Loan approved but money not credited? Discover real reasons, hidden bank checks, and how to speed up disbursement in the USA (with India comparison). In this article, let’s talk about Loan Approved but Not Disbursed.

You got the message: “Your loan is approved.”

For a moment, everything felt sorted.

Bills? Covered. Emergency? Handled. Plans? Back on track.

But then…

No money hits your account.

One day passes. Then three. Then a week.

Now you’re stuck thinking:

- “Did something go wrong?”

- “Did they cancel my loan?”

- “Is this normal or am I being scammed?”

Here’s the truth most banks won’t clearly tell you:

Loan approval does NOT mean money is guaranteed yet.

There’s a hidden gap between approval and disbursement — and that’s where most people get stuck.

Let’s break it down properly.

Quick Answer (Featured Snippet Ready)

A personal loan can be approved but not disbursed due to pending verification, underwriting checks, document issues, employer validation, fraud checks, or internal bank delays.

To fix it fast:

- Complete all document requests immediately

- Confirm bank account verification

- Respond to lender calls/emails

- Check for “final approval” vs “conditional approval”

- Follow up with lender support directly

Why This Happens (Real Reasons – Not Textbook)

Let’s be honest — banks don’t delay randomly.

They delay because they still don’t fully trust the risk.

Here are the real reasons:

1. You Got “Conditional Approval” (Not Final)

This is the biggest trap.

Banks often approve loans like this:

“Approved, subject to verification”

Which means:

- Income not fully verified

- Documents still under review

- Risk profile not finalized

Until that clears → no disbursement

2. Income or Employment Verification Pending

Especially in the USA:

- Lenders may call your employer

- Cross-check income via databases

- Verify tax returns

If something doesn’t match → delay.

3. Bank Account Verification Failed

Even small issues can stop disbursement:

- Wrong account number

- Name mismatch

- Micro-deposit verification pending

No verified account = no money.

4. Fraud & Risk Checks (Silent but Powerful)

Banks run hidden checks like:

- Identity fraud detection

- Duplicate applications

- Suspicious activity flags

If flagged → your loan gets “paused”

5. Credit Score Change After Approval

Yes, this happens.

If:

- Your score drops suddenly

- You take another loan

- Credit utilization spikes

Bank may hold or cancel disbursement.

6. Internal Bank Delays

Not everything is your fault.

Sometimes:

- Weekend/holiday processing

- Backend errors

- Manual approvals pending

7. Missing Final Agreement / E-Sign

Many borrowers forget this step.

Until you:

- Sign loan agreement

- Accept final terms

Money won’t move.

8. Debt-to-Income (DTI) Ratio Recalculation

Even after approval, lenders may recalculate your DTI before disbursement.

If during that time:

- You used your credit card heavily

- Took another EMI

- Your balance increased

Your DTI worsens → loan gets paused

USA Insight:

DTI is taken VERY seriously (usually must stay below 36–43%)

India Comparison:

More flexible, especially with NBFCs

9. Soft Approval via Pre-Qualification

Many users confuse this.

You might have received:

- “Pre-approved”

- “Pre-qualified”

This is NOT actual approval.

It’s just:

“You may qualify — but we haven’t checked fully yet.”

Disbursement won’t happen until:

- Hard credit pull

- Full underwriting

10. Loan Sold to Another Lender (Backend Transfer)

In the USA, this is common.

Your loan may be:

- Approved by platform (like aggregator)

- Then transferred to partner lender

During this transition:

- Files are rechecked

- Approval may get delayed

11. Compliance & Regulatory Checks

Banks must follow strict regulations.

Sometimes delays happen due to:

- KYC/AML checks (Anti-Money Laundering)

- Identity validation

- Address mismatch

If flagged → manual review → delay

12. System Triggered Risk Flags

Modern lenders use AI systems.

Triggers include:

- Multiple loan applications in short time

- Unusual income pattern

- Location mismatch (IP vs address)

Even small things can freeze disbursement.

Psychological Mistake Borrowers Make (Very Important)

Most people think:

“Loan approved = money guaranteed”

Wrong.

Banks think like this:

“We approved you based on probability — now we VERIFY reality”

That’s why delays happen.

