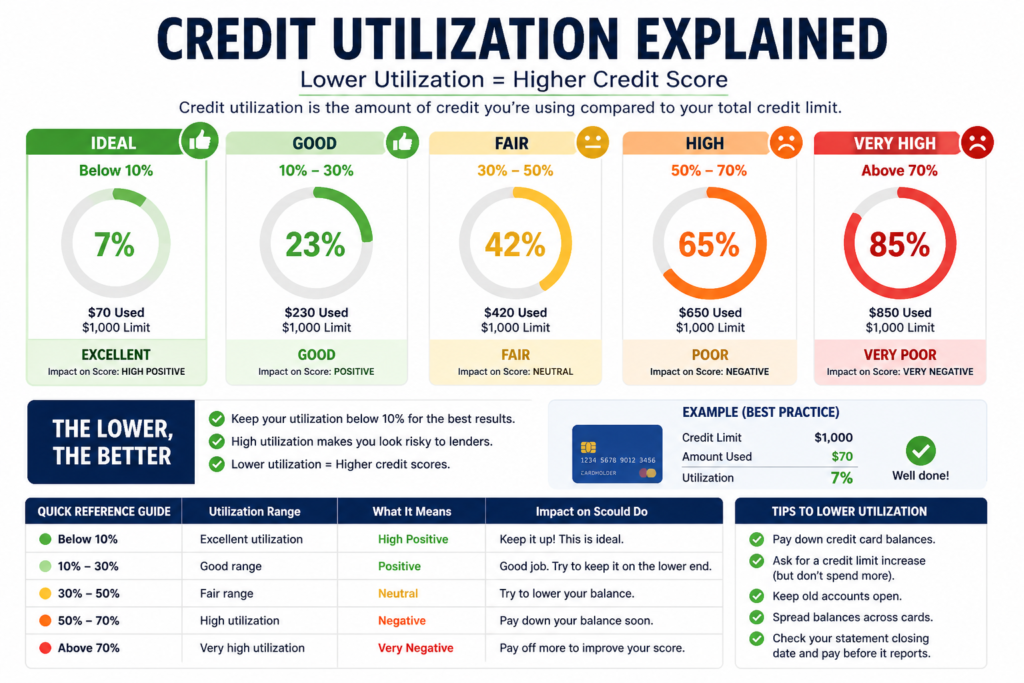

Total usage = $40 / $500 = 8% utilization

That’s powerful.

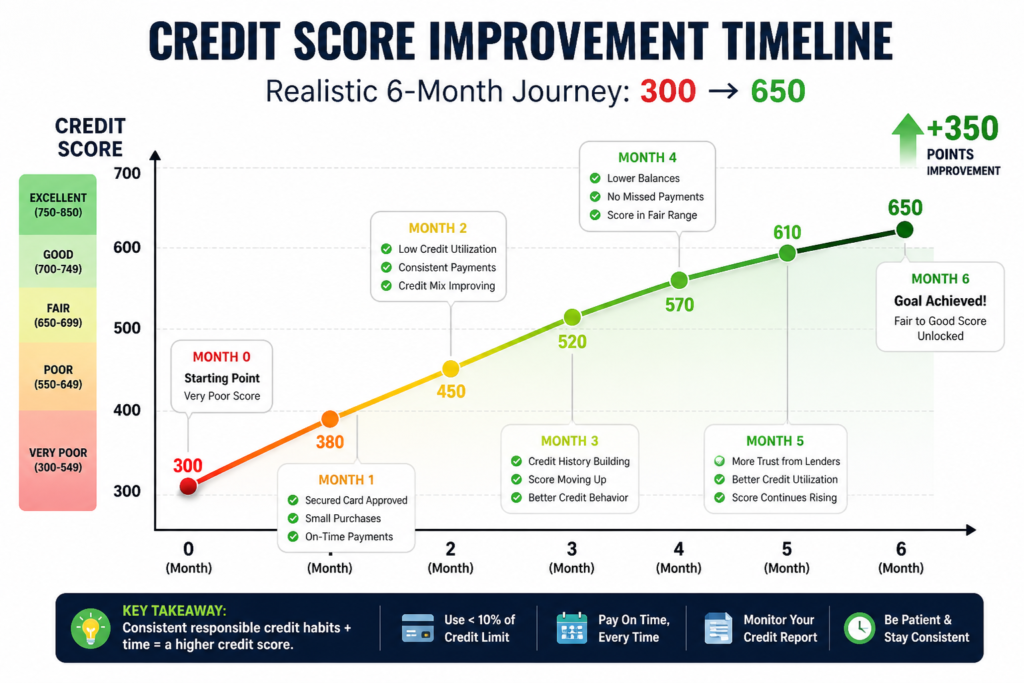

Timeline Breakdown (What Happens Each Month)

Month 1:

- Approval

- First usage

- No score jump yet

Month 2–3:

- Payment history builds

- Score increases slightly (20–40 points)

Month 4–5:

- Utilization impact kicks in

- Bigger jump (40–80 points)

Month 6:

- Lenders start trusting again

- Pre-approval offers begin

Also read: Credit Score Not Improving? Fix It Fast (2026 Guide)

