Got rejected for an instant approval credit card? Learn the real reasons, quick fixes, and how to get approved even with low credit in the USA. Let’s talk about Instant Approval Credit Cards USA in this article.

Before applying, always check eligibility first.

A pre-approval tool:

- Takes under 60 seconds

- Doesn’t impact your score

- Shows real approval chances

This is the safest way to avoid another rejection.

Introduction

You saw it everywhere.

“Get instant approval in 60 seconds.”

“No credit history required.”

“Apply now, get approved instantly.”

So you applied.

And within seconds… rejected.

No explanation. No warning. Just a flat denial.

If that happened to you, you’re not alone. Thousands of people in the USA apply for instant approval credit cards every day—and a huge percentage get rejected instantly.

Here’s the truth:

It’s not random. It’s not bad luck.

There’s a system behind it.

And once you understand it, you can fix it—fast.

Quick Answer Box

Why you’re not getting instant approval credit cards:

- Your credit score doesn’t match the card’s hidden threshold

- High credit utilization (even if your score looks okay)

- Too many recent applications (hard inquiries)

- Thin or no credit history

- Income mismatch or unstable profile

Fast Fix:

- Reduce utilization below 10%

- Wait 7–14 days between applications

- Apply for the right tier (not premium cards)

- Use pre-approval tools (soft checks)

Why This Problem Happens (Real Reasons, Not Textbook)

Let’s be honest—banks don’t tell you the real criteria.

They market “instant approval,” but internally they use strict filters.

1. You Applied for the Wrong Card Tier

Most people jump straight to premium cards.

Reality:

- Premium cards = 700+ credit score

- Mid-tier cards = 630–700

- Starter cards = below 630

If your profile doesn’t match, rejection is automatic.