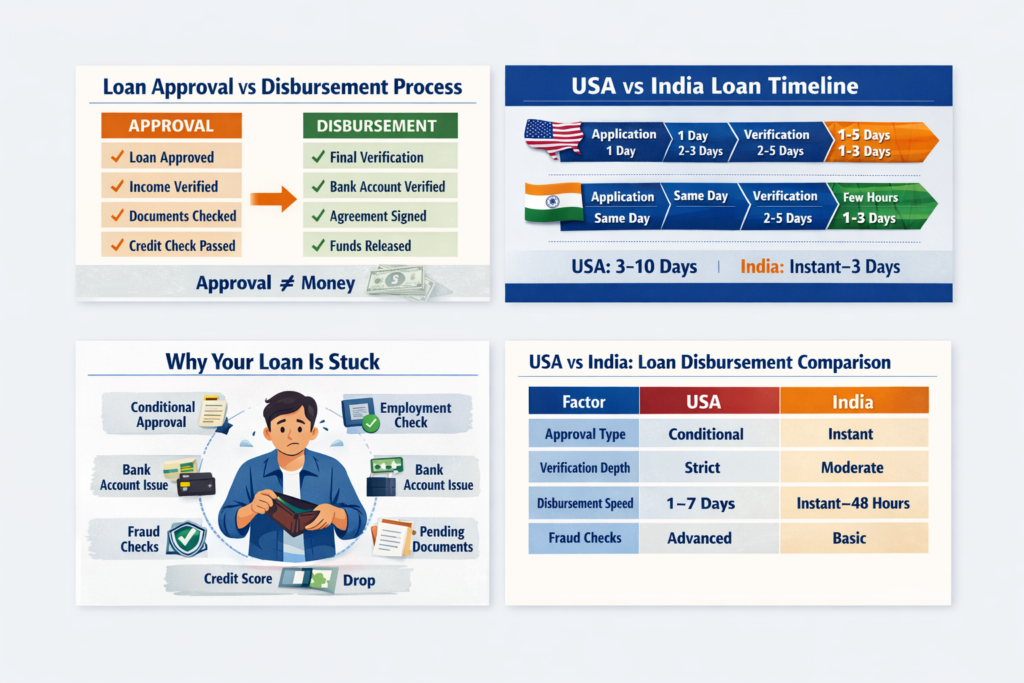

Exact Timeline Breakdown (USA vs India)

| Stage | USA Timeline | India Timeline |

|---|---|---|

| Application | Same day | Same day |

| Approval | 1–3 days | Instant–24 hrs |

| Verification | 2–5 days | Few hours–2 days |

| Disbursement | 1–3 days | Instant–24 hrs |

Total Time:

- USA: 3–10 days

- India: Instant – 3 days

Advanced Fix Strategy (Most Powerful Section)

If your loan is stuck, use this 3-Level Strategy:

Level 1: Passive Fix (Basic)

- Upload documents

- Wait 24–48 hours

- Check email updates

Works only for simple delays.

Level 2: Active Fix (Recommended)

- Call lender directly

- Ask for exact blocker

- Request priority processing

This speeds things up by 2–3x

Level 3: Aggressive Fix (Rare but Effective)

If delay is unreasonable:

- Ask for loan officer escalation

- Mention urgency (medical, emergency, etc.)

- Request written timeline

Banks respond faster when you push.

Lender Types & Their Disbursement Speed

| Lender Type | Speed | Risk | Approval Strictness |

|---|---|---|---|

| Traditional Banks | Slow | Low | Very High |

| Credit Unions | Medium | Low | Medium |

| Online Lenders | Fast | Medium | Medium |

| Instant Loan Apps (India) | Very Fast | High | Low |

Real Case Study (India vs USA Comparison)

Case 1: USA (Emily, California)

- Loan: $8,000

- Approved instantly

- Delayed 5 days

Reason:

- Address mismatch in credit file

Fix:

- Updated address → disbursed in 24 hrs

Case 2: India (Rahul, Bangalore)

- Loan: ₹2,00,000

- Approved & disbursed in 30 minutes

Reason:

- Aadhaar + PAN auto verification

BUT:

Interest rate was higher (hidden cost of speed)

Warning Signs Your Loan Might Get Cancelled

If you notice these → act immediately:

- No updates for 5+ days

- Repeated document requests

- “Under review” status for long time

- Lender not responding clearly

This means:

Your loan is at risk — not just delayed

Pro Tips to Get Faster Disbursement (Insider Level)

- Apply during weekdays (avoid weekends)

- Use same bank account as salary account

- Keep documents ready BEFORE applying

- Maintain stable credit usage (don’t spike suddenly)

- Avoid multiple applications

“Need Faster Loan Disbursement?”

Look for lenders that offer:

- Same-day funding

- Minimal verification

- Soft credit check approval

USA vs India: Why This Happens More in the USA

| Factor | USA | India |

|---|---|---|

| Approval Type | Conditional (common) | Instant approval (common) |

| Verification Depth | High (strict underwriting) | Medium |

| Disbursement Time | 1–7 days | Instant to 48 hours |

| Fraud Checks | Advanced AI systems | Growing but less strict |

| Risk Tolerance | Low | Moderate |

Reality:

USA banks are more cautious → more delays after approval

India apps are faster → but sometimes riskier approvals.