Credit Report Errors (Hidden Opportunity)

Here’s something most people ignore:

1 in 5 Americans has an error in their credit report

Common errors:

- Wrong late payment

- Duplicate accounts

- Incorrect balance

- Closed accounts showing open

Fixing this can boost score by:

→ 50–100 points instantly

Use:

- Experian

- Equifax

- TransUnion

What to Do If You Still Get Rejected

Don’t panic — do this:

Step 1: Wait 30 days

Avoid stacking rejections

Step 2: Switch to no-credit-check card

Go for:

- OpenSky

Step 3: Reduce utilization to zero

If you already have any card:

→ pay it down fully

Step 4: Try again strategically

Secured vs Unsecured (Reality Check)

| Feature | Secured | Unsecured |

|---|---|---|

| Approval | Very High | Low |

| Deposit | Required | No |

| Risk to bank | Zero | High |

| Best for | Bad credit | Good credit |

Truth:

If your score is below 580,

secured is not optional — it’s mandatory.

Long-Term Strategy (What Happens After 6 Months)

This is where money starts.

Step 1: Upgrade your card

Example:

- Discover often upgrades automatically

Step 2: Apply for unsecured card

Now you can target:

- Cashback cards

- No annual fee cards

Step 3: Increase limits

Higher limits = lower utilization = higher score

Pro Tip: The 10% Rule (Game Changer)

If your limit is $200:

Don’t use $150

Don’t use $100

Use:

→ $10–$20 max

This single trick:

→ Can boost your score faster than anything else

Best Beginner Option:

Capital One Secured Card

→ Best balance of approval + upgrade

No Credit Check Option:

OpenSky

→ Highest approval probability

Best Rewards Option:

Discover

→ Cashback even for bad credit

Insider Insight: How Banks Actually Think

This is where most articles fail.

Banks don’t care about your story.

They care about risk vs control.

Secured cards work because:

- You give them money upfront

- They control your limit

- They monitor behavior

Once you prove discipline → they trust you again.

Real-Life Case Study (USA)

Name: Jason (Texas)

Score: 512

Problem: 3 rejections + collections

What he did:

- Got OpenSky secured card ($200 deposit)

- Used only $20–$30 monthly

- Paid full balance

Result (6 months):

- Score: 512 → 645

- Approved for unsecured card later

Key takeaway:

Low usage + consistency = fast recovery

Comparison Table

| Card | Approval Difficulty | Deposit | Credit Check | Upgrade Possible |

|---|---|---|---|---|

| Capital One Secured | Easy | $49–$200 | Yes | Yes |

| Discover Secured | Easy | $200 | Yes | Yes |

| OpenSky Secured | Very Easy | $200 | No | Limited |

| Self Credit Builder | Easy | Varies | Soft | Yes |

Mistakes People Make

- Applying for 5+ cards at once

- Using 80–90% credit limit

- Missing even 1 payment

- Closing card too early

- Ignoring credit report errors

MaintainMarket Expert Advice

If your score is under 580:

Don’t chase rewards.

Don’t chase fancy cards.

Chase approval + discipline.

Your goal is simple:

- Get approved

- Build trust

- Upgrade later

Why MaintainMarket is Different

Most sites:

- List random cards

- Focus on rewards

- Ignore approval reality

MaintainMarket:

- Focuses on real approval chances

- Explains lender psychology

- Gives action-based strategy

Action Plan (Do This Now)

- Check your score

- Choose ONE secured card

- Deposit minimum required

- Use less than 10% limit

- Pay full before due date

- Repeat for 6 months

- Apply for upgrade

Conclusion

You’re not stuck.

You’re just playing the wrong game.

Once you switch to the secured strategy, approval becomes predictable.

And once you get that first approval, everything changes.

FAQs

Q1. Can I get a credit card with 300 score?

Yes, but only secured cards or no-credit-check options.

Q2. Which card is easiest to get approved?

OpenSky Secured Visa.

Q3. How fast can I improve my score?

3–6 months with disciplined usage.

Q4. Do secured cards build credit?

Yes, they report to major bureaus.

Q5. Is deposit refundable?

Yes, if you close in good standing.

Q6. Should I apply for multiple cards?

No. One is enough.

Q7. What utilization is best?

Below 10%.

Q8. Can I upgrade to unsecured?

Yes, usually after 6–12 months.

Q9. Can I get approved after bankruptcy?

Yes, secured cards are designed for this.

Q10. How many points can I gain in 30 days?

Typically 20–50 points (if no errors).

Q11. Does checking eligibility hurt score?

No (soft inquiry).

Q12. Should I close secured card later?

Only after upgrading.

FINAL INSIGHT (IMPORTANT)

People with 300–580 score fail because:

They try to “skip the process”

But the system works like this:

Step 1: Secured → Step 2: Discipline → Step 3: Trust → Step 4: Upgrade

There’s no shortcut.

But there is a clear path.

People searched for: How to Recover 100 Point Credit Score Drop Fast – Hacks Banks Won’t Tell You

2 thoughts on “Best Credit Cards for Bad Credit USA (300–580) That Actually Approve You in 2026”