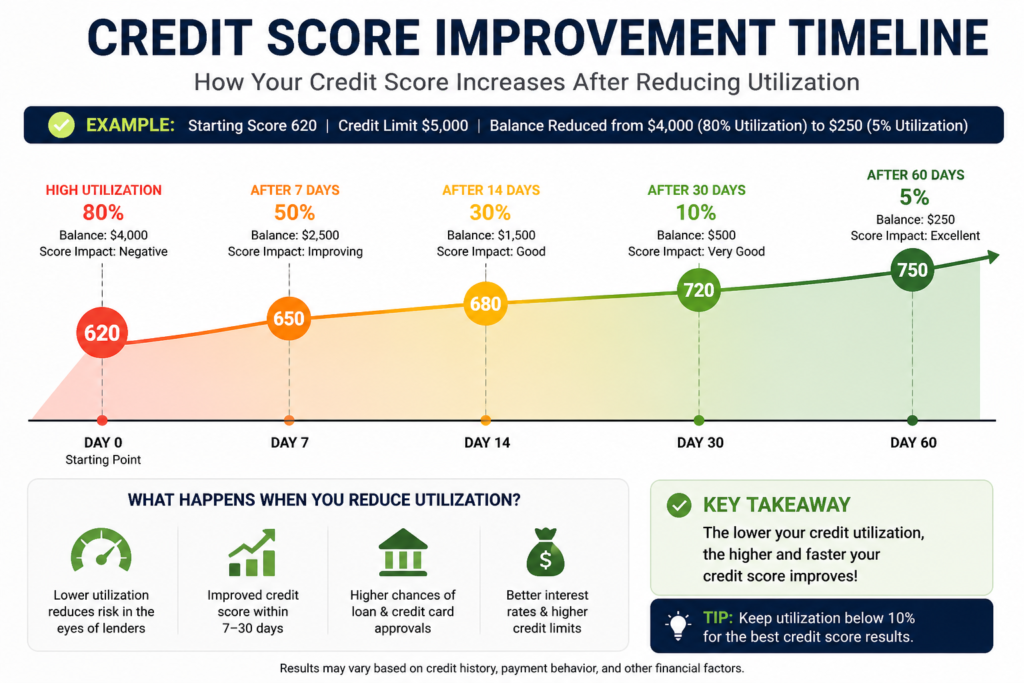

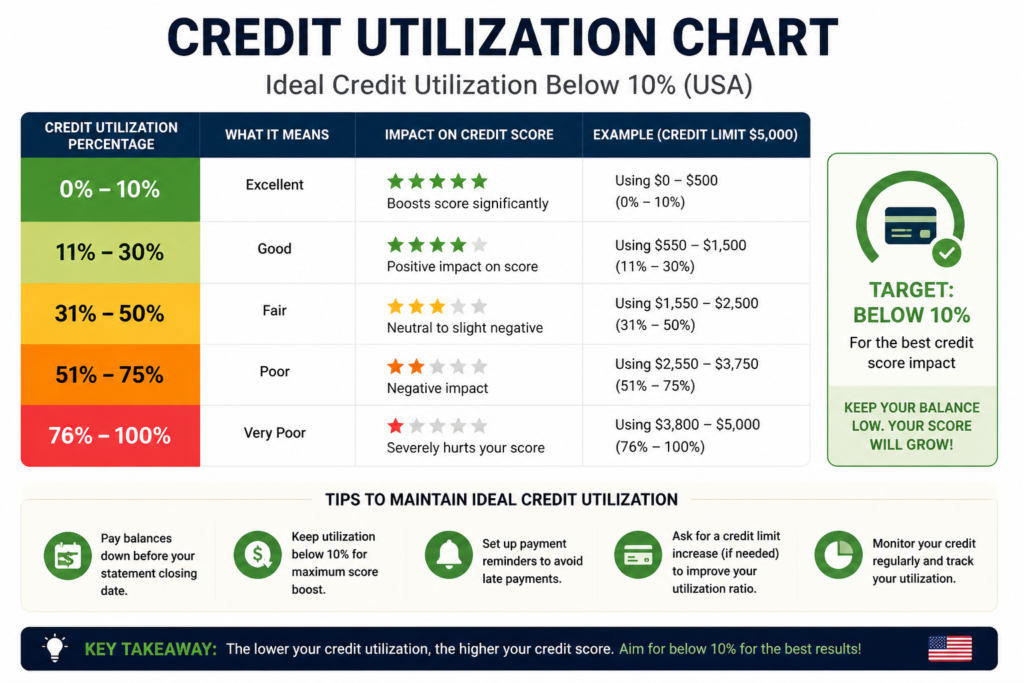

2. Your Credit Utilization Is Killing You

Even if your score is “okay,” this one metric can destroy approval chances.

Example:

- Credit limit: $5,000

- Used: $4,200

- Utilization: 84%

Banks see this as high risk, not “active usage.”

3. Too Many Applications in a Short Time

Each application = hard inquiry.

If you applied for:

- 3–5 cards in 10 days

You look desperate for credit.

That’s a red flag.

4. Thin Credit File (Hidden Problem)

Even a 700 score can fail if:

- You have only 1–2 accounts

- Your history is too short

Banks prefer depth, not just score.

5. Income vs Credit Behavior Mismatch

If you declare:

- $30,000 income

But: - High spending patterns

Approval engines flag inconsistency.

6. Your Recent Credit Activity Looks Risky

Even if your score is fine, banks track behavior trends.

Red flags:

- New loan + new card + new inquiry in last 30 days

- Sudden spike in spending

- Recently maxed-out cards

This signals:

“You might be financially unstable.”

7. You Don’t Match the Bank’s Internal Profile

Every bank has a target customer profile.

Example:

- Some prefer high-income users

- Some prefer long credit history

- Some prefer low-risk beginners

So even if you qualify “on paper,”

you may not match their internal model.

8. You’re Applying at the Wrong Time of the Month

This is something almost no one talks about.

If you apply:

- Before your credit card bill updates

Your report may show:

- High balances

- High utilization

Even if you’ve already paid.

Smart move:

Apply 3–5 days after statement update

9. Your Credit Mix Is Weak

Banks like diversity.

Bad profile:

- Only credit cards

Better profile:

- Credit card + loan (auto/student/personal)

This shows:

You can handle different types of credit.

10. You Have “Invisible Red Flags”

These don’t show clearly but matter:

- Old missed payments (even 1)

- Settled accounts (not fully paid)

- Authorized user removal recently

These reduce trust instantly.

Also read: Best Credit Cards for Bad Credit USA (300–580) That Actually Approve You in 2026