Step-by-Step: How to Fix It FAST

If your loan is stuck, don’t wait passively.

Do this:

Step 1: Check Loan Status (Important)

Ask:

- Is it approved or conditionally approved?

- Is it under final review?

Step 2: Upload Missing Documents Immediately

Common ones:

- Pay stubs

- Bank statements

- ID proof

Delay here = delay in money.

Step 3: Call the Lender Directly

Don’t rely on email.

Ask clearly:

- “What exactly is pending?”

- “What’s stopping disbursement?”

Step 4: Verify Your Bank Account

- Check name match

- Confirm micro-deposit

- Re-submit details if needed

Step 5: Avoid Any New Credit Activity

Don’t:

- Apply for another loan

- Use credit cards heavily

You can trigger re-evaluation.

Step 6: Complete E-Sign / Agreement

Many people miss this.

No signature = no disbursement.

Step 7: Escalate if Delayed

If it’s been more than 5–7 days:

- Request escalation

- Ask for timeline commitment

Insider Insight: How Banks Actually Think

Banks don’t care about your urgency.

They care about:

- Default risk

- Income stability

- Fraud probability

Even after approval, they’re asking:

“Should we REALLY release this money?”

If anything feels off → they delay.

Real-Life Case Study (USA)

John (Texas)

- Loan approved: $12,000

- Expected disbursement: 2 days

But money didn’t arrive.

Why?

- Employer verification failed (HR didn’t respond)

Result:

- Loan delayed by 6 days

Fix:

- John provided alternative income proof

Loan released next day.

Lesson:

Approval ≠ final clearance.

Comparison Table: Fix Options

| Problem | Best Action | Time to Fix |

|---|---|---|

| Conditional approval | Submit documents | 1–2 days |

| Bank verification issue | Re-verify account | Same day |

| Employer not verified | Provide alternate proof | 2–3 days |

| Agreement pending | E-sign immediately | Instant |

| Internal delay | Call & escalate | 1–3 days |

Mistakes People Make

- Waiting silently

- Ignoring lender emails

- Assuming approval = done

- Applying for multiple loans

- Entering wrong bank details

These kill your disbursement speed.

MaintainMarket Expert Advice

If your loan is stuck:

- Treat it like a pending deal, not a done deal

- Over-communicate with lender

- Submit everything fast

- Don’t panic — but don’t stay passive

Why MaintainMarket is Different

Most blogs just explain.

We focus on:

- Real borrower problems

- Practical fixes

- Insider financial behavior

So you don’t just learn — you solve the issue.

Action Plan (Do This Now)

- Check loan status (final vs conditional)

- Call lender support

- Upload pending docs

- Verify bank account

- Complete agreement

- Avoid new credit activity

- Escalate if needed

Where to Place Affiliate Links (Monetization)

Best placements:

- After “Step-by-Step Fix” → suggest fast lenders

- In comparison table → “Check approval speed”

- CTA section → “Apply with faster disbursement lenders”

Conclusion

Getting approved for a loan feels like the finish line.

But in reality…

It’s just the halfway point.

Disbursement depends on:

- Verification

- Risk checks

- Final confirmation

If your money is stuck, don’t wait.

Take action — and you can unlock it within days.

FAQs

Q1. How long does loan disbursement take in the USA?

Usually 1–7 business days.

Q2. Can a loan be cancelled after approval?

Yes, if verification fails.

Q3. What is conditional approval?

Approval subject to final checks.

Q4. Why is my loan not credited yet?

Pending verification or internal delay.

Q5. Can I speed up loan disbursement?

Yes, by submitting documents and contacting lender.

Q6. Does credit score affect disbursement?

Yes, if it changes after approval.

Q7. Is this common in India?

Less common due to faster digital approvals.

Q8. Should I apply again if delayed?

No, it may worsen your situation.

Q9. What does loan approved but pending mean?

It means final verification is not completed.

Q10. Can bank delay loan after approval?

Yes, due to risk checks or missing documents.

Q11. How to know if loan is fully approved?

You’ll receive final agreement + disbursement date.

Q12. Why is my loan stuck in underwriting?

Due to risk reassessment or document mismatch.

People searched for: No CIBIL Score? Get ₹20,000 Loan Instantly (Real Options) – 2026 Guide

Also read: Insurance Claim Under Investigation What To Do USA (2026): Why It Happens & How to Get Paid Faster

How to Get Out of Debt Fast in 2026 (USA) — The Brutal Truth About Credit Card Traps