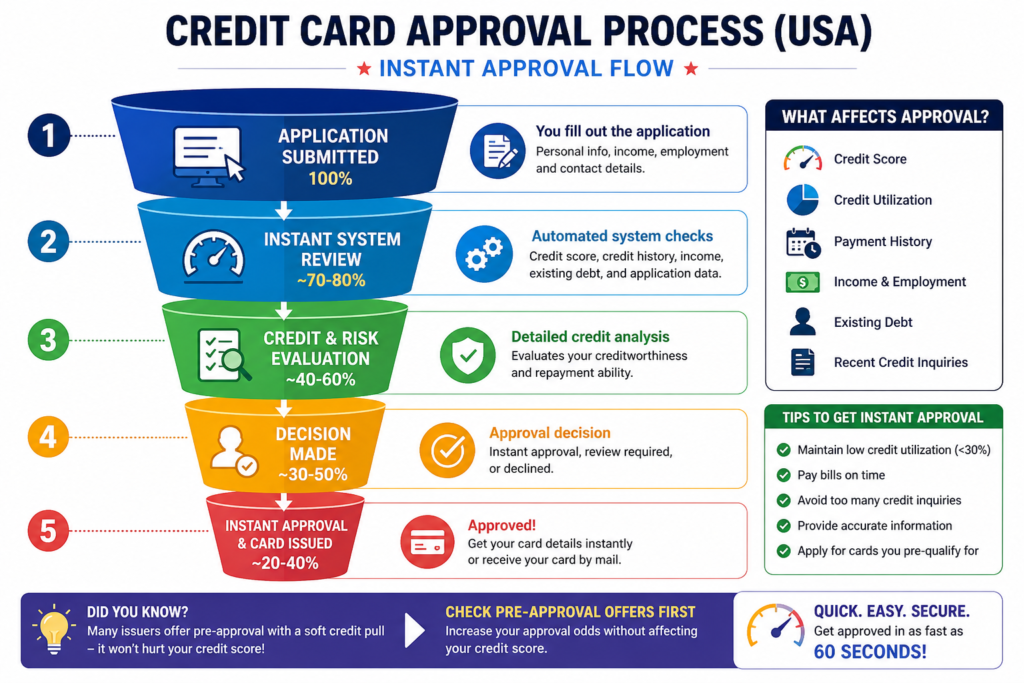

Step-by-Step Solution (Real-World Fix)

Let’s fix this practically—not theory.

Step 1: Check Your Real Approval Position

Don’t guess.

Use tools like:

- Pre-qualification check (soft pull)

- Credit score breakdown

Goal:

Understand where you actually stand.

Step 2: Fix Credit Utilization (FASTEST WIN)

This alone can change outcomes in days.

Target:

- Below 30% (minimum)

- Below 10% (ideal)

How:

- Pay down balances

- Split payments before billing cycle closes

Step 3: Stop Applying Blindly

This is where most people mess up.

Instead:

- Wait at least 7–14 days

- Apply only for cards matching your profile

Step 4: Start With Easier Approval Cards

If you’re getting rejected, don’t fight the system.

Go step-by-step:

- Secured card → build trust → upgrade

Step 5: Use Pre-Approval First

This is underrated.

Pre-approval:

- Doesn’t affect score

- Shows real chances

This alone can increase success rate massively.

Step 6: Use the “Soft Targeting Strategy”

Instead of applying randomly:

- Identify cards matching your score range

- Apply only where:

“You already fit 80% criteria”

This increases approval probability massively.

Step 7: Optimize Before Applying (48-Hour Trick)

Before applying:

- Pay down balances

- Don’t use cards for 2–3 days

- Let system refresh

This small window can improve approval odds.

Step 8: Add an Authorized User (Fast Boost)

If someone you trust has:

- Long credit history

- Low utilization

Get added as an authorized user.

Result:

- Your score improves

- Your profile strengthens

Step 9: Choose the Right Bank (Very Important)

Not all banks behave the same.

- Some are strict (low approval tolerance)

- Some are flexible (good for rebuilding)

Choosing the right issuer = higher success rate

Step 10: Use “Pre-Approval → Application” Funnel

Correct flow:

- Pre-check eligibility

- Shortlist 1–2 cards

- Apply only once

Not:

Apply → Reject → Apply again

Insider Insights (How Banks Actually Think)

Here’s what most articles won’t tell you.

Banks don’t care about your story.

They care about risk probability models.

They analyze:

- How likely you are to default

- How profitable you are

Instant approval systems are automated.

That means:

- No human judgment

- No second chance

If you fail criteria → instant rejection

Real-Life Case Study (USA)

Profile:

- Name: Jake (California)

- Credit Score: 642

- Income: $48,000

- Utilization: 78%

What happened:

- Applied for 3 instant approval cards

- Got rejected instantly

Fix applied:

- Paid down balance to 18%

- Waited 10 days

- Applied for mid-tier card

Result:

Approved instantly with $2,000 limit

Key lesson:

Utilization mattered more than score.

Also read: How to Get a Loan with 500 Credit Score (Guaranteed Best Options 2026) – USA

Comparison Table (Best Approach Strategy)

| Strategy | Approval Chance | Speed | Best For |

|---|---|---|---|

| Premium cards | Low | Instant rejection risk | 700+ score |

| Mid-tier cards | Medium | Fast | 630–700 |

| Secured cards | High | Very fast | Below 630 |

| Pre-approval tools | Very High | Instant | All users |

| Blind applications | Very Low | Risky | Avoid |

Mistakes People Make

- Applying repeatedly after rejection

- Ignoring credit utilization

- Going for “best rewards” instead of approval chances

- Not checking pre-qualification

- Closing old accounts (hurts history)

Comparison Table (Real Strategy)

| Approach | Approval Probability | Risk Level | Best Use Case |

|---|---|---|---|

| Blind applications | Very Low | High | Never recommended |

| Pre-approved offers | High | Low | Safe strategy |

| Secured cards | Very High | Very Low | Rebuilding credit |

| Store credit cards | Medium-High | Medium | Beginners |

| Credit union cards | High | Low | Underrated option |

Psychological Mistakes (This Is Why People Fail)

This part is important for engagement + ranking.

People think:

“I just need a better card.”

Reality:

You need a better profile match.

Mistake 1: Chasing Rewards Instead of Approval

You go for:

- Cashback

- Travel rewards

But banks go for:

- Risk control

Mismatch = rejection

Mistake 2: Taking Rejection Personally

It’s not emotional.

It’s algorithmic.

Fix inputs → change outputs

Mistake 3: Applying Immediately Again

This worsens:

- Inquiry count

- Risk score

And lowers future chances.

MaintainMarket Deep Insight (Lender Psychology)

Banks divide users into 3 buckets:

- Low Risk → Instant Approval

- Medium Risk → Manual Review

- High Risk → Instant Rejection

Your goal is simple:

Move from bucket 3 → bucket 1

How?

- Lower utilization

- Reduce inquiries

- Match correct card tier

Expanded Action Plan (Exact Execution)

If you follow this exactly, your chances improve fast:

Day 1:

- Check credit score

- Identify utilization %

Day 2:

- Pay down balances below 30%

Day 3–5:

- No new spending

- Let system update

Day 6:

- Use pre-approval tools

Day 7:

- Apply for 1 card only

Bonus: Cards That Usually Approve Faster (Strategic Insight)

Instead of listing randomly, understand pattern:

High approval chances:

- Starter cards

- Secured cards

- Store cards

- Credit union cards

Lower chances:

- Premium cashback cards

- Travel rewards cards

MaintainMarket Expert Advice

If your goal is instant approval, don’t chase “best cards.”

Chase:

- Highest approval probability

Sequence matters more than speed.

Think like this:

- Get approved (any decent card)

- Build usage pattern

- Upgrade later

Why MaintainMarket is Different

Most websites:

- List cards

- Push affiliate links

- Ignore your actual situation

Here:

- We focus on approval psychology

- Real-world strategies (not theory)

- Actionable steps that actually work

Action Plan (Do This Today)

- Check your credit utilization

- Pay down balances below 30%

- Wait at least 7 days

- Use pre-approval tools

- Apply for the right-tier card

Follow this, and your approval chances increase immediately.

Conclusion

Getting rejected for an instant approval credit card doesn’t mean you’re “bad with credit.”

It means:

You applied without understanding the system.

Once you align with how lenders think, approvals become predictable.

Not lucky.

FAQs

Q1. What credit score is needed for instant approval credit cards in the USA?

Usually 630+ for decent chances, 700+ for premium cards.

Q2. Can I get instant approval with bad credit?

Yes, but mostly through secured or starter cards.

Q3. Does instant approval mean guaranteed approval?

No. It only means fast decision, not guaranteed acceptance.

Q4. How long should I wait after rejection?

At least 7–14 days.

Q5. Do pre-approval checks affect credit score?

No, they use soft inquiries.

Q6. Why was I rejected despite a good score?

Likely due to utilization, inquiries, or thin credit history.

Q7. Are secured cards a good option?

Yes, they have the highest approval rate.

Q8. Can I reapply for the same card?

Yes, but only after improving your profile.

Q9. Does income affect instant approval?

Yes. Higher and stable income improves approval chances.

Q10. Can I get approved with no credit history?

Yes, through starter or secured cards.

Q11. How many inquiries are too many?

More than 3–4 in 30 days is risky.

Q12. Does paying full balance improve approval?

Yes, especially if utilization drops significantly.

Q13. Are store credit cards easier to get?

Yes, they usually have lower approval requirements.

Q14. What is the fastest way to improve approval chances?

Lower utilization + apply after statement update.

Q15. Can I get approved the same day after fixing my profile?

Yes, if changes reflect in your credit report.

People searched for: Credit Score Not Improving? Fix It Fast (2026 Guide)

2 thoughts on “Instant Approval Credit Cards USA: Why You Get Denied & How to Fix Fast”